Elevator pitch

In the past 25 years, the Chilean labour market has observed a modernisation in terms of its transition to a service economy, but also in terms of its institutional robustness. It has seen a consistent growth in the labour force, driven by women’s entrance in the labour market, and a sustained increase in earnings from salaried work. However, it faces obstacles to drive growth through labour productivity and to ensure that growth translates to better socioeconomic outcomes for workers as a large low-productivity segment persists, also driving informality. These obstacles include lengthy permits, human capital deficits, low R&D investment, as well as slow technological adoption. Solving these issues requires coherent policy making beyond employment and labour policy.

Key findings

Strengths

Chile has seen an increase in labour force participation, driven mostly by women entering the labour market.

There was a sustained increase in real wages in the past 20 years.

Inequality in labour-income has decreased substantially in Chile.

Labour market institutions have been strengthened since 2000.

Weaknesses

Lengthy permits, human capital deficits, low R&D investment, and slow technological adoption are some of the structural obstacles hindering labour productivity.

High levels of informality persist in specific sectors and for specific workers, limiting access to labour protection and social security.

Gender, regional, and income inequality still persist.

There is limited fiscal space for strengthening labour market institutions and for adopting active labour market policies.

Author's main message

Since 2000, the Chilean labour market has grown in size and by now offers opportunities for higher earnings. It has more robust and comprehensive policies and institutions that strengthened worker protections and labour market policies. Challenges persist, particularly in terms of gender inequality, structural unemployment, and pockets of informality as well as low productivity. Demographic change, technological change, climate change, and the general sensitivity of a small and open economy to external shocks will require a continuous process of adaptation that should be based on tripartite social dialogue involving the government, workers, and employers.

Motivation

The 2000-2025 period transformed the Chilean labour market. Owing to the increasing labour force participation of women, the labour market grew faster than expected by population growth alone. Favourable economic conditions allowed average labour earnings to more than triple. Concerted and consistent reforms have strengthened worker protections and labour market institutions, including, among others, an increase in the statutory minimum wage, the establishment of an unemployment insurance scheme and the introduction of different active labour market policies, the consolidation of a robust labour inspection system, as well as a regulatory framework that addresses discrimination and violence. These improvements come on a backdrop of persistent gender and income inequality, increasing structural unemployment and pockets of informality and low productivity. In a context of demographic, productive, and environmental transformation, policies will need to address productivity and inclusion to ensure similar improvements in the future.

Discussion of strengths and weaknesses

Favourable, but increasingly challenging economic context

Between 2000 and 2024, Chile’s per capita GDP (purchasing power parity, ppp, measured in constant 2021 US$,) grew by 42%, reaching over US$ 30,000 in 2024. It is classified as a high-income economy. Growth in this period is characterised by a period of strong growth driven by the commodities boom (2000-2013) and slower rates of growth thereafter. The economy is also sensitive to external shocks, as reflected by the impact of the 1999 and 2008 financial crises and the economic consequences of the Covid-19 pandemic [1]. Chile is a relatively small, open economy highly dependent on the export of commodities (such as copper ore, refined copper, carbonates, molybdenum, and raw copper) as well as agriculture, meat, and fish products [2]. Chile is the fifth largest economy in Latin America and the Caribbean and was the third largest recipient of foreign direct investment in 2023 and fourth in 2024 [3].

Between 2000 and 2025 Chile committed to macroeconomic stability and – with the exception of the Covid-19 crisis – maintained year-to-year inflation rates at around 3%. However, during this period, fiscal space has deteriorated owing to the use of foreign reserves and increased public debt. In fact, the debt-to-GDP ratio has increased steadily from around 5% in 2008 to 41.6% in 2024 owing to higher social expenditure and lower revenue growth [4], [5].

The period 2000-2025 positioned Chile as an important exporter of lithium, wine, and fish products (e.g., salmon), but lack of diversification and investment, as well as structural barriers to lift productivity have hampered continuous economic growth. As in other countries in the region, Chile transitioned to a service economy through a process of premature de-industrialisation [6]. In contrast to the premature de-industrialisation of Mexico and Brazil, for example, Chile transitioned with a highly productive resource sector (e.g., mining) and some evidence of diversification in exports, with a growing volume of manufacturing product exports, including telecommunications products, vehicles, machinery and medicaments, that are not linked to Chile’s abundant natural resources [7].

In parallel, Chile is experiencing an accelerated demographic transition, due to declining fertility rates (currently at 1.59, down from 2.06 in 2000) and longer life expectancy (currently at 82). The percentage of people aged 65 or older increased from 8.1% in 2002 to 14.1% in 2024 [8] and is projected to reach 32.1% in 2050 [9]. In parallel, the percentage of migrants in the population increased from 1.3% in 2002 to 8.8% in 2024 [8]. The period is also marked by an increase in the population holding tertiary degrees, as a result of explicit policies to expand access to this level. However, educational performance has improved slowly and still lags non-Latin American OECD countries, and more than half of adults do not score above the minimum proficiency levels in literacy or numeracy [10], [11].

Overall and female labour force participation compared to other OECD countries

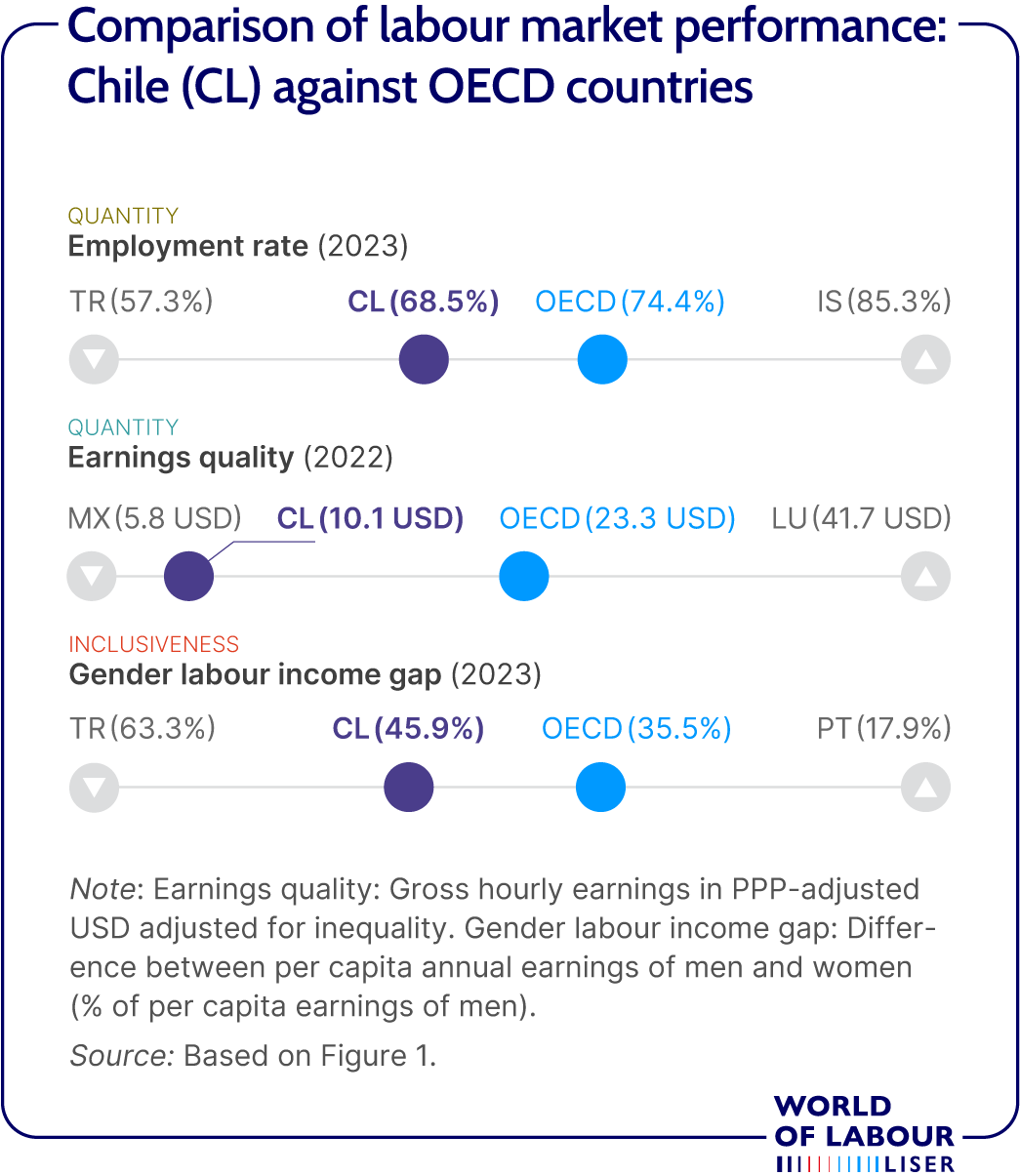

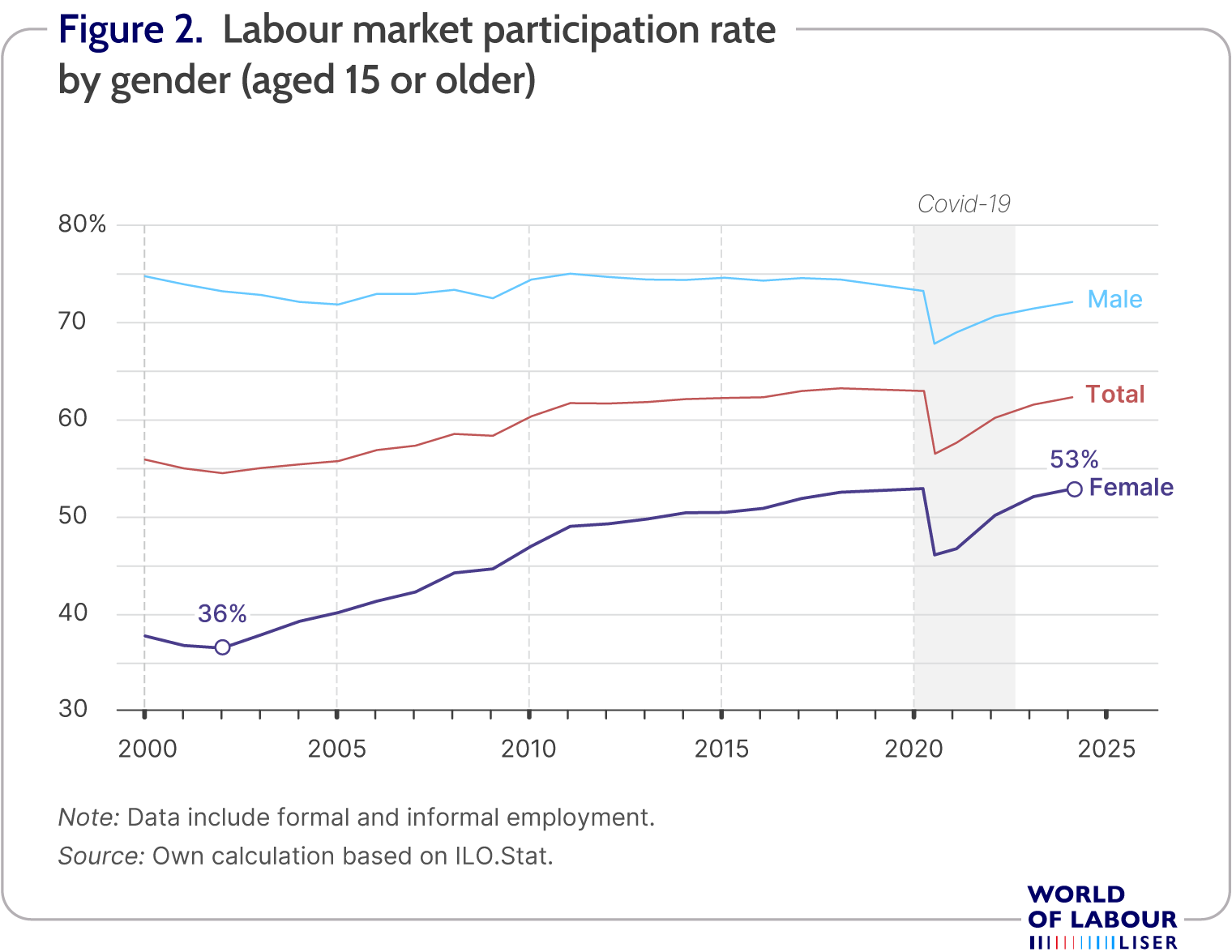

Between 2003 and 2011, the labour force participation grew at an average of 0.8 percentage points per year, driven by an average annual growth in the female participation rate of 1.4 percentage points (Figure 2). Female labour participation rate kept growing, albeit a slower pace up, to 2019. As a result, while roughly 36% of women were in the labour force in 2002, this figure reached 53% in 2024, surpassing pre Covid-19 levels. Female labour participation rates are low compared to other OECD countries, owing to a gender-unequal distribution of care responsibilities and insufficient childcare options [10].

Unemployment reflects structural issues and job mismatch is similar to the OECD average

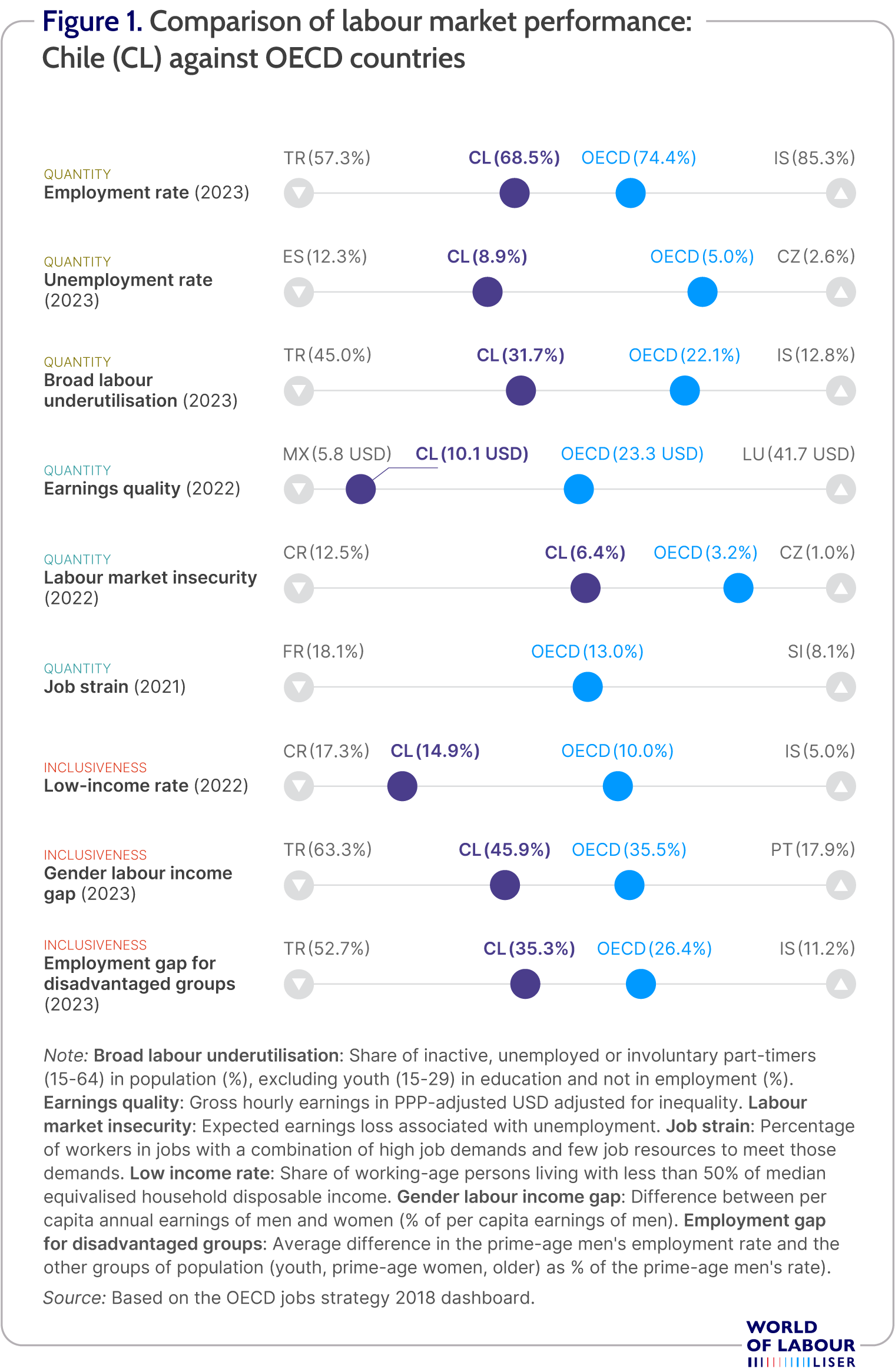

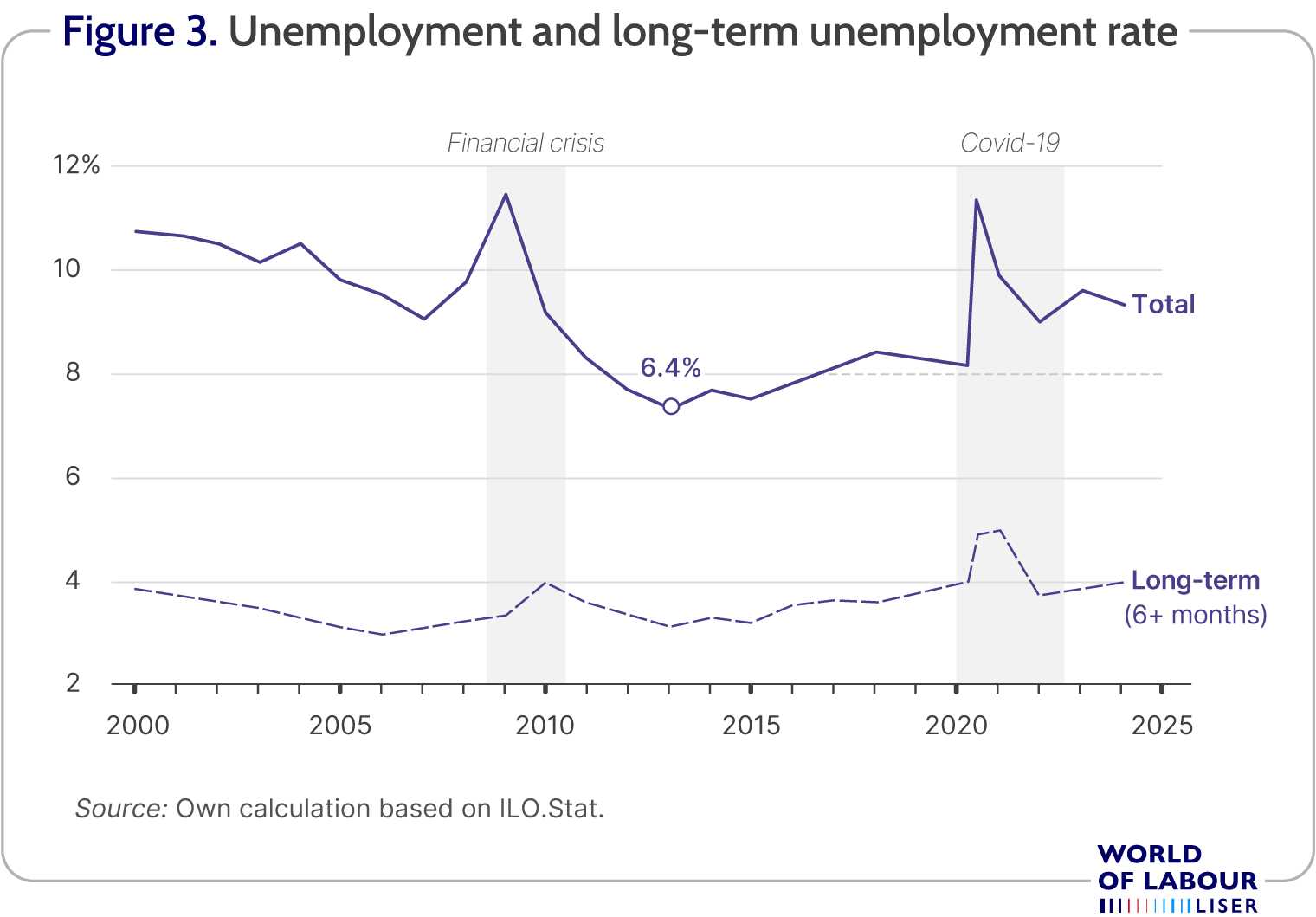

Excepting the peaks that resulted from the financial crisis in 2009 and the Covid-19 crisis in 2020, unemployment rates had been decreasing between 2000 and 2013, reaching a low-point of 6.4%. This trend reverted thereafter, with unemployment rates trending upwards and remaining above 8% after 2020 (Figure 3). Excepting the external shock peaks, unemployment trends closely follow the baseline level of structural unemployment. This baseline rose during the commodities boom (until 2013) and then rose, in line with the decline in total factor productivity growth thereafter [12]. Long-term unemployment, of six months or more, follows a similar trend, with around 2% of the labour force being long-term unemployed over the last 5 years.

Employment mismatch remains close to that of the OECD average. Some 19% of workers have higher educational credentials (qualifications) than their job expects (overqualification) and 35% work in areas unrelated to their field of study (horizontal mismatch) [11].

Real earnings increased, as has the statutory minimum wage, but inequality remains high

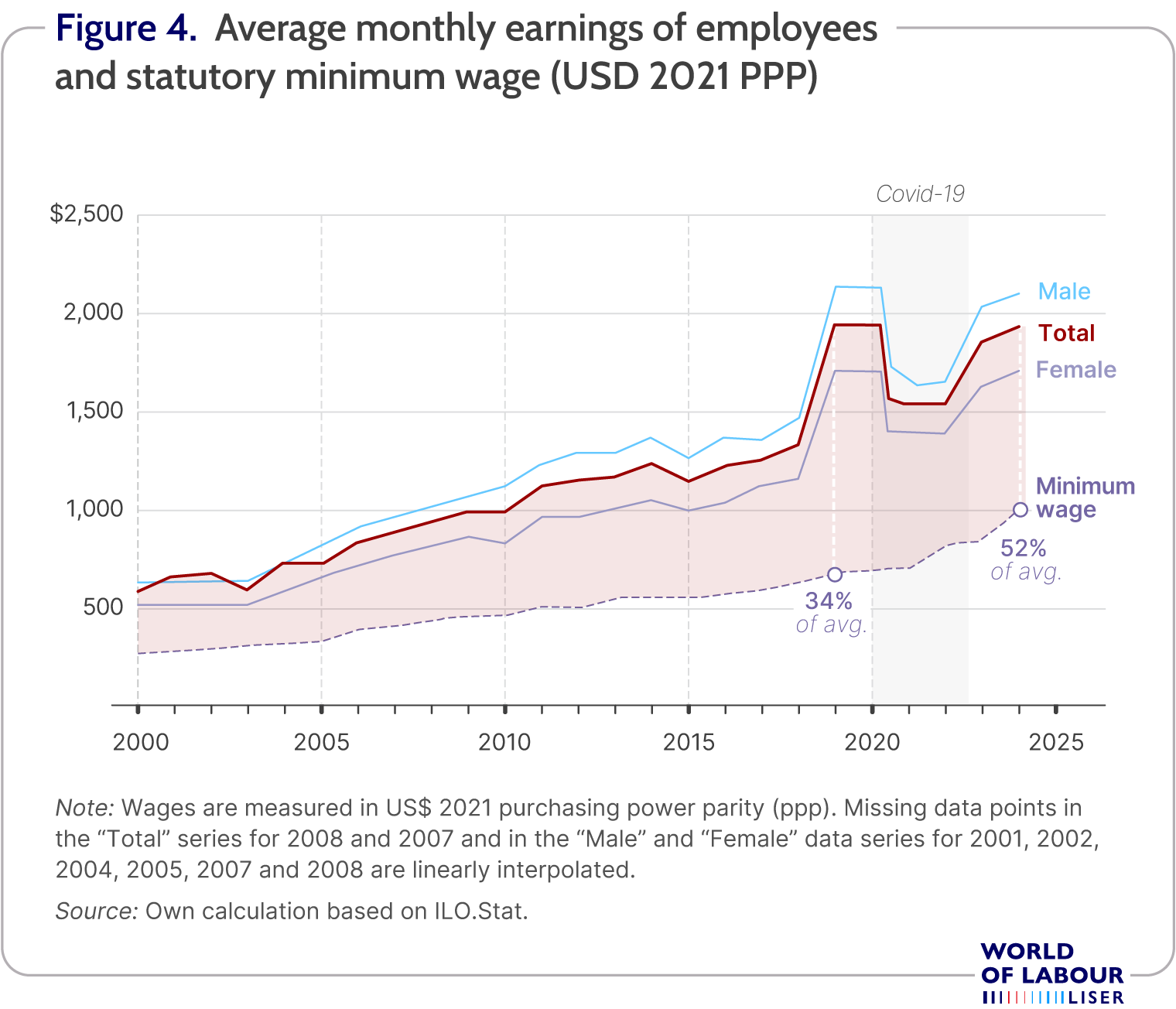

Real earnings for wage workers more than tripled between 2000 and 2025, it rose from US$ 577 (ppp, measured in 2021 US$) to US$ 1,934, with similar increases for men and women (Figure 4). Up until 2019 the statutory minimum wage grew at a slower pace than real earnings. While in the 2000-2019 period real earnings for employees grew by 3.4 times, the statutory minimum wage had grown only by 2.5 times. As of 2021, the minimum wage increased more rapidly so that by 2024 the minimum wage represented about 52% of the average earning for employees (in 2019 it represented 34%,and 45% in 2000). At its 2024 level and compared to the national wage distribution, the statutory minimum wage is high compared to other OECD countries, though this comparison should be made with the caveat that comparatively higher low-salaried informal employment pushes average and median earnings downwards, increasing the minimum wage-to-average earnings ratio [10].

Income inequality in Chile decreased in the 2000-2025 period, with the Gini coefficient, a widely used index for measuring inequality, for household income falling from around 0.51 in 2009 to 0.47 in 2024 [13]. Analyses suggest the tax and redistribution system in Chile could do more to address inequality, as inequality is reduced only by 5% in the county after taking into account cash transfers and other redistribution efforts. This reflects a lower redistributive capacity than in other high-income OECD countries.

The slight decrease in income inequality may stop or even reverse as high-productivity and export-oriented sectors require relatively few workers, are prone to automation, and there are not many other sectors to drive economic growth. The economy in Chile has a high concentration of low-productivity and labour-intensive firms (mostly in the service sector) with a low level of unionisation and collective bargaining coverage, and a relatively high level of informality, as will be discussed further below [14].

Gender inequalities have not necessarily reversed in the 2000-2025 period either. While the male-to-female labour participation gap has closed, it remains high compared to the OECD average owing, in part, to an unequal distribution of care responsibilities and low availability of childcare options [10]. Moreover, women’s access to senior leadership positions in the private sector remains relatively limited compared to other OECD countries, although some improvement has been observed in public employment following the introduction of a board gender quota in 2018. While women’s and men’s wages grew at a similar pace in the period, the gender pay gap, after adjusting for hours worked, occupation and disability status, stands at 16% and is one of the widest in Latin America [15].

Regional inequalities also exist, though they are lower than observed in 2009. While the poverty rate – as estimated by the national standards – reached 29% in the Región de la Araucanía in 2024, it was only 10% in the Región de Magallanes. The national rate is 17,3% with the capital region observing a poverty rate of 13% [13].

Labour market modernisation amid slowing productivity and persistent informality

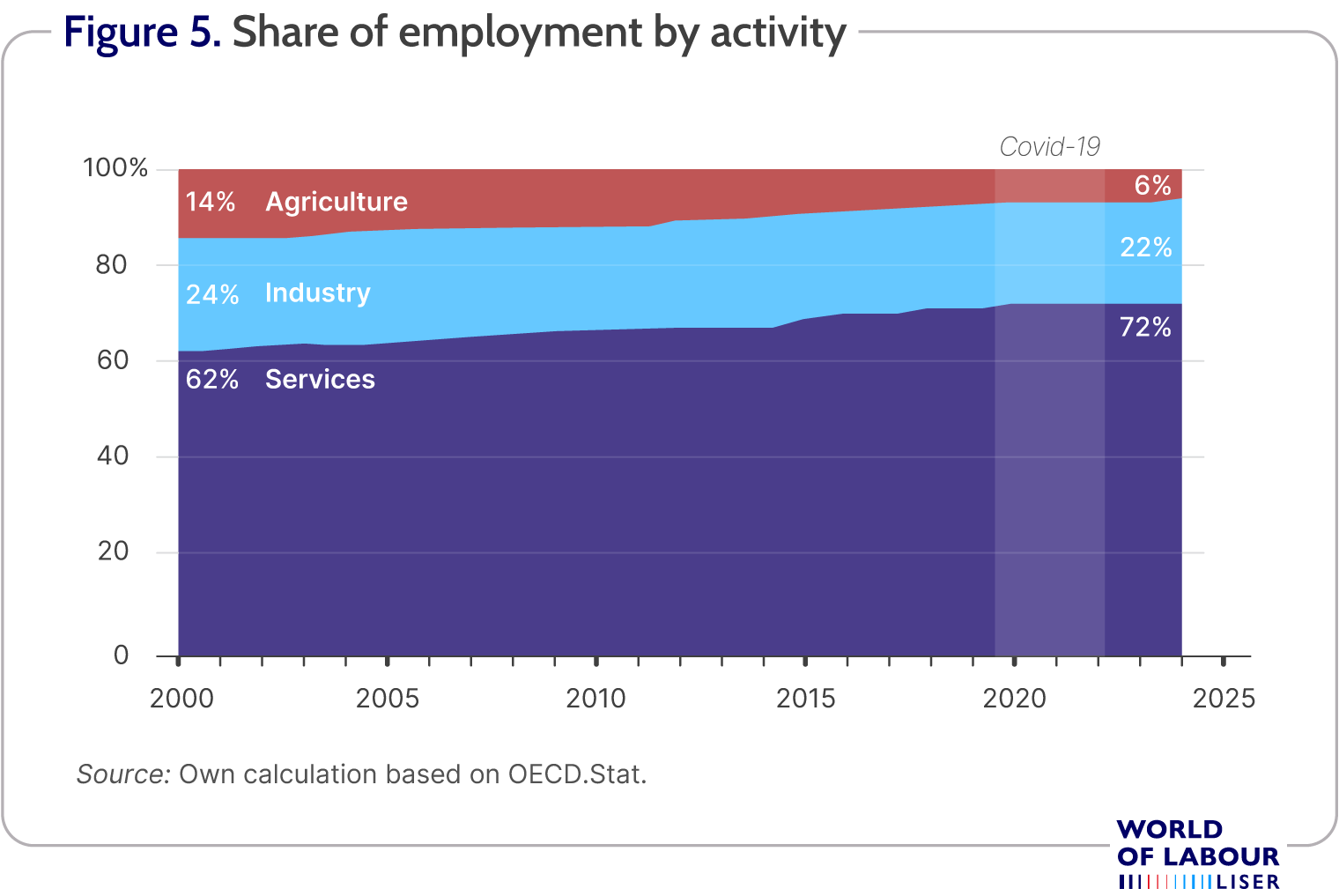

Between 2000 and 2025, the importance of the service sector in the economy grew significantly. According to official data from the National Institute of Statistics, employment shifted towards the service sector, with the share of total employment rising from 62% to 72%. By contrast, employment in the agriculture sector declined from 14% to 6%. Contrary to the economic activity trends highlighted earlier, employment in the industry sector saw a reduction of less than 2 percentage points in past 25 years (Figure 5). Coincidentally, employment in households fell from 5.2% in 2013 to 2.9% in 2024, resulting from a continuous decrease until 2019 and a sharp fall during the Covid-19 years (pre-2013 levels are stable at around 5% of employment).

Labour productivity stands at around half of that of the OECD average. Between 2000 and 2007 Chile registered gains in labour productivity in the order of 2.5% per year which slowed to 1.6% annual growth in the 2010s and stagnated in the following years [16]. According to OECD data and after an increase observed after the Covid-19 crisis, Chile is one of the five OECD countries which expects a reduction in labour productivity to 2027. These labour productivity trends take place in a context of a high number of working hours per year. Annual working hours in Chile (currently at 1.963) are only below those in Costa Rica, Mexico, and South Korea, yet 211 hours above the OECD average.

Informal employment has been decreasing slowly since 2018 for both men and women and stands at 26.9% in 2024. Though official measurement started in 2018, estimates point to a decrease from 40% in 2010 [10]. Informal employment is especially high in agriculture (42%), construction (36%), commercial activities (33%), transport (32%), restaurant and lodging services (31%), arts, entertainment and recreation (41%), as well as in domestic work (59%). Own-account workers account for around half of all informal workers (51%). Though informality in the private sector stands at 15%, informal workers in the private sector account for around a third (35%) of all informal workers.

Strengthened worker protections and labour market institutions

Chile's labour market regulatory framework developed throughout the 2000-2025 period. It ratified nine ILO conventions including the fundamental conventions on worst forms of child labour, on occupational safety and health, sectoral conventions on mining, domestic workers, and public sector workers as well as the maritime labour convention, the indigenous and tribal people convention, and the violence and harassment convention.

Additionally, and especially since 2016, the country's labour legislation evolved with changes to its labour relations framework, anti-discrimination provisions, the regulation of subcontracting, digital platform work, telework and the right to disconnect, a reduction in weekly working hours from 44 to 40, the penalisation of harassment and violence at work, the promotion of disability inclusion, the modernisation of the labour inspectorate, stronger work-family conciliation through the expansion of maternity leave and the creation of paternity leave, special pay for Sunday and bank holiday work, provisions for workers with care responsibilities, and the institutionalisation of tripartite dialogue through the Consejo Superior Laboral.

The unemployment insurance now complements different active labour market programmes (e.g., youth and women employment subsidies, training and intermediation services) which are expected to be strengthened and better coordinated with the creation of the Division of Employment within the Ministry in 2022. The regular production employment prospection analyses has, for example, begun to inform policy and budget allocation, as well as the reformulation of employment subsidies and the debate on worker training schemes.

Throughout the 2013 to 2019 period, the OECD's index of employment protection, which evaluates the regulations on the dismissal of workers on regular and temporary contracts and the hiring of workers on temporary contracts, held steady at 2.34, slightly higher than the OECD average of 2.28 to 2.27.

Looking ahead: fostering labour productivity and adapting to contextual factors

While the relatively low labour productivity levels put constraints on accelerating economic growth and the segmentation of high-performing, capital-intensive firms versus low-performing, labour-intensive firms limit the possibility of translating growth to improved social outcomes and inclusion through salaried work. Barriers to growth in labour and general productivity, particularly outside the mining sector vary and include skills gaps, low female labour force participation, low R&D investment, low interconnectedness, infrastructure deficiencies, lengthy and complex regulatory burden, as well as limited financial options to scale innovation [10], [16], [17].

These obstacles to productivity growth compound to the challenges of adapting to a changing environment driven by population ageing, technological change, climate change, and the general sensitivity of a relatively small and open economy to external shocks. The capacity to adapt to these changes will take place in a context of more limited fiscal space, and higher structural unemployment levels than in the 2010s, as well as the need to strengthen worker protections for the large segment of the working population in informality, especially own-account workers. Examples of the tensions surrounding an ageing workforce are that employment transitions are particularly difficult for workers aged 55 or older [18].

Though the period saw a general strengthening of the institutional architecture governing employment and employment relations, it is still subject to political shifts. Many of the institutions can be strengthened or weakened by government decisions, which is why they could benefit from governance by independent, tripartite bodies, as suggested for the minimum wage setting mechanisms to take into account both the broader context (e.g., productivity levels, labour market conditions) as effects (e.g., on employment, inequality and informality) [10].

Limitations and gaps

Though Chile’s statistical infrastructure is robust and independent, trends dating back to 2000 face limitations owing to breaks in the series and the adoption of new measurement standards [18]. Though care is taken to ensure the comparability of the series, certain gaps exist (e.g., in the measurement of employment by sector at a fine level or across regions). Similarly, certain indicators have limited series (e.g., informality prior to 2018) unless models and simulations are incorporated. Historical analyses at the national level can only go back as far as 1986; previous analyses can only draw on surveys in the capital region.

Analytical gaps persist in understanding the labour-market related obstacles to productivity growth, particularly when contrasting the growth in educational attainment and slow growth of student and adult skill levels.

Summary and policy advice

The Chilean labour market has observed a modernisation in terms of its transition to a service economy, but also in terms of its institutional robustness. It has seen a consistent growth in the labour force, driven by women’s entrance in the labour market, and a sustained increase in earnings from salaried work. It faces obstacles to drive growth through labour productivity and to ensure that growth translates into better socioeconomic outcomes for workers as a large low-productivity segment persists, also driving informality.

Policy should focus on structural factors limiting labour productivity growth and unemployment without weaking labour market institutions. As many of the root causes are of structural nature, policy should go beyond employment and labour aspects and encompass coherence with industrial, sectoral and skills policy. Policy focus should also continue to promote female labour force participation, including through the provision of better childcare services. Unionisation and collective bargaining coverage remain low, and their strengthening could promote greater labour income equality and inclusion. A close monitoring of demographic change, technological adoption, climate trends, and their respective impact on the labour market could help adapt quickly to external shocks, reducing scarring effects on vulnerable population groups.

Acknowledgments

The authors thank the anonymous referee(s) and the World of Labour editors for helpful suggestions on earlier drafts. The author appreciates the comments received by Yukiko Arai, Sonia Gontero and Gerhard Reinecke of the ILO Office for the Southern Cone of Latin America.

Competing interests

The World of Labour project is committed to the European Code of Conduct in Research Integrity. The author declares to have observed the principles outlined in the code.

© Guillermo Montt