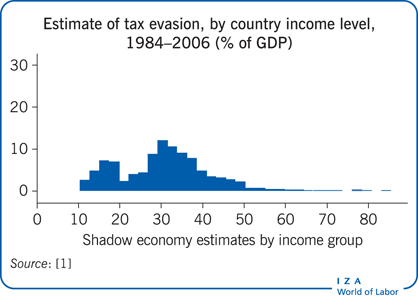

Elevator pitch

To determine the full effects of taxation on income distribution, policymakers need to consider the impacts of tax evasion. In the standard analysis of tax evasion, all the benefits are assumed to accrue to tax evaders. But tax evasion has other impacts that determine its true effects. As factors of production move from tax-compliant to tax-evading (informal) sectors, changes in relative prices and productivity reduce incentives for workers to enter the informal sector. At least some of the gains from evasion are thus shifted to the consumers of the output of tax evaders, through lower prices.

Key findings

Pros

Understanding the effects of tax on the income distribution is a central concern of policymakers.

Standard tax incidence analysis does not adequately consider how tax evasion affects the distribution of income because the typical approach assumes that evaders keep all benefits.

Proper analysis of the incidence of tax evasion must recognize the general equilibrium effects.

Successful tax evasion may encourage others to enter the same occupation as the evader, and new entry will reduce the advantage of tax evasion.

Cons

Even research that incorporates general equilibrium adjustments omits some relevant issues.

No study has yet simultaneously explored the full range of general equilibrium adjustments, effects of agents behaving under uncertainty, and different degrees of competition and entry.

The administrative and compliance costs of taxation and other important considerations have not been fully studied for tax evasion.

Knowledge of the true incidence of taxes is incomplete.