Elevator pitch

Most OECD countries have recently introduced product market reforms with the objective of lowering barriers to entry and increasing competition in many sectors, such as telecommunications, utilities, and transport. The timing and extent of regulatory reform have varied significantly, starting in the US in the early 1980s and in the mid-1990s in many European countries. Will these developments improve economic performance in terms of creating jobs, fostering investment, and encouraging innovations—all of which are important factors for policymakers?

Key findings

Pros

Pro-competitive product market reforms generate significant employment in OECD countries when labor market policies are tight.

Product market reforms generally lead to labor market reforms, enhancing the overall positive effect on employment.

Reducing entry barriers significantly increases the investment rate, which is important because investment often incorporates technologies.

Product market reform is likely to positively affect sectors that are close to the technological frontier, where incumbents, by innovating, can escape the threat of entry of new firms.

Cons

It may take time for the positive effects of product market reform on employment to be felt and short-term employment losses can occur, generating opposition to the reform.

With deregulation there are winners, but also losers. The concentration of losses may make reforms more politically difficult to implement.

Evidence on the effect of product market reform on innovation is mixed; in sectors that are far from the technological frontier (i.e. not technologically advanced), the reduction of expected monopoly profits can hinder innovation.

Author's main message

Product market reform stimulates firms’ demand for labor and their willingness to invest. While this creates jobs in the long term, short-term effects are debatable. Favorable long-term employment outcomes are more likely if labor markets are rigid and are enhanced by product market deregulations that encourage labor market reforms. While empirical results suggest that lower entry barriers stimulate investment, evidence on the impact on innovation is mixed. Lower monopoly profits decrease the incentive to innovate, whereas greater competitive pressure forces incumbents to innovate more. The effect on innovation is more likely to be beneficial the closer firms in an industry are to the technological frontier.

Motivation

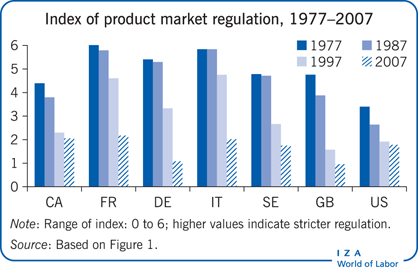

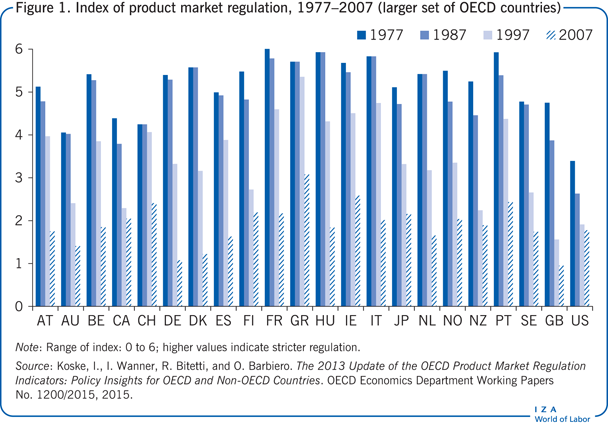

In the last three decades numerous industrial sectors have undergone a significant shift toward less restrictive regulation. One important component of this deregulation has been a lowering of barriers to entry. For instance, OECD countries have seen substantial deregulation in services, particularly within telecommunication, utilities, and transport since the 1980s. The timing and extent of regulatory reform has, however, varied considerably, with the US beginning earlier than other countries, and starting from a lower level. As shown in Figure 1, the UK, Canada, New Zealand, and some Scandinavian countries began slightly later, in the mid/late 1980s. In much of the rest of Europe, as well as Australia, market reform occurred from the mid/late 1990s, and has been less decisive in nations such as France, Italy, and Greece. Moreover, regulatory reform has often been accompanied by privatization, leading to a situation in which the share of output produced by public enterprises tends to decrease. Finally, manufacturing and other sectors have witnessed reduced restrictions on foreign direct investment.

This paper investigates the extent to which product market reform has affected employment, investment in physical capital, and innovation by firms; additional detail can be found in [1]. We do not address a related question: what has been the effect of regulatory reform on aggregate and industry productivity? Notwithstanding its importance, we leave others to provide a detailed answer to that question.

Discussion of pros and cons

What is product market regulation?

The term “product market regulation” includes various dimensions that influence firms’ behavior in different ways. A key aspect is how regulation contributes, either directly or indirectly, to the magnitude of existing entry barriers and, through this, on the markup of prices over marginal costs. Regulation also affects behavior by restricting entrepreneurial choices with respect to inputs, supply, or pricing.

Many of these regulations are justified as attempts to address market failures due to the existence of natural monopolies, informational frictions, or externalities. Whether or not this is the main reason that explains the existence of regulations is debatable. However, there is no doubt that they tend to restrict competition, which has potentially important economic consequences. Yet, there are conceptual and practical problems in measuring the different dimensions of regulation that are relevant in shaping the competitive environment [1].

International institutions such as the OECD and the World Bank or research institutes such as the Fraser Institute provide a variety of measures of entry barriers. In some cases, detailed information is available on legal limitations to the number of companies in potentially competitive markets and on rules about vertical integration of network industries between the natural monopoly and competitive segments (such as the distribution and production of electricity, respectively). Information is also often available on controls imposed by government agencies on the price charged to consumers as well as on the importance of public ownership for specific sectors in OECD countries.

Historically, a large portion of production in sectors such as utilities, transport, and even manufacturing took place within state-owned or local government-owned enterprises. So product market regulatory reforms during the last few decades have often been accompanied by privatization. The disappearance or reduced importance of dominant, publically-owned players, which often have flexible budget constraints, constitute a noticeable reduction in entry barriers.

For manufacturing, the measurement of entry barriers relies on public ownership data, information about restrictions on foreign direct investment, and, at times, on tariff and non-tariff barriers. The effects of tariff reductions and globalization are not, however, the focus of this review. For the retail sector, regulation tightness is usually approximated by the strength of zoning restrictions that limit the entry of large stores and/or restrict their size.

A general measure of entry barriers at the country level is also contained in quantitative or qualitative information on the overall business climate, particularly regarding the ease of starting a new business, provided by international organizations or research institutes, such as the World Bank or the Fraser Institute. This includes the number of required procedures, the time involved, and the related costs. This cross-country information, together with more detailed studies of deregulation episodes in a specific industry and country, have been used by researchers to study the impact of product market reform on economic performance.

Product market reform influences employment

What are the theoretical arguments behind the idea that policy changes that increase competition in product markets lead to an increase in employment? Changes in competitive environments are typically summarized by changes in the markup of price over cost: a more competitive environment implies that the markup will be smaller, resulting in lower prices. Smaller markups raise the demand for labor, which, everything else being equal, results in greater employment. This argument oversimplifies the issue, but it is not overtly misleading.

At a deeper level, markup changes reflect how easy or difficult it is for firms to enter a given market: higher barriers are associated with higher markups and profits for firms. One study analyses the impact of product and labor market regulation on employment and wages under the assumption that firms are identical and imperfectly competitive. For these firms, labor is the only factor of production and both the product and labor markets are considered non-competitive [2]. In this context, a product market reform is modeled as either an increase in the degree of substitutability between goods, or as a decrease in market entry costs. Both will lead to a decrease in the markup due to increased competition.

The effect of a product market reform is shown to differ in the short versus the long term [2]. In the short term, an increase in the degree of substitutability between goods will lead to lower markups, increased employment, and higher real wages. However, no long-term effect is observed because the reduced markups cause some firms to exit the market. This exit compensates for the increase in employment experienced by each single firm. In contrast, product market reforms that lead to a decrease in entry costs also have long-term effects. The entry of new firms is associated with a lower markup as well as with higher employment and an increase in real wages [1]. The fact that policies that affect the cost of entry are the only ones to exhibit long-term effects justifies why they have received the greatest attention.

The model presented in [2] has been extended in several dimensions in [3], allowing for a more complex specification of what workers would earn if they did not work for the firm that employs them. The updated model also provides more in-depth analysis of the relationship between product and labor market reform, both theoretically and empirically. The key result of this extension is that product market deregulation is more effective in situations where the labor market is more rigid, as summarized by a greater bargaining power of trade unions, for instance. The intuition is that in conditions where unions’ bargaining power is low, real wages will also be low and employment will be near the full employment level. In this case, product market deregulation that decreases markups has only small effects on employment. However, if unions’ bargaining power is high, and if employment is far from full employment, the potential for reforms to have a greater impact on employment is enhanced [3].

Several empirical contributions have used cross-country panel data to analyze the effect of product market regulation on employment or unemployment. In these studies, researchers typically estimate an employment or unemployment rate equation while controlling for cyclical factors and for labor market policies and institutions; in some cases, they also allow for an interaction between product and labor market regulation. Most studies find that product market regulation decreases employment (or increases unemployment). However, there is disagreement on whether product market deregulation is more effective in highly regulated and more unionized labor markets, or in more lightly regulated ones with lower union density or coverage [1]. For instance, high labor market regulation is shown to enhance the effect of product market deregulation in [4], while both [5] and [6] find the opposite.

Recent evidence is based on a dynamic specification of the employment rate equation for the business sector in OECD countries. Country specifics and trends are allowed for, as well as the fact that policies themselves respond to the economic environment (i.e. they are endogenous) [3]. Gains from reducing entry barriers to product markets appear positive and greater when labor markets are highly regulated. This is important from a policy perspective because it implies that in situations where labor market regulation is high, and where introducing more flexibility may prove to be politically difficult, deregulating product markets is an attractive option, as it leads to an increase in employment [3].

Evidence based on summary measures of labor market policies, which include both employment protection and the generosity of welfare benefits, shows that domestic product market deregulation leads to a decline in the bargaining power of workers by promoting the deregulation of labor markets or by affecting union density and coverage [1], [3]. This is consistent with the idea that when product market reform leads to a reduction of the monopoly profits that firms and workers can share, the incentive to capture those rents through unions or state regulation decreases.

As there is evidence that at least some dimensions of labor market regulations and unionization exert negative impacts on employment (i.e. destroy jobs), this additional channel enhances the positive effect of product market deregulation on job creation, delivering a “double dividend” with respect to employment gains.

Furthermore, evidence shows that excessive product market regulation has a negative effect on job creation for particular sectors in specific countries. For instance, commercial zoning restrictions in France, which affect the entry of larger stores, are associated with weaker job creation (and higher prices) [7]. Lowering entry barriers, conversely, stimulates job creation. This is the result of two opposing forces, in which the second one dominates. On the one hand, larger stores are likely to be more productive, which leads to lower employment for a given level of output. On the other hand, lower prices generate greater product demand and increase employment.

Most of the studies reviewed so far typically include a variable that captures business cycle fluctuation. By netting out the effects of cyclical fluctuations, they probably come closer to capturing the long-term effect of product market regulation on economic outcomes. However, changes in product market regulation may also induce interesting effects in the short term; moreover, the short-term and long-term effects may differ from each other. This issue has been explored in the context of both a theoretical and empirical model of product and labor market regulation [8]. Empirical evidence shows that a reduction in barriers to entry first generates an increase in unemployment. However, this increase is reversed after two years, so that unemployment decreases in the long term. The fact that it may take time for reforms to pay off is an important result that should receive due consideration and may explain the difficulty in introducing reform measures.

Another important issue in assessing the effect of product market reform is that it creates winners and losers across industries. For instance, the removal of protections and the reduction of entry barriers from an upstream sector producing, for example, steel may negatively affect profits, wages, and employment of steel workers. However, the resulting reduction in markups and steel prices will reduce the costs to downstream steel users, leading to potentially favorable employment effects in those sectors.

Similar considerations are relevant regarding the knock-on effects of entry barrier reductions in the provision of services. Although the focus is not on employment, but rather on value-added growth, productivity, and export performance, it has been shown that lower service regulation is beneficial in downstream industries, particularly if they are service-intensive [9].

It is important to note that it may be difficult to overcome political obstacles to reform if the losses from deregulation are concentrated on specific groups, while the gains, though potentially large in the aggregate, are spread out across many players.

Product market reform and investment

In addition to its effect on employment, product market regulation may influence investment in physical assets (plant, machinery, and structures). Interesting evidence, using country and sector time varying information on regulation in the telecommunications, utilities, and transport sectors is used to assess regulation’s effect on the accumulation of capital [10].

Understanding investment behavior is crucial for many reasons, including the fact that process innovations are often embodied by new capital goods; investment is thus a means by which technological innovation diffuses through the economy. As we have already argued, product market regulation impacts the markup size by altering, for instance, entry barriers. Moreover, regulation can also influence the costs that existing firms face when expanding their capital stock. Regulatory reform that decreases markup or capital adjustment costs leads to an increase in the demand for capital, and hence in the amount of investments made by firms.

There may, however, also be contrary forces at work. For instance, in certain sectors, regulation may impose a ceiling on potential rates of return. If such a ceiling is binding, removal of the constraint may reduce the demand for capital. Moreover, deregulation is sometimes accompanied by privatization. As a dominant publicly-owned player’s role is reduced, entry barriers decline. However, public enterprises are often heavy investors, either because of political mandates or because of incentives to over-expand by firms’ managers. Reduced investment by the public sector may therefore occur. Ultimately, which effect dominates is an empirical question. One relevant empirical work examines investment in non-manufacturing industries (e.g. energy, utilities, communication, and transport) in OECD countries that have experienced profound changes in their regulatory framework [10]. The results suggest that reducing regulation has a significant and sizable positive effect on the investment rate, particularly if the regulation affects barriers to entry. The results prove robust when considering numerous variations and controls. Changes in the importance of public ownership do not affect investment significantly. Finally, deeper and more decisive deregulations seem to have larger favorable marginal impacts on investment. Moreover, the impact of further deregulation is greater in a more deregulated environment [10].

Studies that focus on liberalization episodes in specific sectors provide further evidence on the effect of product market regulation on investment. For instance, evidence has been presented on the relaxation of limits to the opening of large stores in Italy, using the fact that retail sector entry regulation was decentralized at the regional level [11]. The results suggest that reducing entry barriers stimulates investment in information and telecommunication technologies, helping logistics and inventory management to become more efficient. In other words, lower entry barriers encourage the diffusion of new technologies across locations. Moreover, in areas with stricter entry regulation, lower productivity and higher margins are observed, leading to higher prices.

Do product market reforms foster innovation?

Product market reforms may not only affect investment in physical capital, but also investment in innovations. Recent research formalizes the idea that economic growth is a process of creative destruction in which there are both winners and losers. This is based on the assumption that the introduction of new processes and products is associated with the destruction of monopoly profits associated with the old processes and products. If product and factor market regulations hinder the reallocation of production factors from low- to high-return activities, this can lead to adverse effects on innovation activity as well as on the economy’s aggregate growth performance [1].

However, contrasting forces may influence the effect of greater competition on innovation. To start with, innovation activity is primarily driven by the aim of achieving monopoly profits on new products (or processes) while they are protected by patent laws or by secrecy. If monopoly profits decrease as a result of regulatory reforms, the pace of innovation and growth may likewise be reduced. Furthermore, the degree of market power affects firms’ ability to innovate, since it allows them to accumulate profits that can be used to finance innovation in subsequent years. Funds generated internally through retained profits, which are not distributed as dividends, are crucial given the presence of information asymmetries, which may make it costly or difficult to obtain external funds from financial markets for risky innovation activities that are difficult to evaluate. Indeed, most models from the 1990s that analyze the research and development decisions by firms and their effect on growth indicate that rent reductions caused by regulatory changes adversely affect firms’ incentives to innovate [1].

Nevertheless, in more recent models, incumbent firms also innovate (rather than just newcomers) [12]. In these models, the difference between post and pre-innovation monopoly profits determines the incentive to innovate. Greater competition reduces both, but if the pre-innovation profits decrease more than the post-innovation profits, this fosters innovation. Essentially, competition stimulates innovation due to the threat of (or actual) entry of newcomers into a market, which provides incentives for incumbents to innovate in order to escape competition. This effect is expected to be greater in industries where firms with similar production costs (“neck-and-neck” sectors) compete. This suggests that competition is more likely to stimulate innovation and productivity growth in industries or countries that are situated close to the technological frontier (i.e. technologically advanced), while the opposite holds true for industries or countries that are far from the frontier [3].

Firm-level evidence for the UK suggests that the relationship between competition and innovation at the industry level has an inverted U shape indicating that increases in competition have a positive effect on innovation when starting from a low level of competition, but that the effect becomes negative if one starts from an already high level of competition [12]. Moreover, there is evidence showing that the more “neck-and-neck” the competition in an industry is (with firms more similar in terms of production costs), the more strongly an increase in competition will foster innovation.

Detailed results on the impact of product market reforms on innovation are limited to only one country, the UK, and are based on what happened to the markup following the implementation of reforms that originated from The European Single Market Program, large-scale privatization, and investigations by the UK antitrust authority. Other contributions that are based on variations in product market regulation over time and across countries have typically focused on research and development (R&D) investment as a measure of innovation because it is more readily available. The downside, however, is that R&D does not represent the only input in the innovation process and, even if it did, records of R&D intensity may not capture changes in its effectiveness.

Cross-country evidence on the effect of (time varying) product market regulation on R&D through changes in the markup reveals that the markup has a positive and significant effect on R&D [13] for most countries. The results suggest that fewer barriers to starting a business, lower tariff rates, and lower regulatory trade barriers are all associated with a lower markup and, as a result, with lower levels of R&D in the business sector or in manufacturing. However, they are very sensitive to the selection of countries included in the sample. As such, the results’ sensitivity to country selection should be investigated further.

Limitations and gaps

In sum, although much is known about the effects of product market deregulation, several issues still deserve further investigation. Product market deregulation has been introduced with varying speeds in different countries, with distinctive institutional settings, and at different levels of development. Moreover, product market deregulation has sometimes been accompanied by other reforms, such as labor market deregulation and financial deregulation. Hence, more work is required to understand how the effect of product market deregulation depends upon the initial conditions in which it takes place, such as the level of development and the overall quality of governance in a given country. To do so, it will be necessary to enhance data collection and documentation of product market reform efforts, particularly for non-OECD countries. Furthermore, a better understanding of potential interactions with other elements of reform “packages” is needed to see whether or not the various elements can, and actually do, enhance each other.

Finally, the dynamic effects of product market deregulation should be investigated further to assess whether there are tradeoffs between the short term and the long term. The timing of any observed positive effect is important because it may affect the political feasibility of reforms, for instance when long-term employment gains are accompanied by short-term losses.

Summary and policy advice

Product market reforms introduced in the last decades in OECD countries have, on the whole, led to an expansion of investment and employment, as the evidence suggests. This is particularly true if reforms are given sufficient time for their effects to fully materialize. Evidence also indicates that employment effects are more pronounced when labor markets are rigid. Moreover, product market reform can act as a substitute for labor market deregulation, and can actually increase the probability that the latter may occur in the future.

The effect of product market reforms on innovation must be more finely qualified due to the different forces at work. Whether product market deregulation spurs innovation or not depends upon the initial level of profits, and upon how close the firms in an industry are to the technological frontier. In more neck-and-neck industries it is more likely that an increase in competition generated by product market reforms will stimulate innovation.

In sum, policymakers can view product market reform as an effective way of spurring investment, improving employment outcomes, and spurring innovation, so long as sufficient consideration is given to the short- versus long-term effects, and so long as existing institutional features of the labor market and industry structure are appropriately understood before any policy is implemented.

Acknowledgments

The author thanks an anonymous referee and the IZA World of Labor editors for many helpful suggestions on earlier drafts. Previous work of the author contains a larger number of background references for the material presented here and has been used extensively in all major parts of this article [1].

Competing interests

The IZA World of Labor project is committed to the IZA Guiding Principles of Research Integrity. The author declares to have observed these principles.

© Fabio Schiantarelli