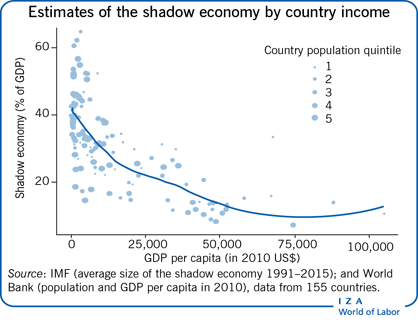

Elevator pitch

How does tax evasion affect the distribution of income? In the standard analysis of tax evasion, all the benefits are assumed to accrue to tax evaders. However, tax evasion has other impacts that determine its true effects. As factors of production move from tax-compliant to tax-evading (informal) sectors, these market adjustments generate changes in relative prices of products and factors, thereby affecting what consumers pay and what workers earn. As a result, at least some of the gains from evasion are shifted to consumers of goods produced by tax evaders, and at least some of the returns to tax evaders are competed away via lower wages.

Key findings

Pros

Tax evasion creates a cascade of market adjustments as firms and individuals react to changing incentive structures.

Successful tax evasion may encourage others to enter the same occupation as the evader, and new entry will reduce the advantage of tax evasion.

A full analysis of the effects of tax evasion must recognize and incorporate general equilibrium adjustments via the interactions of supply and demand across multiple markets.

Recent research that incorporates general equilibrium adjustments suggests that tax evasion has large, and often neglected, effects on the distribution of income.

Cons

Standard tax incidence analysis does not adequately consider how tax evasion affects the distribution of income.

Most research neglects general equilibrium adjustments, resulting in incomplete and potentially misleading findings.

No study has yet simultaneously examined the full range of relevant factors.

As a result, knowledge of the true effects of tax evasion remains incomplete.