Elevator pitch

Persistent unemployment after recessions and the policies required to bring it down are the subject of an ongoing debate. One view suggests there are fundamental changes in the labor market that imply a long-term higher rate of unemployment, requiring the implementation of structural policy reforms. The alternative view is that the slow recovery of the economy is due to cyclic reasons coming from lack of demand which prevents unemployment from falling quickly. Knowing whether higher unemployment is caused by structural change in the labor market or whether the problem is cyclic determines how effective policy can be in addressing the problem.

Key findings

Pros

Most of the large increase in unemployment during the 2007−2009 recession appears to be cyclic, not structural.

Those industries that experienced the most significant increase in unemployment during the recession also experienced the largest declines as the unemployment rate fell.

Demographic groups experiencing greater unemployment during a recession are those employed in highly cyclical industries.

The degree of mismatch across industries and occupations is pro-cyclic, rising during the recession and falling during the recovery.

Evidence suggests mean wages decline during a recession indicating lower labor demand rather than a structural shift in labor supply.

Cons

Vacancy rates are high relative to unemployment rates during the recovery from a recession.

Labor mobility is lower during recessions.

The ratio of long-term unemployed to the total number of unemployed rose dramatically in the 2007−2009 recession.

It is difficult to determine whether a recession is cyclic or structural while it is underway, but there are indicators that make this possible.

Author's main message

The optimal macro policy response to a negative shock is quite different depending on whether unemployment is structural or cyclic. Monetary policy is an inappropriate tool for addressing structural problems, but may be relevant for cyclical unemployment. The high unemployment during the 2007−2009 recession in the US is primarily cyclic. This does not imply that monetary policy will be effective; only that it is not ruled out as a possible tool.

Motivation

When a recession hits an economy, policymakers want to take actions. Designing the optimal response to a negative shock requires a deep understanding of the mechanisms through which the economy and, in particular, its labor market operates. The speed with which the economy recovers depends on the recession’s severity, the way it is managed, and the design of labor market institutions. During most recessions, especially the most severe ones, there is a debate about the extent to which there are fundamental changes in the labor market that imply a long-term higher rate of unemployment than the one prevailing in the past. The alternative view is that a slow recovery of the economy is cyclic, coming from lack of demand, which prevents unemployment from falling to the pre-recession level.

This debate was particularly heated in the US during the 2007−2009 recession, because unemployment rates in the US are traditionally below those of Europe. However, during this recession, the US unemployment rate rose above most of the countries in Europe. The issue of whether high unemployment is a structural or a cyclical phenomenon is important for guiding policy. If there is structural change in the labor market that causes a higher long-term unemployment rate, then polices addressing these structural problems are required to reduce unemployment. If instead the problem is purely cyclic, then monetary policy may be effective in addressing the problem.

The aim of this paper is to help policymakers to decide whether unemployment during an economic downturn is a cyclic phenomenon by using a set of indicators. The analysis presents empirical findings considering the US experience during and after the 2007−2009 recession as a case study. The paper also highlights limitations and gaps in the literature, and concludes with a brief summary and a discussion for the role of policy.

Discussion of pros and cons

Structural factors explaining higher unemployment rates

Prolonged periods of high unemployment rates may suggest that a structural change has occurred, causing a higher natural rate of unemployment.

Existing literature focuses on a number of structural factors that can explain the increase in the unemployment rate. These include:

changes in the composition of the unemployed, the demographic composition of the labor force, or the industrial composition;

higher mismatch between the skills of unemployed workers and available vacancies, or the geographic location of workers and available jobs; and

supply shifts stemming perhaps from reduced incentives through extended unemployment benefits.

Compositional shifts

Changes in the unemployment rate come about because of compositional shifts in the economy, which might be labeled structural, and changes in the group specific unemployment rates, which might be labeled cyclical [1]. Compositional changes refer to changes in the weight of different groups in the economy. For example, in a number of countries, manufacturing has declined as a share of the labor force (for example, the US), the proportion of females has risen, while the labor force has aged and become better educated. In addition, some of these changes might have a cyclical component. For example, the relative share of construction might be lower during downturns, affecting low-skilled men disproportionately more than women or high-skilled workers.

The empirical literature on the importance of compositional changes in explaining higher unemployment rates mainly focuses on the recession of 2007−2009. A 2012 study using US data investigates how much of the change in the unemployment rate can be explained by changes in the composition of the workforce [1]. The findings suggest that the changing relative importance of the various groups as a proportion of the labor force account for only a very small share of the changes in unemployment rates from 2007−2009. Almost all of the changes are within-group. For example, during the 2007−2009 recession, male unemployment rates rose more than female rates, primarily because men dominate construction and manufacturing sectors with higher-than-average increases in unemployment. However, men and women have very similar unemployment. Even if the share of women in the labor market had changed significantly, this cannot account for any part of the increase in unemployment rates between 2007 and 2009. A similar conclusion is drawn with regard to changing industrial composition. Almost all of the action is in increasing within-industry unemployment rates, not in changes in the composition of different industries over time [1]. Moreover, a few industries, notably construction and manufacturing, had very sharp increases in unemployment in 2007−2009, but the same industries also experienced the sharpest decreases between 2009 and 2012.

The most important finding from the analysis of the composition of unemployment is that those industries that experienced the most significant increase in unemployment during the recession were the ones that experienced the largest declines as the unemployment rate fell [1]. This is inconsistent with the structural explanation that would imply displaced workers in high-unemployment industries are the slowest, not the fastest, to become re-employed.

These findings suggest that no significant structural shift occurred during the 2007−2009 recession and that, for the most part, it appears to resemble earlier recessions [1].

Mismatch

A mismatch occurs when the vacancies available in an industry, occupation, or location do not match the skills of the available workers. Most of the logic behind structural impediments in the labor market relates to mismatch. When there is mismatch, a change in the skill composition of the workforce (or skill requirements of the jobs available) is required to reduce unemployment. For example, there may be many unemployed construction workers but few vacancies in construction while there are few unemployed health care workers but many vacancies in health care. Mismatch problems are not easily remedied by central banks, as they cannot bring about fundamental changes in the skill and/or industrial structure [1].

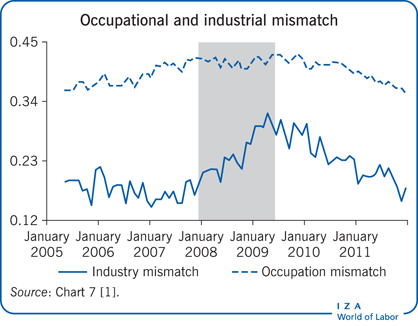

Industry and occupational mismatch

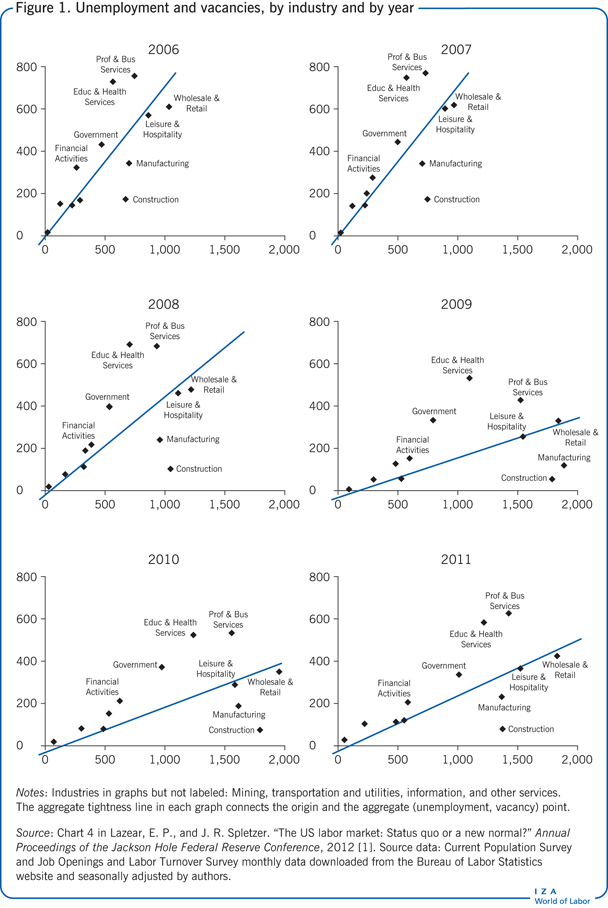

The degree of mismatch in the US is measured using vacancy and unemployment data [1]. Figure 1 shows the allocation of vacancies and unemployment across industries in the US from 2006−2011. As the recession hits, the ratio of vacancies to unemployed falls (flattened line from the origin) as both the number of unemployed rises and the vacancies decline. It is worth noting, however, that the four industries to the left of the aggregate tightness line in 2006 are to the left in every year, and the four industries to the right of the aggregate tightness line in 2006 are to the right in every year [1].

Mismatch is highly pro-cyclic, rising during the 2001 recession, falling during the expansion of the mid-2000s, rising through most of the 2007−2009 recession, and then falling since the end of the recession in June 2009 [1] (see Illustration). Although mismatch increases during recessions, the industrial mismatch index in late 2011 is at the same level as before the 2007−2009 recession. Even though the average level of unemployment in 2011 is almost double the average level of unemployment in 2007, the percentage of unemployed persons mismatched across industries is the same in the two time periods. Furthermore, the industrial composition of mismatch in December 2007 is very similar to the one in November 2011, indicating that the decline in mismatch during the past several years is symmetrical to the rapid increase during the onset of the recession. Occupation mismatch is higher than industrial mismatch and exhibits much less business cycle sensitivity than does industrial mismatch. However, with industrial mismatch the occupational mismatch index has returned to its pre-recession level [1]. Similar results are found in other studies looking at industrial mismatch [2], and occupational mismatch [3]: mismatch increased but, starting in 2009, it has declined.

Geographic mismatch

Reduced matching efficiency may also result from mismatch between the geographic location of available workers and jobs. Geographic mismatch may be particularly relevant to the 2007−2009 recession because unemployed workers whose home values drop below the amounts they owe on their mortgages may face a “housing lock,” which leads to lower labor mobility. Evidence for the US suggests no increase in geographic mismatch during the 2007−2009 recession [2], [3]. In addition, findings using mobility data are not consistent with the view of reduced match efficiency because of the “housing lock.” Although geographic mobility declined during the recession for both owners and renters, the fall was primarily among renters, not owners [1].

During the 2007−2009 recession the average level of unemployment increased not because of mismatch, but because all industries and occupations had more unemployed and fewer vacancies. The conclusion is that changes in mismatch are cyclical, rather than structural. The change over time does not seem to reflect any permanent shift in the labor market that happened in an abrupt manner, nor does the industrial mismatch analysis suggest the shifts will persist [1].

Supply shifts

Changes in the price of non-work might be another potential structural cause of higher unemployment rates in all industries. Expansions in safety net programs during recessions, such as the availability of extended unemployment insurance benefits, even if desirable, reduce the value of work relative to leisure. As a consequence, most of the decline in work hours during the 2007−2009 recession has been suggested to be a result of government-induced distortions that reduced the value of work [4]. More generous benefits received during unemployment increase the implicit tax on work, which is defined as the extra taxes paid and subsidies forgone as the result of working. But other empirical evidence suggests that such a supply shift cannot account for the bulk of higher unemployment rates [5], [6]. The impact of extended insurance benefits on the unemployment rate was found to be about 0.8 of a percentage point in one study, while another finds that it was only 0.3 of a percentage point, with more than half of this due to increased labor force participation among those who would in any case not be employed [5], [6]. Other estimates range from 0.7 of a percentage point to a maximum of 1.7 percentage points. Additionally, there is no sign of mean wages being bid up when examined in terms of education, age, geography, or industry [7]. Instead, wages have fallen rather than risen, which suggests that there is not a decline in labor supply.

It is difficult to believe that a reduced incentive to work does not result in some increased unemployment. The issue of how large this factor is in explaining the high and prolonged unemployment of the 2007−2009 recession and slow recovery remains uncertain.

Long-term unemployment

Changes in the profile of unemployment duration may also be associated with structural changes in the labor market. For example, benefit extensions may reduce search effort and skill, while geographic mismatch may lengthen unemployment duration through a reduced exit rate from unemployment. However, longer unemployment duration is also expected when labor demand is weak.

In the case of the US during the 2007−2009 recession and its aftermath, the ratio of long-term unemployed to total unemployed was higher than in prior recessions, including recessions with comparable unemployment rates. For example, in June 2012, those unemployed for 27 weeks or more accounted for 41.9% of the unemployed, and the percentage of long-term unemployed had exceeded 40% for 31 consecutive months. Prior to the 2007−2009 recession, the highest proportion of long-term unemployed was 26%, having occurred in 1983. There are many factors that can explain this difference, such as:

demographic changes (for example, a higher share of older workers);

different economic conditions (for example, labor demand); and

remaining structural changes (for example, unemployment insurance extensions).

The existing evidence is scarce.

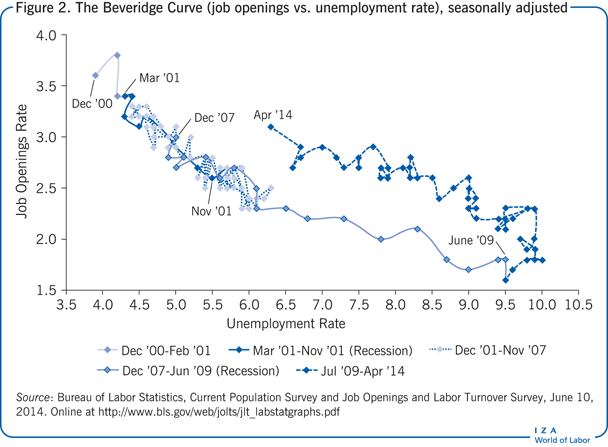

Shifts in the Beveridge curve

Shifts in the Beveridge curve (that relate vacancy rates to unemployment rates at a point in time) may be a sign of structural changes, such as increased mismatch or supply shifts in the economy. An examination of the Beveridge curve for the US suggests the possibility of structural change, because vacancy rates are high relative to unemployment rates during the recovery from the 2007−2009 recession (see Figure 2). The pattern is equally consistent with the counter-clockwise dynamics observed during recessions and recoveries. The intuition behind the dynamics is that the posting of vacancies increases before actual hiring occurs. Thus, there is a short-term increase in vacancies before unemployment declines. Extended unemployment insurance benefits may contribute, as the unemployed delay their return to work [1].

Existing evidence from the US shows that, historically, during recessions the actual unemployment rate is higher than that which would have been implied by the long-term Beveridge curve by as much as 4 percentage points, which disappear as the economy recovers [5]. The introduction of structural reforms in the UK and Germany is suggested to have increased the flexibility of the labor market [8].

Limitations and gaps

One limitation of this analysis is the difficulty of determining whether a recession is cyclic or structural while it is underway. This may lead to an underestimation of the potential increase in structural unemployment. Furthermore, empirical findings available to date consider predominately the US experience during and after the 2007–2009 recession. Hence, this is a case study only and evidence for other countries is still scarce.

Summary and policy advice

The design of policy responses to high unemployment rates during a recession should be based on the evaluation of indicators such as the composition of the unemployed, the degree of mismatch in the labor market, and whether there are any supply shifts. The evidence from the US experience of a persistently high unemployment rate during the 2007−2009 recession points to primarily cyclic factors driven by problems in the general macroeconomic environment and not in the labor market. Therefore, the standard cyclic remedies, to the extent that they are effective, were appropriate.

Acknowledgments

The author thanks Konstantinos Tatsiramos for many helpful suggestions on an earlier draft, two anonymous referees and the IZA World of Labor editors for many helpful suggestions on earlier drafts.

Competing interests

The IZA World of Labor project is committed to the IZA Guiding Principles of Research Integrity. The author declares to have observed these principles.

© Edward P. Lazear

Structural change: definition

There are a number of different ways to define structural change. The first option is to define structural causes of increased unemployment as those that cannot be influenced by monetary policy. This may be the most relevant definition, but it confuses two issues: (a) determining the causes of unemployment; and (b) assessing whether those factors can be remedied by monetary policy.

A second option defines structural causes of increased unemployment as those that cannot be remedied by either monetary or fiscal policy. This definition is broader than the first, but still suffers from the same problem, as outlined above.

A third approach is to distinguish between supply and demand causes. Supply causes may be labeled structural causes, which demand causes are not. This is based on the idea that demand conditions tend to be short-lived and are inherently cyclic, whereas supply conditions may reflect longer-term changes, such as demographics. This includes changes that may be brought about by fiscal policy.

For example, changes in the generosity of unemployment insurance might induce workers to spend more time searching for jobs or taking more leisure. Making housing subsidies income contingent would also lower the value of work and might increase the proportion of individuals who are unemployed.Fourth, a structural change might be said to occur if the composition of unemployment changes. However, this definition is somewhat indirect. It suggests that a structural change has occurred when we observe changes in the pattern of unemployment, not when we see changes in the factors that caused the pattern of unemployment to change. It is a “define-by-residual” approach: that is, if nothing else can account for a pattern, then it must be structural. In addition, it also overlooks the notion that the existence of more long-term unemployed people does not in itself imply that monetary policy has less power to affect unemployment than it did in the past.

A fifth approach is simply to define a structural shift as one that is permanent (or at least long-lasting). A non-structural (possibly “cyclical”) shift is a change that is more temporary. In summary, a structural change is permanent (or at least long-lasting). A non-structural (cyclical) shift is a change that is temporary. Structural changes can occur if there are changes to unemployment insurance or the industrial composition of the economy.

For example, a permanent change in the amount or nature of mismatch would be considered as structural. The industrial composition of the economy may have changed permanently. Consequently, this change might mean that the skill requirements of the available jobs do not match the skill set of workers who are looking for jobs because they trained for an economic structure that has become out of date. Monetary policy is unlikely to be helpful in fixing these kinds of structural changes.Source: Lazear, E. P., and J. R. Spletzer. “The US labor market: Status quo or a new normal?” In: Annual Proceedings of the Jackson Hole Federal Reserve Conference, 2012.

Defining and measuring mismatch

Lazear, E. P., and J. R. Spletzer. “The US labor market: Status quo or a new normal?” In: Annual Proceedings of the Jackson Hole Federal Reserve Conference, 2012.

Beveridge curve: Definition

Lazear, E. P., and J. R. Spletzer. “The US labor market: Status quo or a new normal?” In: Annual Proceedings of the Jackson Hole Federal Reserve Conference, 2012.