Elevator pitch

Remittances have risen spectacularly in recent decades, capturing the attention of researchers and policymakers and spurring debate on their pros and cons. Remittances can improve the well-being of family members left behind and boost the economies of receiving countries. They can also create a culture of dependency in the receiving country, lowering labor force participation, promoting conspicuous consumption, and slowing economic growth. A better understanding of their impacts is needed in order to formulate specific policy measures that will enable developing economies to get the greatest benefit from these monetary inflows.

Key findings

Pros

Remittances can increase the well-being of receiving households by smoothing consumption and improving living conditions.

Remittances can facilitate the accumulation of human capital by making possible improved sanitary conditions, healthier life styles, proper healthcare, and greater educational attainment.

Remittances can ease the credit constraints of unbanked households in poor rural areas, facilitate asset accumulation and business investments, promote financial literacy, and reduce poverty.

Cons

Remittances can reduce labor supply and create a culture of dependency that inhibits economic growth.

Remittances can increase the consumption of nontradable goods, raise their prices, appreciate the real exchange rate, and decrease exports, thus damaging the receiving country’s competitiveness in world markets.

Remittances can be curtailed, along with international migration, by escalating anti- immigrant sentiment and tougher enforcement practices in host countries, including the US and many in Europe and the Gulf region.

Author's main message

Remittance flows have the potential to greatly improve the livelihoods of receiving households by smoothing their consumption and enabling investments in human and other capital. At an aggregate level in the receiving country, they facilitate economic stability, improve creditworthiness, and can attract investments to promote economic growth and reduce poverty. The main challenges remain how best to assess the impacts of remittances and how to design policies that facilitate the transmission and productive use of remittance flows while taking into account the idiosyncrasies of each country. Possible policies range from easing capital controls to reforming immigration policy.

Motivation

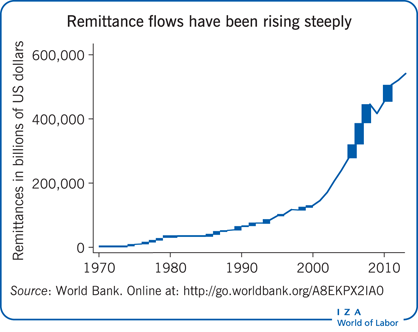

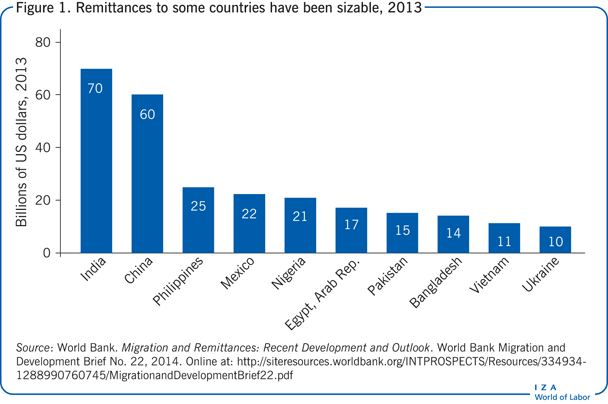

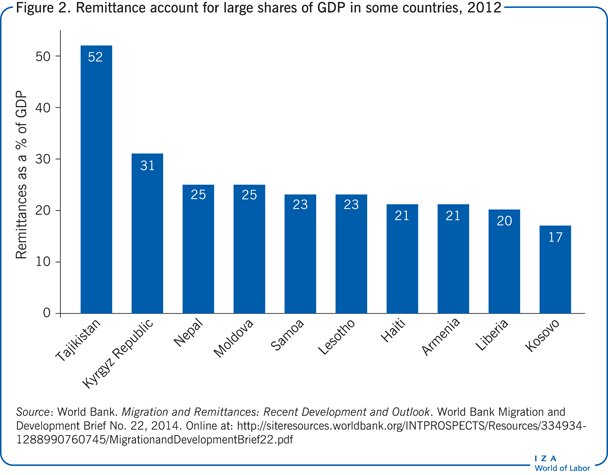

Remittances, the repatriated earnings of emigrant workers, have grown remarkably in recent decades, while proving considerably less volatile and more reliable than other sources of foreign exchange, such as foreign direct investment and official development aid. The economic relevance of these monetary inflows is evident from the raw figures (Figure 1). In both India and China remittances exceeded $50 billion in 2013. Yet, these sources of foreign exchange are particularly important for small developing economies; they accounted for more than 50% of gross domestic product (GDP) in Tajikistan in 2012, for example (Figure 2).

The growth in remittance flows has fed a long-standing debate on their positive and negative consequences. On the one hand, some studies have pointed out how remittances have hurt the receiving economy by cultivating a culture of dependency that reduces labor supply and promotes conspicuous consumption. At a macro-economic level, remittances have been found to hurt exchange rates and the export sector through the so-called Dutch disease. On the other hand, many studies have noted that these monetary flows can greatly improve the livelihoods of receiving households by promoting education, health and capital investments. At an aggregate level, positive effects include economic stability, improved creditworthiness, and greater access to foreign capital that can boost economic growth. The empirical evidence remains mixed.

Discussion of pros and cons

Are remittances good or bad?

Assessing the impact of remittances is difficult. Receiving remittances is not a random event. Households that receive remittances are likely to exhibit certain characteristics, such as having family members abroad, or specific needs owing to their composition (perhaps they have more dependent children or elderly members). As a result, it becomes cumbersome to separate the impact of remittances from that of emigration or other household characteristics that could themselves be the byproduct of remittance flows (endogeneity).

Researchers have tried to cope with that challenge in various ways, such as using instrumental variable methods (using variables that do not belong in the equation, but are highly correlated with remittances), exploiting natural experiments, and designing randomized experiments. All these methods have limitations, such as the difficulty of finding valid instruments, the high cost of randomized experiments at a larger scale, and the limited applicability of the findings to other migrant groups or countries. As a result of the distinct methodologies used and the differences in geographic and temporal settings in which the studies take place, findings on the pros and cons of remittance flows vary considerably.

What are some of the cons?

Concerns about the economic and social implications of remittance flows have been raised by a variety of studies. While any impacts at an individual or household level may ultimately show up at an aggregate level, the concerns are classified here for discussion into those found when examining individuals and households (referred to as “micro-level” impacts) and those found while working with country-level data (“macro-level” impacts).

Micro-level impacts (individual and households)

At the micro level the two primary concerns in the literature are dependency, along with lower labor force participation, and conspicuous consumption. At the household level, the most widely cited concern has been that remittances—a source of non-labor income—may breed dependency by discouraging receiving household members from working. Indeed, remittances may ease budget constraints, raise reservation wages, and through an income effect, reduce the employment likelihood and hours worked by individuals receiving remittances. However, remittances might also be accompanied by a substitution effect if household members have an incentive to cut back on their labor supply in order to continue to receive the non-labor income flows, which is a distortion of household labor supply decisions. It is this substitution effect that preoccupies many researchers and policymakers.

While a number of studies have pointed out that remittances curtail the labor force participation of household members, others show that the impacts of remittances on labor supply can be complex, varying by gender and type of employment, formal or informal [1]. Specifically, hours of work in marginal types of employment might decrease, whereas hours of work in self-employment might increase. In other instances, remittance flows have been found to reduce child labor while increasing the labor supply of older household members [2]. As such, it is important to keep track of the type of labor that is being reduced and for whom.

Another concern expressed in the literature is that remittances change consumption patterns among receiving family members, often resulting in the purchase of nonessential goods manufactured outside local communities or the acquisition of items that require an increased use of energy. While some of these changes may be good—lower demand for fuel wood, for example—others might prove negative for the global environment.

Macro-level impacts (country-level)

At a more aggregated level, there are two main areas of concern that have found broad empirical support in the literature: moral hazard problems and the impact of remittances on the prices of domestically produced goods and exchange rates.

Moral hazard problems are related to the potential reduction in labor supply, the development of conspicuous consumption patterns, and the inability to develop a culture of saving that can enable future investments and growth. Still, while there is evidence of labor supply reductions following the receipt of remittance flows, evidence of reductions in economic growth are scarcer, and analyses typically fail to take into account the long-term investment of remittance flows in human capital.

Another impact of remittance flows at an aggregate level that has long received attention is their effect on exchange rates through increases in the prices of domestically produced goods. Reminiscent of the effects shown for Dutch disease or resource boom models, some researchers have argued that remittances can increase the consumption of nontradable goods and the prices of domestically produced goods, reduce exports, and damage the country’s competitiveness in world markets. While there is some evidence of such effects among smaller economies, as in some Latin American and Caribbean economies [3], the evidence is harder to find for larger economies.

What are some of the pros?

Micro-level impacts (individual and households)

Of the micro-level impacts discussed in the literature, three are most prominent: increases in individual well-being, in human capital accumulation, and in savings, investment, and financial literacy.

Perhaps one of the main benefits of remittance flows is that they can stabilize household income, thereby improving living conditions and increasing well-being. Remittances appear to be responsive to income shortfalls and, in that way, have the potential to smooth household income [4]. Studies have shown how remittances have helped smooth household income in Mexico, particularly among households that face greater saving constraints and are therefore exposed to greater risks.

Accumulation of human capital through better health and higher educational attainment is another important benefit of remittances. A broad literature has shown how the human capital gains of household members who emigrate and the remittance flows that follow can significantly improve health outcomes and health care access in receiving households by easing financial constraints. For instance, remittances have been associated with lower mortality rates, higher birth weights, and improved living and sanitary conditions in the receiving household through the acquisition of durable goods, such as refrigerators, stoves, and washing machines.

Similarly, remittance flows have been shown to have positive impacts on educational investments in children left behind. To better assess the causal effect of remittances, a study exploited the depreciation that followed the 1997 Asian financial crisis and the corresponding increase in remittance flows to examine the impact on children’s schooling and labor [2]. It found an increase in the share of children being schooled and a corresponding decrease in the hours children worked.

Others have tried to separate the potentially positive impacts of remittance flows on the educational investments in children from the disruptive effect that the emigration of a father or mother might have on the educational attainment and performance of children left behind. When the household head migrates, some of the older children might have to quit school and start working to help support the household. In other instances, researchers have argued that the emigration of household members might lower the incentives for young children to invest in an education at home if they foresee emigrating in the future. The imperfect portability of human capital from one country to another might drive that decision.

A way of distinguishing these impacts is to compare the effect of remittance flows in families with migrant household members to the impact of remittance flows received from more distant family members or friends in households without emigrants [5]. The findings seem to confirm the positive impact of remittances on the educational attainment of children documented by the earlier literature. In some instances, the most disadvantaged groups of children also seem to benefit, as is the case with secondary school-age children for whom the opportunity cost of not working is higher, higher-order birth children who do not receive the same benefits as the first-born child, and girls. In that regard, remittances can play an important role in leveling the field by providing better educational opportunities for those children.

Perhaps one of the most examined impacts of remittance flows is on investment. A number of studies have examined how remittances can ease the credit constraints faced by households that lack access to financial markets and thus can facilitate the accumulation of assets and business investments (such as in land, tools, and new businesses) and increase financial literacy [6].

For the most part, remittance flows seem to increase savings, facilitate access to financial institutions, and promote financial literacy and investment. However, an important challenge in much of this literature, particularly when focusing on business investments, remains the confounding impacts of human capital acquired during the migration process (new business ideas, production, and sale strategies, for example) and the impacts of remittance flows themselves. To further complicate matters, the endogeneity of remittance flows and business investments can be troublesome—for example, if migrants are more likely to send money home when there is a family business in anticipation of future bequests. In that case, it is the business that attracts the remittance flows rather than the remittance flows that make the business possible. Finally, unlike educational investments or consumption, business investments are not a frequent occurrence, thus presenting an additional data challenge.

Macro-level impacts (country-level)

Two impacts at the country level have been extensively explored: the contribution of remittances to economic stability and to a country’s creditworthiness.

A key characteristic of remittance flows is their resilience and countercyclical nature, both of which promote economic stability. A number of studies exploiting natural experiments, such as natural disasters and financial crises, to examine the response of remittance flows to greater economic need at home find that remittances tend to increase in response to economic need and to decline otherwise [2], [4].

Finally, to the extent that remittances constitute a large and stable source of foreign exchange, they have been shown to help prevent sudden current account reversals during periods of economic instability, improve a country’s credit rating, and facilitate the inflow of new investments [7]. Recognizing this potential, a number of countries have developed active emigration policies and the institutional framework needed to educate and orientate potential migrants before they emigrate in order to promote remittance inflows and investment in the home country.

Some more contentious impacts of remittances

While there is some consensus on the outcomes just discussed, there is still much debate on the potential impact of remittances on other spheres, such as whether remittances boost economic growth and reduce poverty and inequality. Some studies have found positive impacts of remittance flows on economic growth and poverty reduction, while others remain skeptical. For example, a widely cited study concludes that remittances slow economic growth [8]. However, the study has been criticized for ignoring the intermediate impact of remittances on labor supply and capital formation. Perhaps slow-growing countries experience more outmigration and receive more remittance flows. Once again, identifying the direction of causality remains an empirical challenge.

Some studies have also argued that remittance inflows reduce inequality by helping people in rural and poor areas. However, the evidence varies widely by country, with many studies showing declines in inequality in Mexico, but not in Pakistan or the Philippines, among other countries. Differences are also found in the selection into emigration in each country. One study argues that remittances may worsen income inequality if international migration is confined to the elite [9]. That connection could explain why remittance flows prove to be more income equalizing in Mexico, where emigrants are neither at the very bottom nor the top of the skill distribution, than in other countries.

Some nuances: Level versus volatility and predictability

For the most part, the remittance literature has focused on the impact of remittance flows, paying much less attention to other aspects surrounding the receipt of the money inflows, such as their frequency, volatility, and uncertainty. Yet, the ultimate impacts of remittances on labor supply or asset accumulation, for example, depend not only on the amount of money received, but also on the regularity. Households that receive remittance flows on a regular basis might better be able to coordinate remittance receipts with necessary expenditures and therefore might be more likely to reduce their labor supply. In contrast, households that receive remittance flows irregularly would not be able to rely on those flows to meet necessary expenses and so might be more reluctant to change their labor supply.

Some studies focusing on Mexico have found that increases in the volatility of remittance income raise the employment likelihood of men and women in receiving households, as well as the hours worked by employed women [10]. To the extent that men are more likely to be working full-time than women, women might be better able to respond flexibly to remittance income volatility by increasing their hours of work. In other words, female labor supply may be used as a buffer against increases in the volatility of remittance inflows.

Similarly, the decision to use remittance receipts for consumption or investment might depend in part on their regularity and predictability. Households that receive remittances on a predictable basis will be better able to coordinate their day-to-day expenditure and consumption needs with the receipt of remittances. In contrast, households that receive remittances on an unpredictable basis are more likely to view the inflows as nonpermanent and, therefore, are less likely to include them in their consumption planning. As a result, they might have a greater tendency to save the remittance inflows.

Studies for Mexico have found that a one standard deviation increase in the uncertainty of remittance income raises the likelihood of household spending on asset accumulation by about two percentage points while raising the share of household spending going to asset accumulation by 4–9% [11]. Their findings suggest that both the level and predictability of remittance inflows should receive full attention in the design of policies for maximizing the benefits from remittance inflows into developing economies.

Policies affecting remittance flows

Because policies may affect the magnitude, stability, and destination of remittance inflows (and vice versa) and because of the many potentially important impacts of remittances, analyses of their economic impact often seek to inform the design of policies to improve the impact on remittance inflows. Developing countries that are recipients of remittance flows can select from a wide range of policies to facilitate those flows:

Relaxing exchange and capital controls, as well as the operation of domestic banks overseas, to facilitate international transactions by banks and financial institutions.

Providing identification cards that allow migrants access to financial institutions. An example is the matrícula consular for Mexicans living in the US. The matrícula consular has been recognized by financial institutions in the US as an acceptable form of identification for resident aliens, facilitating access to banking services for undocumented Mexican migrants. While most remittance flows continue to be sent through money transmission firms, such as Western Union or MoneyGram, facilitating access to banking services lets migrants take advantage of the more secure and less expensive transmission methods offered by banks while helping them build a relationship with the bank. Developing that relationship is key in gaining financial literacy and access to credit for asset accumulation and investments.

Creating matching fund programs and promoting hometown associations that invest remittance flows in their home communities.

Establishing the necessary institutional arrangements to educate, inform, and orient potential migrants before they emigrate to improve their well-being in the host country and facilitate the flow of remittance funds back home.

Host countries, too, can facilitate this alternative source of foreign exchange flows:

Reducing remitting costs, so that more of the flows go to the intended recipients. This policy has already received considerable attention. While costs still vary widely, from as low as 2% for remittance flows originating from Russia to as high as 18–20% for flows from Japan, countries have succeeded in reducing remitting costs, which today average around 8%.

Affecting migration and remittance flows through immigration policy. For example, immigration policies that facilitate the permanent settlement of migrants, such as the 1986 US Immigration Reform and Control Act, could strongly affect remittance flows, though the outcome may be ambiguous. On the one hand, legalizing the status of migrants could facilitate their travel back and forth between the home and host country, allowing migrants to stay in touch with their family back home and facilitating the flow of remittances. On the other hand, remittance flows could drop if migrants no longer envision their migration as temporary and settle permanently into their new life, gradually losing touch with their family back home [12].

Affecting migration and remittance flows through stronger enforcement of stringent immigration laws. Stronger enforcement, as has occurred in the US since September 2011, can reduce the number of undocumented immigrants, restrict the cyclicality of migration flows, and limit employment opportunities for undocumented immigrants. Recent studies show how increased enforcement reduces the share of migrants sending money home. However, legal immigrants tend to increase their money outflows enough to offset any reductions in remittances from undocumented immigrants. For example, the average dollar amount remitted per Mexican immigrant in the US has risen in the midst of increased uncertainty, thus protecting one of the least volatile sources of income in the developing world [13].

Limitations and gaps

Overall, when considering the impact of remittance flows on receiving economies, it is important to keep in mind research limitations that undoubtedly shape study findings. Most studies focus on a specific country or region at a particular point in time. Because of cultural differences and country idiosyncrasies, some of the empirical evidence based on a specific country might not generalize to other economies. For instance, even if remittances cause Dutch disease in some Latin American and Caribbean economies, they might not do so in a large economy like Mexico. Furthermore, remittance impacts might vary over time within a given country depending, among other things, on its policies and the characteristics of emigrants.

Further, studies have applied many different methodologies as they try to get at the causal impacts of remittance flows. These differences undoubtedly contribute to the diversity of findings. Some studies implement randomized trials, some exploit natural experiments, some rely on instrumental variable methods, and others do none of these. And getting at the causal impact of remittances remains a challenge given concerns about the endogeneity of remittances, the difficulty of separating the impacts of migration from those of remittances, and the selection of migrants into emigration and remitting, to mention a few.

Summary and policy advice

Remittance flows—estimated at $404 billion in 2013—are expected to continue to grow along with international migration flows. Because of the size and stability of these flows, remittances have the potential to help developing countries in a number of ways, from improving their economic stability and creditworthiness to attracting funds for asset accumulation and investments in human capital. The main challenge remains the design of policies that can promote these flows and their productive use while taking into account the idiosyncrasies of each country at a particular point in time.

In addition, while research has expanded the understanding of remittance flows and their impacts, there is more to learn about how the periodicity and predictability of the flows affect their impact. These aspects of remittance flows could prove crucial to the design of policies that can help developing economies attract the most remittance flows and use them most productively.

Finally, given the current political environment and escalating anti-immigrant sentiment, strict enforcement of immigration laws, and abusive treatment of immigrants in many remittance-sending countries, more research is needed on how immigration policies in host countries affect the flow of this vital source of foreign exchange for many developing economies.

Acknowledgments

The author thanks two anonymous referees and the IZA World of Labor editors for many helpful suggestions on earlier drafts.

Competing interests

The IZA World of Labor project is committed to the IZA Guiding Principles of Research Integrity. The author declares to have observed these principles.

© Catalina Amuedo-Dorantes