Elevator pitch

When hiring new workers, employers use a wide variety of different recruiting methods in addition to posting a vacancy announcement, such as adjusting education, experience, or technical requirements, or offering higher wages. The intensity with which employers make use of these alternative methods can vary widely depending on a firm’s performance and with the business cycle. In fact, persistently low recruiting intensity partly helps to explain the sluggish pace of job growth in the US economy following the Great Recession, and the historically subpar wage growth during the subsequent expansion.

Key findings

Pros

An employer’s recruiting intensity is an important part of hiring and job creation.

Changes in recruiting intensity can account for some structural or “mismatch” unemployment.

Businesses that are fast-growing recruit more intensely.

Positions that offer higher wages tend to have greater recruiting effort and generate more interviewees per job offer.

Cons

Until recently, theories of the labor market generally ignored recruiting intensity, complicating policy analysis.

Recruiting intensity is difficult to measure and is not well understood by economists.

Little is known about which recruiting methods matter most, or which aspects of recruiting intensity might be most responsive to policy.

Existing evidence is unable to identify supply- or demand-driven changes in recruiting intensity.

Author's main message

Job creation policies that only focus on how often employers hire and ignore how employers adjust their recruiting efforts for those hires may fail to achieve their goals. The behavior of aggregate recruiting intensity in the US during and after the Great Recession underscores this point. Following the Great Recession, recruiting intensity remained persistently low despite a rise in the vacancy rate to historically high levels. In contrast, wage growth and the hiring rate recovered more sluggishly, in part because of low recruiting intensity.

Motivation

When looking to hire workers, employers often do more than post a job vacancy. They can alter their hiring standards for a given position. They can do this explicitly, such as when they adjust specific education, experience, or technical requirements for a particular job, or implicitly, such as when they post a vacancy, but only in the hopes of attracting an outstanding candidate. Employers can also alter the wage offered. They can use above-market wages to attract more applicants, or increase the probability that job candidates accept an offer, in the hopes of filling a position more quickly. And they can vary the amount of resources they dedicate to recruiting, under the assumption that greater effort in the recruiting process will fill a position faster. These multiple methods can be collectively referred to as an employer's “recruiting intensity.”

Employers tend to put the most effort into filling their vacancies when their business is growing rapidly and when the economy is expanding. Economists are just now beginning to understand the importance of these adjustments for labor market fluctuations.

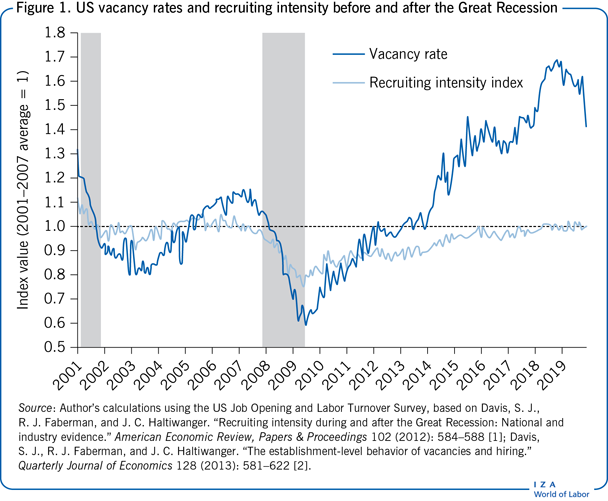

The experience of the US labor market following the Great Recession is a prime example of how changes in recruiting intensity affect the posting of job openings and the subsequent hiring for those positions. During the end of the recession, between mid-2009 and 2012, the US vacancy rate recovered back to its pre-recession level, but wage growth and the hiring rate remained low and unemployment remained elevated. Persistently low recruiting intensity is a partial explanation for this divergence. It remained 9% below its pre-recession level in 2012, did not fully recover until 2016, and remained near its pre-recession level thereafter, even as the vacancy rate continued to rise well above its pre-recession level [1], [2] (Figure 1).

Discussion of pros and cons

Recruiting effort and hiring outcomes

The fact that employers use multiple methods to attract and hire workers has been known for some time. Employers search more intensely when a position requires more formal training, or when the eventual hire is more educated or experienced [3]. Such positions are more difficult to fill, though, independent of the amount of recruiting effort. Recruitment strategies, and consequently how long a vacancy remains open, vary with the starting wage offered [4]. The duration of a vacancy's posting reflects more of a screening period than a selection period, meaning that most job-seekers who are interviewed apply at the beginning of a vacancy's posting [5]. The remaining time between the initial posting and the eventual hire is spent screening these applicants. This stands in contrast to the notion that a vacancy's duration is a selection period whose length depends on how long it takes for a qualified applicant to walk through the door.

The relationship between the wage offered and the recruiting outcome shows that positions offering higher wages tend to have a greater recruiting effort by the employer and more interviewees per job offer [6], [7].

Recruiting intensity and business performance

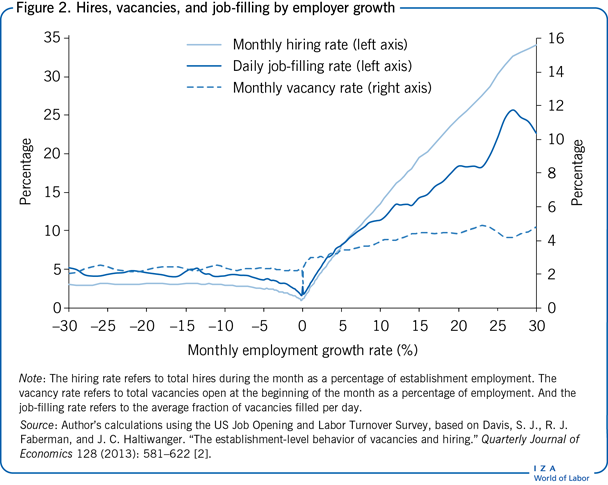

Research on recruiting intensity documents its importance for individual businesses and the economy as a whole. Specifically, it examines how recruiting intensity and hiring outcomes relate to a business's performance and to the business cycle [1], [2], [8], [9]. The monthly hiring rate (total monthly hires, as a percentage of employment), the monthly vacancy rate (total vacancies open at the beginning of the month, as a percentage of employment), and the daily job-filling rate (percentage of vacancies filled daily) vary with establishment-level growth (see Figure 2). First, there is a substantial amount of recruiting and hiring done at establishments that are contracting, though the pace is fairly stable in relation to the size of the contraction. Second, there is a dip in the pace of recruiting and hiring for establishments with close to zero growth. Third, hiring and vacancy rates rise with the size of an establishment's expansion.

The hiring rate rises slightly more than one-for-one with the growth rate, while the vacancy rate rises much less than one-for-one. Thus, on average, businesses that expand their employment by 30% have a hiring rate of about 34% of employment, suggesting some turnover even as they rapidly expand, and a vacancy rate of just under 5%. The fact that hires and vacancies do not rise proportionally with an establishment's growth rate implies that an establishment's vacancy-filling rate must rise with the growth rate. As an establishment moves from zero growth to around 30% growth, the chances that it fills one of its vacancies on any given day rises from just under 3% to about 23% (Figure 2).

The rise in the job-filling rate with establishment growth reflects the fact that fast-growing businesses recruit more intensely. These businesses, by definition, hire at a rapid pace. Consequently, they do much more than simply post many vacancies to attract these workers.

kept in mind that some outside force must drive an employer's decision to expand. For example, a sudden increase in the demand for a business's product will cause it to ramp up production. In this case, it is not enough only to post vacancies. The business has a strong incentive to fill these vacancies quickly. The methods at an employer's disposal when doing so include all of the methods described above:

Employers could offer above-market wages to attract more applicants or make job candidates more likely to accept their offer.

They could also lower their hiring standards, opting for hires that are less experienced or less qualified than the people they would normally hire, with the thought that these individuals could be trained on the job or that the returns to growth outweigh the increased risk of worker turnover.

Employers could try to look at the widest range possible when attracting applicants, exerting significant effort through the use of networking, referrals, and the aggressive advertising of their job postings.

Finally, they could exert significant effort in the screening process, ensuring that enough quality applicants are interviewed to fill the available positions.

Recruiting intensity and the business cycle

A measure of recruiting intensity that captures these micro-level variations in employers’ recruiting behavior shows that changes in recruiting intensity can have considerable effects on the overall labor market [1], [2]. Specifically, aggregate measures of recruiting intensity vary with the business cycle, tending to fall during recessions and to rise during expansions. This is partly due to the fact that a slack labor market makes it easier for employers to hire in general, so less recruiting effort is required to achieve the same job-filling rate. At the same time, persistently low recruiting intensity can account for some of the shift in the US Beveridge curve following the Great Recession.

The Beveridge curve is the aggregate relationship between the unemployment rate and the vacancy rate. Between the end of the Great Recession and mid-2013, the vacancy rate rose steadily while the unemployment rate fell slowly. This led to an outward shift of the Beveridge curve, implying that there were more unemployed workers for a given level of vacancies. Between 2013 and 2018, the vacancy rate continued to rise but unemployment fell more steadily, leading to a gradual inward shift of the Beveridge curve. Throughout 2019, the vacancy rate fell somewhat while the unemployment rate remained steady, leading to a further shift of the Beveridge curve.

A plot of the relative movements in the US vacancy rate and the index of recruiting intensity over time shows that the vacancy rate fluctuates much more over the business cycle than recruiting intensity does (Figure 1). Between late-2007 and mid-2009 (the official span of the Great Recession), the vacancy rate fell by 43%, while recruiting intensity fell by 23%. Since then, however, vacancies and recruiting intensity have diverged considerably. The vacancy rate has risen steadily. By early 2012, the vacancy rate had returned to its pre-recession average, but recruiting intensity was still 9% below its pre-recession average. Starting in 2014, the vacancy rate began a steady rise, peaking at 69% above its pre-recession average at the end of 2018 before declining somewhat in 2019. In contrast, recruiting intensity did not return to its pre-recession average until 2016 and remained roughly steady thereafter.

Recruiting intensity, matching efficiency, and unemployment

The relatively stagnant behavior of recruiting intensity following the Great Recession is consistent with the persistently high US unemployment rates during this time. Between mid-2007 and late-2010, the unemployment rate more than doubled, from 4.5% to a peak of 9.8%. At the end of 2012, the unemployment rate had only fallen to 7.9%. This slow decline, coupled with the rapid recovery in the vacancy rate, led to the shift in the US Beveridge curve. Multiple theories on the causes of this shift have arisen, each with considerable policy implications. Technically speaking, a shift in the Beveridge curve represents a change in the efficiency of matching workers to jobs. Since the vacancy rate rose faster than the unemployment rate fell, the shift reflects a decline in matching efficiency. As noted, this outward shift took several more years to reverse itself.

This decline could have come about for a variety of reasons:

Some interpret it as a rise in structural unemployment. Under this interpretation, the skills of the unemployed do not match up with the skills required of the posted job vacancies. It may be that these workers’ skills deteriorated while they were unemployed, or that the businesses posting vacancies are quite different from the businesses where job-seekers were last employed, leading to a “mismatch” between job openings and job-seekers.

Another interpretation is that the technologies used to match workers to jobs have changed, though the rise in the use of online job search tools should increase rather than decrease matching efficiency.

Yet another interpretation is that the shift reflects a reduction in search effort by the unemployed, driven by a sharp rise in the amount of unemployment insurance benefits provided.

Hypotheses regarding structural change and unemployment insurance benefits have largely been refuted as being too small to account for the observed shift in the Beveridge curve. Using an index to measure the degree of mismatch between job-seekers and vacancies, researchers have found that, while the index rose sharply during the Great Recession, it fell just as quickly following its end [10]. Using variations in the timing and length of benefit extensions across US states, the contribution of extended unemployment insurance benefits on the unemployment rate is found to be small [11].

The persistently low recruiting intensity seen in Figure 1 is at least a partial explanation of the shift in the Beveridge curve. The shift reflects increased “choosiness” on the part of employers, or alternatively an unwillingness to pay a wage that current job-seekers are willing to accept. Recent research using online vacancy postings shows that businesses in fact increased their hiring standards following the Great Recession [8], [9]. Standard economic theories of labor market search can also be expanded upon to estimate the contribution of changes in recruiting intensity to shifts in the Beveridge curve. Doing so for the 2001−2011 period shows that changes in aggregate recruiting intensity account for about 20% of its shift [2].

Why recruiting intensity is not well understood

Changes in recruiting intensity have been inferred from the implications of a more generalized theory of labor market search and matching, with respect to the hiring and vacancy filling process. This inference-based measure of recruiting intensity becomes a catch-all for a variety of different methods by which employers can affect hiring outcomes. From a policymaker's perspective, it may be critical to know whether employers have cut back on actual recruiting effort, reduced the wages they are willing to offer, or increased their overall “choosiness” in the quality of job candidate that they prefer.

As noted, recent studies have used online job boards data to track the qualifications employers seek for a potential hire [8], [9]. Even in these cases, though, it is not clear why these qualifications change. It may be that new production technologies employers use require a more skilled workforce, or it may be that heightened economic uncertainty causes hesitancy on the part of employers in hiring all but the most exceptional candidates.

Knowing the root causes of a change in recruiting intensity is critical for policy. Policymakers may be able to offset changes in the relative wages offered by employers, or induce employers to offer a wage job-seekers are willing to accept, with various policy instruments, but policy options are likely to be more limited in affecting how choosy employers are in who they hire. Furthermore, policymakers will likely want to know if any change in recruiting intensity reflects something permanent, as with an increase in skill requirements due to the use of new technologies, or something transitory, as with a response to economic uncertainty.

Traditionally, labor market theories have assumed that when a business wants to expand, it posts vacancies in proportion to the number of people it wants to hire. Recent studies, however, have incorporated recruiting intensity explicitly into these theories [12], [13]. These theories illustrate how businesses can use the wages they offer and their explicit recruiting efforts to affect how quickly they fill their vacancies. More importantly, they show how shocks to the aggregate economy can alter the choices businesses make for their wage offers and recruiting efforts. These recent studies provide new models of the labor market that will hopefully guide policymakers in their thinking about how businesses create jobs and the effort they put into filling those jobs.

Limitations and gaps

Recruiting intensity is an important part of fluctuations in the labor market, but several issues limit the policy recommendations one can give about it. First, the data available in most countries make a direct measurement of recruiting intensity difficult, though recent studies have made progress with innovate new sources such as online job boards. More generally, it is difficult to conclude why recruiting intensity may have risen or fallen, regardless of how well one can measure it. Finally, providing detailed policy implications regarding recruiting intensity is also hindered by the fact that it is generally ignored in traditional labor market models, but recent research has made significant progress in bridging the gap.

Summary and policy advice

Recruiting intensity is an important part of the hiring process. Changes in recruiting intensity have implications at both the micro and macro levels. Employers’ recruiting intensity per vacancy varies systematically with the growth prospects of the business as well as the labor market conditions that the business faces.

Recruiting intensity includes a variety of methods at an employer's disposal. Adjustments can involve changes in the employer's hiring standards, in offering a wage substantially above or below the market wage for a particular position, or in the physical effort an employer puts into attracting applicants and screening candidates. Little is known about which recruiting methods matter most, or which aspects of recruiting intensity might be most amenable to policy.

Employers tend to put the most effort into filling their vacancies when their business is growing rapidly and when the economy is expanding. There is a substantial amount of recruiting and hiring done at establishments that are contracting, but the pace is fairly stable in relation to the size of the contraction.

In contrast, hiring and vacancy rates rise with the size of an establishment's expansion. The hiring rate rises slightly more than one-for-one with the growth rate, while the vacancy rate rises much less than one-for-one. The rise in the job-filling rate with establishment growth reflects the fact that fast-growing businesses recruit more intensely. These businesses, by definition, hire at a rapid pace. So, they do much more than simply post many vacancies to attract these workers.

Aggregate measures of recruiting intensity vary with the business cycle, tending to fall during recessions and to rise during expansions. This is partly due to the fact that a slack labor market makes it easier for employers to hire in general, so less recruiting effort is required to achieve the same job-filling rate.

The US vacancy rate rose faster than the unemployment rate fell following the Great Recession, causing an outward shift in the Beveridge curve that reflects a decline in matching efficiency. Even as the vacancy rate continued to rise, well above its pre-recession levels, the Beveridge curve remained shifted outward, taking a decade to shift back.

Fluctuations in aggregate recruiting intensity account for a sizable portion of this shift. Persistently low recruiting intensity reflects greater “choosiness” on the part of employers or their unwillingness to pay a wage that current job-seekers are willing to accept. Lower employer recruiting intensity makes it less likely that a job-seeker is hired for a given level of vacancies.

Job creation policies that ignore the fact that employers can adjust along multiple margins in the hiring process may fail to achieve their goals. For example, in the US, aggressive policies focused on stimulating hiring during and after the Great Recession. Vacancies rebounded during this period, but recruiting intensity did not, and hiring remained low. Regardless of how employers go about recruiting, changes in the intensity of their efforts over time add an additional layer of complexity between the posting and filling of an open position.

Both policymakers and economists need a better understanding of what causes employers to vary their efforts in filling their job vacancies. Only then will policymakers be in a position to create effective targeted policies that boost hiring and reduce unemployment.

Acknowledgments

The author thanks an anonymous referee and the IZA World of Labor editors for many helpful suggestions on earlier drafts. The views expressed here are solely those of the author and do not necessarily reflect the positions or policies of the Federal Reserve Bank of Chicago or the Federal Reserve System. Version 2 of the article updates the discussion to further analyze the effects on unemployment, recruitment, and wages in the more recent years following the Great Recession, includes updated figures, and new “Key references” [8], [9], [12], [13].

Competing interests

The IZA World of Labor project is committed to the IZA Code of Conduct. The author declares to have observed the principles outlined in the code.

© R. Jason Faberman