Elevator pitch

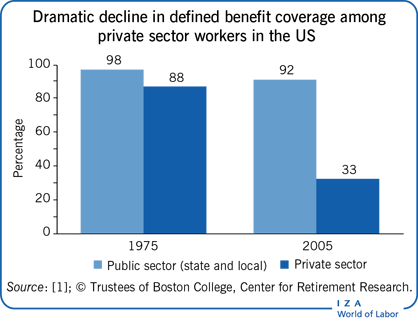

The relationship between retirement plan type and job mobility is more complex than typically considered. While differences in plan features and benefit structure may directly affect employees’ mobility decisions (“incentive effect”), the type of plan offered may also affect the types of employees a given employer attracts (“selection effect”), thereby affecting mobility through a second, indirect channel. At the same time, some employees may not be able to accurately assess differences between plan types due to limited financial literacy. These factors have implications for policymakers and employers considering retirement plan offerings.

Key findings

Pros

The relationship between higher job mobility and increased prevalence of defined contribution plans is in part driven by employee preferences for higher job mobility.

The choice structure governing a transition between a defined benefit and a defined contribution plan is key for employee enrollment outcomes.

A firm considering a transition from a defined benefit to a defined contribution plan needs to consider the effects on existing employees separate from new employees.

Cons

Evidence shows that employees place low value on additional defined benefit plan benefits, which may be in part due to low financial literacy.

Even employees who make an active choice (i.e. complete paperwork) between a defined benefit and defined contribution plan at a given employer are highly influenced by which plan the employer selects as the default plan (i.e. plan enrollment if no choice is made).

More research is needed on retirement plan valuation by employees just starting their careers.