Elevator pitch

Economists have long recognized that free trade has the potential to raise countries’ living standards. But what applies to a country as a whole need not apply to all its citizens. Workers displaced by trade cannot change jobs costlessly, and by reshaping skill demands, trade integration is likely to be permanently harmful to some workers and permanently beneficial to others. The “China Shock”—denoting China’s rapid market integration in the 1990s and its accession to the World Trade Organization in 2001—has given new, unwelcome empirical relevance to these theoretical insights.

Key findings

Pros

Trade among consenting nations raises GDP in all of them.

The benefits from trade tend to be small at the individual level but broadly distributed and hence large in aggregate.

Because trade grows the national pie, it creates an opportunity for every citizen to acquire a modestly larger slice; no one necessarily need have a smaller slice.

Policymakers have multiple levers available to ensure that the gains from trade are more broadly shared.

Cons

Without policy intervention, trade will almost necessarily harm some individuals and industries.

Labor market adjustments to trade operate with weakness and are materially offset by forces that amplify trade-induced displacement.

The adverse impacts of trade are highly concentrated among specific worker groups and locations.

Trade-induced employment impacts are magnified by inter-industry linkages, creating adverse spillovers to other manufacturers and non-manufacturers.

Trade adjustment programs are too small to be economically consequential, and passive responses to worker displacement impede labor market adjustment.

Author's main message

International trade integration creates diffuse benefits and concentrated costs. Until recently, economists were sanguine about the limited practical relevance of theoretical implications for workers in developed countries. Evidence from the China Shock has overturned this benign view. China’s rapid rise, while enormously positive for world welfare, has created identifiable losers in trade-impacted industries and the labor markets in which they are located. To mitigate the harms and share the benefits of trade integration more broadly, policymakers should consider modernizing trade adjustment programs, providing wage insurance to displaced workers, and expanding the set of workers eligible for work-contingent wage support, such as the US Earned Income Tax Credit.

Motivation

The costs and benefits of free trade are among the most contentious topics in economic policy, no less today than two centuries ago when David Ricardo developed the theory of comparative advantage. While economists often argue in policy discussions—though not in textbooks—that trade is Pareto improving (i.e. at least one party wins without any other party losing), most laypeople view it as a constant-sum game, wherein exporters win and importers lose. In truth, both views are oversimplified. Trade grows the economic pie—that is, it is not constant-sum—but it typically shrinks the slices received by some citizens. Economic policy must grapple with how to maximize the shared gains while mitigating the concentrated costs that accompany trade integration.

Discussion of pros and cons

The conventional wisdom

Introductory theory treats trade between nations as not typically being Pareto improving. In their undergraduate textbook, Paul Krugman and Maurice Obstfeld write: “Owners of a country’s abundant factors gain from trade, but owners of a country’s scarce factors lose. […] [C]ompared with the rest of the world the United States is abundantly endowed with highly skilled labor and […] low-skilled labor is correspondingly scarce. This means that international trade tends to make low-skilled workers in the United States worse off—not just temporarily, but on a sustained basis” [2].

For the first three or four decades after World War II, however, there was little cause to question the benefits of trade. Most trade occurred between nations with similar average incomes, which meant that any distributional impacts were limited. The rise of inequality in the 1980s and 1990s spurred an extensive literature that sought to quantify the contributing roles of trade, technology, labor market institutions, and other factors. A reasonable summary of the consensus around 2000 was: (i) Trade had not been a major contributor to declining manufacturing employment or rising wage inequality in developed countries over the past several decades. (ii) If displaced by trade, workers employed in regions specializing in import-competing sectors could easily move to other labor markets. (iii) Due to the "law of one price" for skills—meaning that skills, like currency, have the same market value anywhere within a given country—any adverse effects of trade on low-skilled workers would reduce the wages of this group nationally, rather than primarily affecting the outcomes of trade-exposed workers [3].

Based on these observations, it was generally held that while trade might modestly affect national wage levels, it would have no effect on regional or local employment rates. Moreover, considering the assumed fluidity of the US labor market, the aggregate gains from trade in the US should be positive, even in the short or medium term (that is, without much delay due to frictional adjustment).

Just as economists were reaching consensus on the impacts of trade on wages and employment, an epochal shift had begun. China, which had lagged economically for centuries, was emerging as a global power and, in the process, reshaping established patterns of trade. The long-held belief that while trade might in theory be strongly redistributive, when in practice it was relatively benign, has been overturned by more recent evidence. Similarly, the idea that trade adjustment is rapid and relatively painless, with effects spread out over broad skill categories rather than being born disproportionately by workers in trade-competing industries or locations, has also been discredited. Moreover, when measuring the potential gains from trade, recent evidence finds that the short- and medium-term adjustment costs of large trade shocks are substantial.

China’s rise over the past decades offers a rare opportunity to study the labor market impacts of a large trade shock in developed economies. The evidence gained from studies of this phenomenon makes it clear that the distributional consequences of trade are robustly evident, consistent with canonical theory.

While this evidence does not refute the long-held view that trade increases aggregate welfare or national incomes—indeed, China’s meteoric rise from endemic poverty to burgeoning prosperity bears testimony to the potential of trade to deliver rising living standards—it makes clear that trade has both significant benefits and substantial costs. These include distributional costs, which have long been recognized by canonical theory, and adjustment costs, which the literature has typically downplayed. Gaining a keener understanding of when and where trade is costly, and how and why it may be beneficial, are key goals for trade and labor economists. Likewise, policymakers and applied economists should devote renewed focus to managing and mitigating the costs of trade adjustment.

The “China Shock”

One of the toughest challenges for empirical analysis of the causal effects of trade on labor markets is that changes in one country’s trade policy are often driven by changes in the behavior of its trading partners. Several features of China’s economic rise help researchers to overcome this challenge. First is the unexpected nature of China’s export growth. Even after reform implementation in the 1980s, few predicted how important a role China would come to play in the global economy. China’s share of world manufacturing exports rose only modestly between 1984 and 1990, from 1.2% to 1.9%. In the 1990s, however, its trade expansion began in earnest.

Second is the depth of economic isolation and accompanying economic distortions during the Maoist era, which kept China far inside its production frontier. Between 1952 and 1978, China’s GDP per capita decreased from 59th to 134th out of the 167 countries covered by the Penn World Table. When China’s economic expansion began, it ignited a phase of rapid catch-up growth that in part reflected how far China had fallen relative to the developed world.

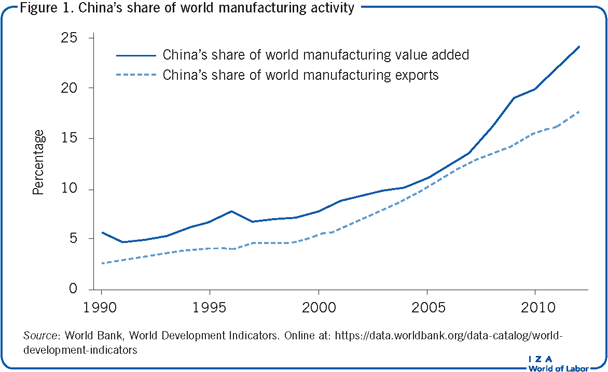

Manufacturing has been the driving force behind China’s economic turnaround. Between 1991 and 2012, China’s share of world manufacturing value added increased six-fold, from 4.1% to 24.0% (Figure 1). China’s stellar growth generated a large positive net global supply shock for manufactured goods, coupled with a large positive net global demand shock for raw materials. Regional and national economies differ greatly in their exposure to these two forces, and the effects of China’s rise are thus likely to vary across locations according to their own patterns of industry specialization.

Industry-level impacts

Taken as a whole, China’s rise is a singular global macroeconomic event, which makes it challenging to empirically identify its consequences. However, the distinct nature of China’s comparative advantage gives rise to substantial sectoral variation (i.e. cross-industry and over time) that can be used for credible identification.

Industrialized countries’ product markets were the first to feel the effects of supply shocks in China. As China’s productive capabilities improved and its trade costs fell, the intensity of competition for US goods increased, inducing a contraction of US industries subject to greater import exposure. Using data on US manufacturing plants for 1977–1997, one study examines the impacts of increased exposure to import competition from low-wage countries [4]. The authors find that over five-year intervals, industries facing larger increases in exposure to trade experience higher rates of plant exit. Among the plants that survive, those in more trade-exposed sectors undergo greater falls in employment and are more likely to switch to a different sector.

A recent study from 2016 provides a complementary analysis that moves the focus to the industry level and extends the data forward in time to cover the period from 1991 to 2011 [5]. The authors exploit an identification strategy that involves instrumenting observed changes in industry import penetration in the US with contemporaneous changes of Chinese imports into other countries [1]. This strategy posits that if numerous rich countries simultaneously substitute Chinese-produced goods within detailed product categories for domestically produced goods or imports from other countries, then China’s comparative advantage in these goods improves (e.g. a fall in price, or in transport or tariff costs, or a rise in the quality of China’s exports). These forces correspond to a supply shock from the perspective of China’s trading partners. Consistent with previous results [4], this study shows that US industries facing rising exposure to Chinese imports experienced sizable contractions in employment, number of establishments, and employment per establishment [5].

These findings make clear that employment in import-competing US industries has shrunk as a result of China’s rapid growth. For researchers, the challenge is to measure the distributional effects and net economic costs and benefits of these labor market impacts. For policymakers, the challenge is to recognize these costs and benefits, while maximizing the latter and mitigating the former. Quantifying these costs and benefits requires exploring mechanisms that are not evident from the basic facts above, specifically:

Do the geographically concentrated industry-level shocks to manufacturing translate into localized employment shocks, or do they dissipate regionally and nationally? If they do have localized incidence, are these effects offset or amplified by local labor market mechanisms?

To what extent are trade-induced reductions in industry employment compensated for by employment gains elsewhere in the economy, potentially outside of trade-impacted regions?

Are wages the main margin of adjustment to trade—as has traditionally been believed—or are effects also seen on overall employment, or both? If trade does affect overall employment, what are the costs to individual workers and to the public at large?

Are workers employed at trade-impacted firms and residing in trade-impacted local labor markets disproportionately affected by trade? Or do these shocks diffuse nationally across workers with comparable skills, thus diluting their direct effects?

Regional employment impacts

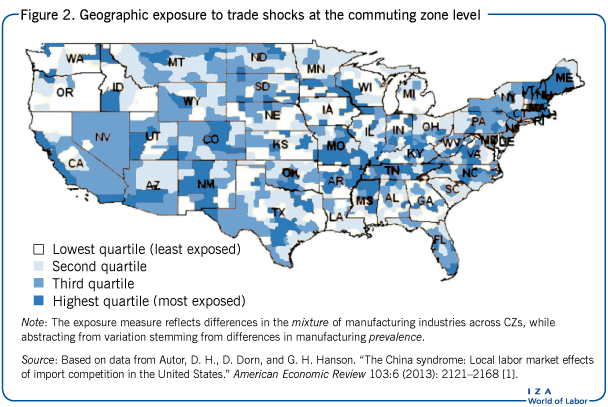

Because manufacturing activity tends to cluster in specific areas of the country, with a region’s manufacturers often concentrating in a narrow set of sub-industries, local exposure to trade varies substantially across locations. Within specific manufacturing regions, there is also wide variation in the industry composition of local firms. To measure regional trade exposure, one of the above-mentioned studies exploits regional industry specialization patterns in the pre-shock period, thereby averting the potential confounding factor created by endogenous adjustment of industry location to concurrent trade shocks [1].

Figure 2 presents the geographic distribution of exposure to increases in Chinese import competition across commuting zones (CZs) between 1991 and 2007. The exposure measure depicted in the figure holds the share of manufacturing in each CZ’s employment to be constant as of 1990. It thus measures import competition for the set of manufacturing industries represented in a location, rather than reflecting the overall prevalence of local manufacturing. Over the period 1990 to 2007, CZs that were more exposed to import competition from China experienced substantially greater reductions in manufacturing employment. Contrary to the established understanding of US labor markets as fluid and flexible, over the course of a decade, trade-induced manufacturing declines in CZs were not offset by sectoral reallocation or labor mobility. Instead, overall CZ employment-to-population rates fell at least equally with manufacturing employment rates, and generally by slightly more.

These results do not support the traditional assumption of the trade literature that local employment effects of sectoral demand shocks are short lived, and, moreover, they also fail to support the assumption that such shocks do not differentially reduce employment rates in directly impacted CZs relative to the national labor market. The fact that these localized effects endure for the span of (at least) a decade suggests that the effects of trade shocks on labor markets are likely amplified by slow and incomplete adjustment. They also reveal that adjustment does not accrue primarily along the wage margin. While one would expect a modest reduction in wage levels among low-skilled workers nationally, sizable falls are instead found in employment rates within trade-impacted local labor markets.

It is also important to note that analyses for Denmark, Norway, and Spain, covering periods from the late 1990s to 2007, find results that are consistent with the US evidence, suggesting that the phenomenon is not exclusive to the US (see for example [6]).

National versus regional impacts

Do the above results indicate that trade-impacted locations suffered employment declines in absolute terms, or simply that they benefited less than trade-insulated locations? This distinction between relative and absolute effects matters: the former covers the distributional effects of trade, whereas the latter deals with the magnitude of the net gains from trade.

The above-mentioned 2016 study assesses whether the seemingly adverse industry and regional impacts are offset by employment responses elsewhere in the economy [5]. The study estimates that if import penetration from China had stopped increasing after 1999, there would have been 560,000 more manufacturing jobs in the US through the year 2011. Actual US manufacturing employment declined by 5.8 million workers from 1999 to 2011, meaning the counterfactual job loss from direct Chinese import competition accounts for 10% of the realized job decline.

Negative shocks to one industry are transmitted to other industries via economic linkages between sectors. For example, rising import competition in the apparel and furniture sectors will cause these “customer” industries to reduce purchases from the “supplier” sectors that provide them with fabric, lumber, and textile and woodworking machinery. Because customers and suppliers often locate near one another, trade-induced employment impacts are likely to be transmitted via linkages to suppliers in the same regional or national market, thus magnifying their aggregate effects.

When manufacturing workers lose their jobs or suffer declines in earnings they will reduce their spending on goods and services. This contraction in demand spreads throughout the economy, dragging down consumption and investment. Offsetting some of these negative demand effects is the notion that workers who exit manufacturing may find jobs elsewhere in the economy, replacing some of the earnings lost in trade-exposed industries. Because aggregate demand and reallocation effect work in opposing directions, their net impact can only be detected on aggregate employment.

Summing over both aggregate demand and reallocation effects, and considering both those industries that are directly exposed to import competition and those that are indirectly exposed via input–output linkages, the analysis in [5] finds that import growth from China between 1999 and 2011 led to an employment reduction of 2.4 million workers. There is little evidence to suggest, however, that employment gains in non-exposed local industries substantially offset these losses. Indeed, the estimated employment decline is actually larger than the 2.0 million job loss estimate when considering only direct and input–output effects.

Wage and transfer impacts

Trade shocks impact more than just the employment margin in labor markets. Workers in trade-exposed CZs experience larger reductions in average weekly wages [3], and these impacts are concentrated among workers in the bottom four wage deciles [7]. Thus, while trade theory has typically emphasized the wage impacts of trade shocks, analysis finds that adjustments at the employment margin might have an even larger quantitative impact on workers’ earnings [3].

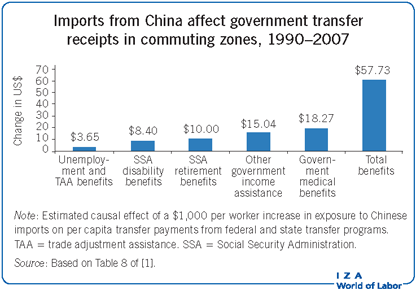

A direct result of reduced employment and wages in trade-exposed local labor markets is a rise in transfer benefits. Perhaps unsurprisingly, CZs that are more trade exposed experience greater increases in per capita payouts of unemployment insurance and trade adjustment assistance (TAA) (see the Illustration, based on [1]), both of which are designed to assist laid-off workers.

This is not just a short-term issue: trade-induced declines in local employment and wages appear to be persistent. As the Illustration shows, CZs that are more trade-exposed see larger per capita growth in publicly provided medical care and government income assistance, indicating that more households are qualifying for income-based health benefits and meeting the threshold for welfare payouts. Trade exposure also contributes to an increase in disability benefits, which are typically associated with permanent exit from the labor force. And finally, retirement benefits also rise in more trade-exposed CZs, suggesting that adverse labor market shocks induce more workers to retire early.

The impact of trade shocks on benefit take-up is sizable: per worker transfer receipts rise by approximately $6 per capita for every extra $100 in local import exposure. Perhaps even less expected are the categories of benefits in which these transfers accrue. TAA, the federal government’s primary program to help workers who lose their jobs due to foreign competition, offers extended unemployment benefits of up to 18 months, where eligible workers may obtain allowances toward relocation, job search, and health care, as long they remain enrolled in a training program. However, despite its intended purpose, TAA has a negligible impact on easing local adjustment to trade shocks. Comparing a CZ at the 75th versus the 25th percentile of trade exposure over the 1991–2007 period, the findings show an average increased per capita take-up of TAA of only $0.23 in the more- versus less-exposed CZ. By contrast, public spending on medical benefits, federal income assistance, and social security retirement and disability benefits grew by more than $45 per capita in the more-exposed CZ, relative to the less-exposed one.

Worker-level impacts

Which types of workers bear the costs of trade adjustment—those employed by trade-impacted firms? Or, are these effects felt equally by all comparably skilled workers in a locality? In a frictionless labor market where workers move quickly across firms, industries, and regions, wages should adjust uniformly within skill groups in response to a trade shock, even if only a subset of industries or regions is directly exposed. If worker mobility is imperfect across jobs and locations, however, trade shocks can have heterogeneous impacts across workers within the same skill groups. Until recently, there has been little evidence on how individual workers adjust to trade shocks.

A 2014 study uses longitudinal data from the US Social Security Administration to analyze the impact of import competition from China on the careers of individual workers [8]. Comparing workers with similar demographic characteristics and previous labor market outcomes, but who differ according to the subsequent trade exposure of their 1991 industry of employment, those initially employed in subsequently trade-exposed industries accumulate substantially lower earnings over the period 1992–2007. Although workers who become trade-exposed due to initial industry affiliation move among jobs at a higher rate than those who are not trade-exposed, this trade-induced job mobility is shown to be insufficient to offset the difference in career earnings between more and less trade-exposed workers.

Why do trade-exposed workers not fully recover earnings losses after changing employers? One possible explanation is that job displacement devalues prior industry-specific human capital, leaving affected workers poorly prepared for their new roles relative to non-displaced workers. Ironically, workers may also suffer subsequent earnings losses because they seek new positions in the industries where they currently possess specific skills—industries that remain exposed to import competition and hence may subject these workers to further job displacement.

Although trade shocks affect both high- and low-wage individuals, there are substantial differences between their patterns of adjustment. Workers whose pre-shock wages are in the top earnings tercile of their age cohort respond primarily by relocating to firms outside the manufacturing sector, and they do not lose earnings relative to their peers who started out in less trade-exposed industries. By contrast, workers in the bottom tercile of pre-shock earnings react by relocating primarily within the manufacturing sector, often remaining in industries that are hit by subsequent increases in import competition. These low-wage workers experience substantial differential earnings losses, as they earn less per year both while working at the initial firm and after relocating to new employers.

Worker-level adjustment patterns in response to Chinese import competition have also been studied for several EU countries, including Denmark, Norway, and the UK (e.g. [9]). As in the US, earnings losses are concentrated among low-skilled workers. These results as well as structural estimates of models with sectoral switching costs suggest that workers in import-competing sectors incur differential adjustment costs in reaction to the China trade shock, depending on initial industry and pre-shock wage levels.

A brief look at the positive side of international trade

These gloomy tidings from the labor market do not imply that trade integration, or China’s rise specifically, have reduced US welfare—and even less so global welfare. On the benefit side, there is no question that rising trade integration has lowered consumer prices in the developed world. Recent work estimates that China’s entry into the World Trade Organization in 2001 reduced the price index for manufactured goods in the US by 7.6% between 2000 and 2006 [10]. Moreover, the expanded ability of firms in high wage countries to offshore production to China may raise productivity for home-country workers, lower the relative price of intermediate goods, and extend the range of final goods that firms are capable of producing. And there is little doubt that China’s rise as an exporter has been central to its extraordinary economic growth, which lifted 680 million Chinese citizens out of poverty between 1981 and 2010 [11]. The expansion of the economic pie from these positives means that, in theory, all countries could compensate those adversely impacted by trade integration to make all individuals better off.

Limitations and gaps

A key limitation of the evidence above is that it considers only the cost side of the cost–benefit equation. While this evidence is unambiguous that workers, firms, and local communities that are directly in the path of rapidly advancing international competition suffer substantial and durable adverse adjustment costs, this article does not provide analogous evidence on the gains experienced by consumers facing lower goods prices, nor does it quantify the production and profit opportunities opened for domestic multinationals. Concretely, it is hard to imagine Apple’s success in conceiving and delivering wildly popular consumer products absent the capability of its primary Chinese supplier, Foxconn, to manufacture these labor-intensive products at relatively low cost and high quality. The correct interpretation of the evidence provided here, therefore, is that rising international competition imposes concentrated costs on a subset of workers and communities—not that this competition is harmful in net for a trading country.

A second gap in understanding is that we know little about the dynamics of trade adjustment. The US-based evidence above indicates that the adjustment process can be sluggish, unfolding over a decade or longer. Recent work studying the labor market effects of Brazil’s rapid reduction in import tariffs in the early 1990s presents an even more troubling picture: alongside slow adjustment, the long-term consequences may include permanently lower productivity, earnings, and formal sector employment in more trade-exposed regions [12]. If this finding bears up broadly—and it is premature to say whether it will do so—it adds urgency to understanding why trade-exposed areas tend not to fully rebound, and to exploring the set of policies and local conditions that can improve the speed and extent of rebound.

This last observation underscores what is perhaps the essential gap in our understanding of the effect of trade on labor markets, which is an extraordinarily limited knowledge of what policies “work” to facilitate trade adjustment, either at the individual level (e.g. wage insurance or training programs), the local geographic level (e.g. subsidizing new business formation or, alternatively, facilitating worker moves to new locations), or the national level (e.g. adopting gradualism versus shock therapy in trade policy). Now that research has unambiguously demonstrated that sharp changes in trade exposure impose substantial adjustment costs on workers, firms, and surrounding communities, it is incumbent on researchers and policymakers to think creatively, rigorously, and experimentally—meaning, using the best tools of social science—to discern what policies serve to maximize the shared gains from trade while minimizing the concentrated brunt of adjustment costs on a subset of citizens.

Summary and policy advice

While policy knowledge is lamentably incomplete, enough is already known to conclude that there is no magic policy that can reap all of the benefits of trade integration while fully shielding workers from the costs of trade adjustment. When industries contract—due to either trade, technological advances, or even shifts in consumer tastes—workers in those industries typically experience considerable economic losses.

Though rigorous evidence is quite limited, there are at least five policy levers that appear promising for mitigating these costs and sharing the gains from trade integration more broadly. First are well-designed trade adjustment assistant programs. In the US, for example, the federal TAA program is difficult for workers to access and places artificial strictures on their re-employment options. Making assistance more accessible, flexible, and supportive rather than constraining of labor market re-entry would be a first constructive step.

A second policy to consider is wage insurance. Workers displaced from career jobs typically have trouble getting back into the labor market and are often understandably reluctant to accept a new job at diminished pay and status. But waiting is costly. The longer workers spend unemployed, the harder re-employment becomes. The simple idea of wage insurance is to ease the economic and psychological pain of transitioning to a new line of work. If a displaced worker must take a pay cut to find a job, a publicly provided wage insurance policy would meet them part way. Workers may quickly move up the wage ladder once re-employed, but if this does not occur, wage insurance affords them months of enhanced pay while they make other adjustments.

A wage subsidy that increases the rewards to otherwise low-wage work is a third policy option. In the US, the Earned Income Tax Credit (EITC) is among the nation’s most significant tools for reducing poverty and encouraging work. Receipt of EITC payments is contingent on having work, and much evidence confirms that the EITC increases both income and employment. But the EITC provides almost no cash assistance or employment incentive to childless workers and non-custodial parents, many of whom are low-wage men. Thus, the EITC excludes a group that is much in need. Expanding the EITC into a generalized “earners’ credit” would assist workers whose earnings have been reduced due to economic forces—such as trade exposure and technological displacement—outside of their individual control.

Developed countries’ experiences with the China Shock also underscore the value of gradualism as a principle for trade policy. There is a natural ebb and flow to labor markets: as older workers retire and younger workers enter, industries are able to change size without disrupting careers. But sharp labor market shocks that convulse entire industries rush this gradual process, imposing steep transitional costs. In short, such shock therapy is rarely wise as labor market policy.

Too often, policy is guided by untested assumptions, stylized economic theories that omit critical details, and a selected set of historical anecdotes that may lack generality entirely. Thus, a fifth policy that policymakers should almost universally embrace is rigorous experimentation to learn what works. Policies should not only be well intentioned but also explicitly engineered to be rigorously evaluated as they go into effect. Experimentation may take the form of random assignment, a phased rollout of program benefits among individuals or communities, or a set of crisp administrative rules that creates clear contrasts in the extent or nature of treatment among different beneficiaries. Policy making is both an art and a science, and the scientific component has advanced considerably over the past decade, as randomized controlled trials have been widely deployed to evaluate and improve economic and social policy. In trade policy, the stakes are high. Not by coincidence, the opportunity for well-designed policy to improve individual and collective outcomes is substantial.

Trade integration offers profound gains for all nations. Reaping them is a worthy policy goal. Yet an appreciation for the concentrated costs trade adjustment imposes on a subset of citizens should caution policymakers to proceed toward that goal with due care.

Acknowledgments

This piece draws extensively on papers co-authored with Daron Acemoglu, David Dorn, Gordon Hanson, and Brendan Price. Sections of the text above are reproduced in whole or part from [3]. The author acknowledges research support from the National Science Foundation (SES-1227334) and the Russell Sage Foundation. He thanks Evan Soltas and the editors of the IZA World of Labor for their assistance with preparation of this article.

Competing interests

The IZA World of Labor project is committed to the IZA Guiding Principles of Research Integrity. The author declares to have observed these principles.

© David H. Autor