Elevator pitch

For decades, pension systems were based on the rising revenue generated by an expanding population (the so-called demographic dividend). As changes in fertility and longevity created new population structures, however, the dividend disappeared, but pension systems failed to adapt. They are kept solvent by increasing redistributions from the shrinking working-age population to retirees. A simple and transparent structure and individualization of pension system participation are the key preconditions for an intergenerationally just old-age security system.

Key findings

Pros

Pension reform can improve social equity by balancing the interests of workers and retirees.

By lowering labor costs, pension reform can reduce entry barriers to the labor market.

Pension reform can reduce tax distortions that discourage job creation.

By reducing subsidies to the pension system, reform can improve public finance.

More transparent institutions can lead to more rational decisions on savings, work, and family.

Cons

Pension reform faces political obstacles from the opposition of those due to retire or recently retired.

The strong tendency to make the same choices as in the past ignores condition changes.

Pension system complexity makes it hard to see the need for reform, and to assess its merits.

If reforms involve financial markets, positive as well as negative externalities may arise.

Accounting applied to contributions flowing through pension systems misleads and tempts politicians to hide the real scale of indebtedness.

Author's main message

Pension systems need to be redesigned to accommodate demographic changes. Postponing adjustment simply increases the economic and social costs. The interests of workers (deductions from wages) and retirees (receipt of benefits) differ. Governments need to make pension systems more transparent and make adjustments to reduce the burden on workers, returning the pension system to its social role, which is helping the very old without overburdening the young. Pension solidarity should not be confused with political discretion. Transparency and fairness are the key preconditions when adjusting pension systems for the 21st century.

Motivation

Pension systems based on rising revenues made possible by demographic growth (demographic dividend) are unsustainable. These systems were devised at a time when each new working generation was more numerous than the previous, which enabled easy and cheap financing of pension and other government expenditures out of rolled-over debt. This was a brief window, however; as the dividend disappears, society needs to adjust, particularly its pension systems.

These demographic changes, which play a crucial role in the life of societies, are generally perceived with a lag. Policies—even if well designed and generously financed—cannot substantially alter demographic trends. Rather, institutions need to adapt to demographic developments. If pension systems are not adjusted to population developments, huge social and economic problems will arise, including increasing intergenerational conflict.

There have been many studies dealing with pension issues (for instance [1], [2], [3], [4]), but there are no clear prescriptions on how to solve the problem of inflated pension expectations [5]. This article addresses some of the issues that make redesigning pension systems difficult. Chief among them are public perceptions about the role and financing of public pension systems.

Discussion of pros and cons

The impact of demographic change on pension systems

Countries were able to build and fund welfare state institutions without unduly burdening the economy by using the additional revenue collected during the demographic transition, when the working-age population (and the number of taxpayers) grew rapidly. The demographic dividend disappeared at the end of the 20th century in many countries as the working-age population began to shrink. Instead of surpluses, countries were racking up deficits. Huge hidden and open debts have accumulated since the dividend disappeared [6], but institutions continue to be financed as if it were still available.

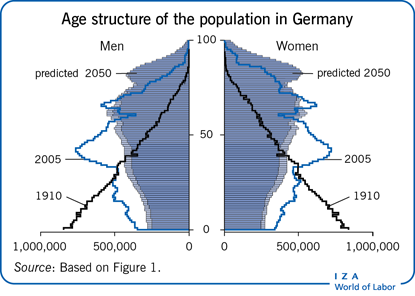

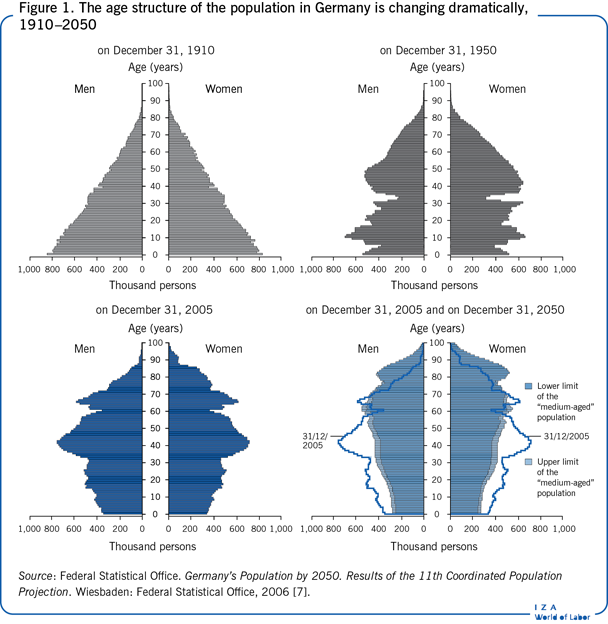

When traditional pension systems were established, around a century ago in many countries, numerous workers paid contributions that financed the pensions of relatively few old people. For example, in Germany in 1950, there were 16 people aged 65 and older for every 100 of working age. That meant that contributions to pay for pensions were a small share of wages. Projections for 2050 show that share rising to 67 people aged 65 and older for every 100 people of working age, a clearly unsustainable ratio [7]. Figure 1 illustrates the scale of the population change, using Germany as an example.

Initially, the key goal of pension systems was to reduce poverty in old age through taxation or quasi-taxation of the economically active population. Taxation was selected as the means for funding old-age pensions because that was politically convenient and because technology at the time did not allow for individualized participation. Because the social tax was fairly low, negative labor market externalities were negligible.

When pension systems were established, the vast majority of workers died before retirement. Today, most workers live into retirement. With that demographic shift, the pension system goal has shifted from old-age poverty alleviation to income reallocation over time. Transferring large amounts to the young-old not only put a heavier burden on the working population but also reduced the resources left for financing transfers to the very old, weakening old-age poverty alleviation.

Workers retire much earlier today than in previous generations, in terms of their lifespan as well as their age, weakening the social justification for imposing taxes on the working generation. Today, youths are increasingly at risk of poverty, while retirees are—relative to the average—well off [5]. A pension system provides an institutional structure for intergenerational transfers. The economically active population produces national income that is then divided between remunerating production factors (labor and capital) and financing pensions (given other expenditure). Pension system designs vary across the world, as there are a number of different ways to organize this intergenerational transfer. But, however financed, pension promises are fulfilled at the expense of the current working generation's welfare. The design of future pension systems has to take into account the interests not only of retirees but also of workers, especially the young.

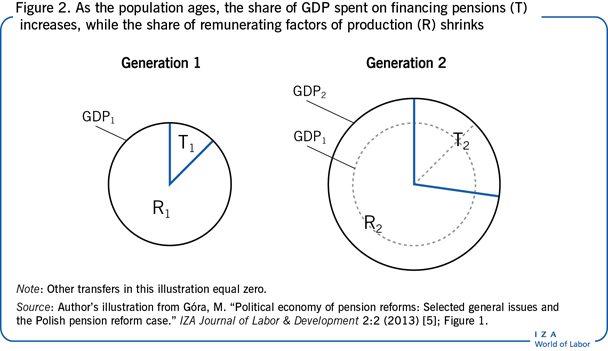

Unless contributions are adjusted as the population age distribution changes, the share of gross domestic product (GDP) spent on financing pensions increases. The increase is unintentional, endogenous to the pension system. Figure 2 illustrates the problem.

Population aging has led to a substantial increase in the share of GDP spent on pensions (T2 is larger than T1), which implies that a smaller share is going to remuneration of production factors (the share of R2 in GDP2 is smaller than the share of R1 in GDP1). This means that generation 2 workers are more poorly remunerated for their activity and productivity growth (as a share of GDP) than generation 1 workers.

Reform options

Today, the revenue available to fund pension systems is declining as the share of the retirement-age population expands and the working-age population shrinks with declining fertility and increasing longevity. Countries are in different phases of change. Understanding the root of the problem is crucial for a rational response. But this is made more difficult by the complexity of traditional pension systems, which leads to misunderstandings about how they work.

The average level of pension benefits depends only on the proportion of those who pay contributions/taxes to those who receive benefits (given the contribution/tax rate). This is contrary to the perceptions of generations whose understanding of pension systems were formed at the time when the demographic dividend was generated. They believed that pensions depend on political decisions or on financial market performance.

Government efforts to reform pension systems are typically fiscally driven. Pension expenditures are very high as a share of GDP and are projected to rise further. Expenditures continue to rise because traditional pension systems lack adjustment mechanisms. The expectation was that politicians would take steps to ensure that pension systems remain adequately funded. That assumption held (more or less) when the demographic dividend was generated. Today, however, imposing adjustments of the size needed to keep systems sustainable means delivering very bad news to the public: in the future, pensions will have to be reduced relative to wages. Politicians, fearing the consequences of such a decision, put off announcing the bad news. But failing to deliver the message and to make the necessary adjustments means that pension systems will go bankrupt—today in an actuarial sense and tomorrow in cash flow terms as well.

The political response to deteriorating pension system finances was first to increase contributions, and then, when the burden on the working-age population grew too large, to increase (largely hidden) debt. The burden was just moved from this generation to the next. That option might be justified if it was possible that future generations would have a greater ability to pay back the debt than the current generation, but demographic change rules that out. Now these two options have been played out. Contributions/taxes and indebtedness are already very high [6]. Adjustments are inevitable, but they come decades late. They should have begun as the demographic trend began to shift.

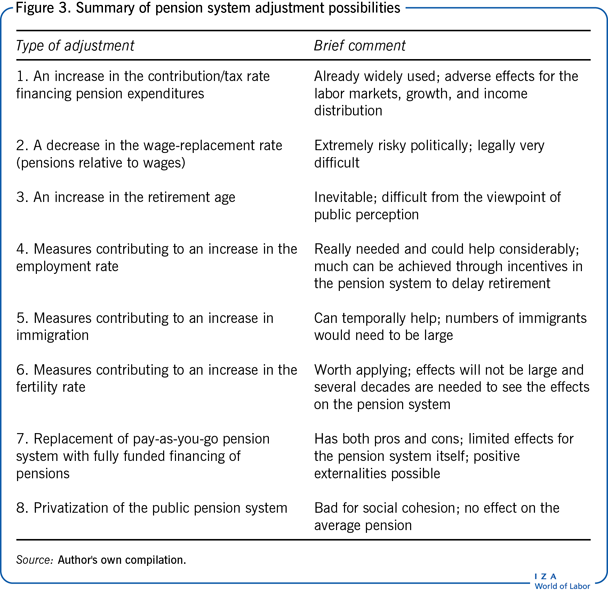

Several types of adjustments to pension system policies are possible, but none is easy to apply (Figure 3). Increasing the contribution rate used to be relatively easy, but rates are now so high that they hurt employment and growth. Moreover, increasing contributions is a short-term solution at best. According to projections, the population will continue to age. Allowing debt to accumulate leads to a higher burden for the working-age population. So even if increasing the contribution rate was feasible, it would have to be repeated again and again. It is hard to imagine that any politician would be willing to take such a politically risky approach.

The level of pensions measured in terms of wages (the replacement rate) can be reduced slightly through indexation below the productivity dynamics of economically active workers. However, substantial reductions in pension benefits are politically unfeasible. Pensioners constitute a well-defined interest group, which unites them as voters.

Increasing the retirement age is the most promising method to improve the sustainability of pension systems [8], [9]. In effect, it combines raising contributions and lowering benefits. Workers who work longer contribute more to the system and take out less, since they will be receiving the benefits for a shorter period. Increasing the pension age is less burdensome to most people than either of its two components since it does not raise flows of monthly payments or reduce flows of monthly benefits. But increasing the retirement age is difficult. Popular protests often force politicians to back down. Evidence suggests that raising the retirement age is possible only if done prospectively, in step-by-step, clearly pre-announced future increments. The recent economic and financial crises shifted public opinion slightly toward some acceptance of more radical policy changes.

Pension reform is needed for more than fiscal reasons. It is needed to improve job opportunities for the young and to end the drag on economic growth. Although increasing employment goes beyond pension policies, much can and should be done. Designing a fair and transparent pension system, with individualized participation, could help the labor market as well as the pension system. Individualized participation reduces the perception of pension contributions as taxes, thereby reducing tax distortions. These goals, commonly on the margin of public debate on pensions, need to be brought into the center, so that they can gain greater support.

Immigration is a delicate political and social issue as well as a potential pension financing issue [10]. If the scale of immigration is large enough, it could have a positive effect on the pension system since immigrants are usually younger than the average citizen. If the immigrants work legally, they contribute to the pension system for many years before they start receiving benefits. However, to have a substantial effect on the population age distribution, immigration flows would have to be huge. Mass immigration would need to be absorbed into formal employment. However, financial easing of pension systems today will increase pension system liabilities in the future.

Encouraging higher fertility is another delicate issue. There is evidence that pronatalist policies can help raise the population growth rate from below the replacement level to close to that level but no higher. This means that even successful efforts to boost the population growth rate will not yield a new demographic dividend, which would require three or more children per woman; in most European countries two children per woman would already be an extremely ambitious goal.

Switching to a fully funded system and privatizing the public pension system can have both positive and negative outcomes. They neither increase benefits nor decrease contributions, but both funding and privatization may support implementation of other adjustment methods.

Pension systems can be organized for the entire working population (public system) or for groups or individuals (private system). Pension reform aims at fixing the public system. Privatizing the public pension system would eliminate its solidarity-based nature. But there are other options. A public system can be run by a private firm and remain public, while also introducing such reforms as individualized pension accounts and financial market investments. However, a key feature of 21st-century public pension systems is individual-ization of participation, which is still based on solidarity—understood as sharing the outcomes of the universal system. But, participation in the system is based on the rules instead of political discretion (as in traditional defined benefit systems).

Possible ways of implementing adjustment mechanisms

Most pension system reforms have involved finding new sources of revenue and ways to reduce spending while retaining their general framework (rationalization). This approach, as well as more ambitious partial reforms, can improve the fiscal status of pension systems, but it further complicates what are already very complex systems.

In a democratic society, pension system adjustments need the support of a majority. But implementing reforms is difficult because pension systems are complex and nontransparent. Most people know little about the mechanisms influencing performance or about the reforms needed to make the systems sustainable. That makes it hard for people to understand why they should pay higher contributions or receive lower benefits or work longer. People continue to demand the same level of benefits, which leads to inflated expectations. Thus, regulation is left to political discretion. That worked when the demographic dividend was positive and large, but it ceased to work after the dividend disappeared and pension system deficits grew. Once the demographic dividend disappears, the choice societies face is clear: the more they spend on financing pension transfers, the less that is left for remunerating production factors—especially for labor and other expenditures. The dramatic choice cannot be avoided. It has to be well managed.

But politicians postpone making difficult decisions as long as they can, since the required adjustments necessarily mean less generous arrangements (e.g. higher contributions, lagged indexation of benefits, later retirement). However, politicians have run out of time. The time to implement the reforms listed in Figure 3 is now. These reforms can be applied within the following general framework:

Fine-tuning, which should be applied in advance of other measures.

Rationalization (parametric reform), by finding new sources of revenue and ways to reduce spending.

Reform, by radically changing elements of the system.

Automatic adjustment, by neutralizing the pension system's impact on remuneration of production factors and stabilizing the share of GDP devoted to the pension system.

Neutralization occurs as the pension system is transformed from tax financing to savings financing (during the contributory phase) and then to an insurance function (after retirement). The goal is to make the present value of contributions equal the present value of benefits, so that the share of GDP going to finance pensions is constant and remuneration of production factors is not affected.

Automatic adjustment can work properly in bad times as well as good, while discretionary adjustment works only in good times. Automatic adjustment protects the interests of both the working population and retirees, while discretionally regulated pension systems tend to favor the interests of retirees over the working generation. Pension reform should be presented as an effort to protect the interests of the working generation. Automatic adjustment seems the most effective mechanism for doing so [5].

Future wage replacement rates will have to be lower for obvious demographic reasons. Implementing an automatic adjustment system would provide fair information on declining benefits in advance. This decline is population-driven and should not be confused with cutting benefits. Automatic adjustment simply reduces inflated pension expectations to the level that the next generation is able and willing to meet—and it does so in advance, so that people are prepared.

Both automatic and discretionary mechanisms favor either those who produce or those who receive transfers. As long as the adjustment works in favor of one group or the other, the choice is difficult but clear. In real life, the situation is more complex. Regular employment of labor is shrinking while various types of irregular employment are expanding. This implies that people can, to an extent, avoid participating in mandatory pension systems, further reducing the resources for financing pensions.

Traditional pension systems enable individuals to reduce their participation without being exposed to income problems afterwards, thus creating a perverse incentive to free ride. This type of incentive is much weaker if participation is individualized. However, that can result in the undesirable social outcome of some people failing to have adequate pension rights in their old age. This problem requires a specific policy response, but the design of traditional pension systems just hides the problem; it does not solve it. Solutions are outside the pension system, requiring labor market regulations for the 21st century.

The key advantages of individualization are transparency and automatic adjustment. Individualized systems can work in one of two ways: nonfinancial, based on the real economy, and financial, based on financial markets [11]. In both cases, individual accounts are turned into annuities after retirement. According to currently applied accounting procedures, nonfinancial accounts do not increase public debt, making them more popular with governments, while financial accounts do. Financial accounts are easier for people to understand, while nonfinancial accounts require some economic knowledge. The two types of account are only partially correlated, so they are more stable combined than each is individually. This provides risk diversification and greater security.

Limitations and gaps

There is no one good prescription for redesigning pension systems. Doing so is an open challenge, requiring dealing with multiple limitations and gaps in such areas as the optimal pace for implementing new institutions. This article addresses selected general problems and offers some suggestions for dealing with them. Countries need to choose their own approach.

Summary and policy advice

Public debate about pension systems is difficult because they are complex. Breaking the issues into three levels might help [5]:

Social goals and economic fundamentals: GDP is divided between generations (factors of production and pensions), based on the population structure.

Method: Basic arrangements for acquiring pension rights in terms of future GDP.

Regulations: Many institutional arrangements are possible.

All three areas are important to a well-designed pension system. To lead to rational conclusions, discussion should progress from goals to methods to regulations. Public debate has tended to move in reverse, which leads to incoherent discussion.

The inability of institutions to adapt to the changed demographic pattern is at the core of the pension system problem. Unable to change demographic trends, countries must adjust their institutional structures to the new situation. Waiting is an expensive error. During this difficult demographic period, institutions need transparency more than ever. Nontransparent institutions generate public unrest, making adaptation difficult. More transparency makes it easier to understand the trade-offs and to adapt to reality.

The central value behind pension reform is reintroducing intergenerational equilibrium by recognizing participants’ interest in both phases of their life: economically active and retired. A reformed pension system should aim for an optimal combination of the contribution rate and the wage replacement rate. The first step for a successful adaptation of pension systems to the 21st-century reality is individualization of participation. Using financial markets is possible but not necessary. So redesigning pension systems may be easier than typically assumed.

Acknowledgments

The author thanks an anonymous referee and the IZA World of Labor editors for many helpful suggestions on earlier drafts. Version 2 of the article includes minor text updates to the “Cons” and “Author's main message,” plus brief additional material on individualization, solidarity, and immigration. The “Further reading” references have been updated and a new “Key reference” has been added [9].

Competing interests

The IZA World of Labor project is committed to the IZA Code of Conduct. The author declares to have observed these principles.

© Marek Góra