Elevator pitch

Around ten countries currently use a variant of a national income-contingent loans (ICL) scheme for higher education tuition. Increased international interest in ICL validates an examination of its costs and benefits relative to the traditional financing system, time-based repayment loans (TBRLs). TBRLs exhibit poor economic characteristics for borrowers: namely high repayment burdens (loan repayments as a proportion of income) for the disadvantaged and default. The latter both damages credit reputations and can be associated with high taxpayer subsidies through continuing unpaid debts. ICLs avoid these problems as repayment burdens are capped by design, eliminating default.

Key findings

Pros

ICLs deliver consumption smoothing by reducing or eliminating student loan repayment burdens on disposable income when debtors’ future incomes are low.

By coupling loan repayment amounts to a debtor’s actual income, ICLs provide insurance against default.

ICL debt can be collected efficiently if functional tax and personal identification systems are in place.

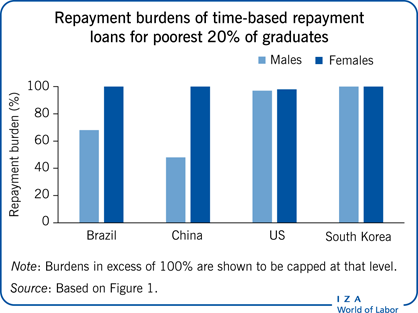

Cons

TBRLs have the strong potential to create major repayment difficulties for borrowers.

TBRLs do not provide debt default insurance for borrowers.

TBRLs can lead to credit reputation loss for the borrower due to default.

Systems based on TBRLs create inequality in educational access due to a high fear of future debt default by low-income prospective students.

ICLs have sophisticated administration requirements that may be unachievable for some countries.