Elevator pitch

How do minimum wage policies interact with labour tax evasion? In many transition economies, two features stand out: a large spike in the wage distribution at the minimum wage and widespread use of “envelope wages”—undeclared cash paid in addition to official earnings. This spike can be explained by the over-representation of tax-evading employers among minimum wage payers. In such a context, raising the minimum wage may serve as an enforcement tool by compelling evading firms to convert part of the undeclared pay into formal wages in order to comply with the legal minimum.

Key findings

Pros

Raising the minimum wage reduces income underreporting among labour tax (and social security contributions)-evading firms.

Envelope wages provide an adjustment margin, allowing firms to comply without reducing total pay.

Firms that underreport wages are less likely to cut employment in response to a minimum wage hike.

Higher formal wages boost personal income tax and social security contribution revenues.

Cons

Not all firms engage in labour tax evasion making them more sensitive to minimum wage policy.

Minimum wage hikes can lead to job losses in firms that already fully comply with wage regulations.

Firms using envelope wages will lose an adjustment margin when facing negative shocks.

Employees of evading firms may face lower take-home pay if the tax burden is shifted onto them.

Author's main message

Labour tax evasion through income underreporting remains a significant challenge in Central and Eastern Europe. Many workers receiving envelope wages are officially recorded as earning exactly the minimum wage, creating a visible spike in the wage distribution. In this context, raising the minimum wage can function as a tax enforcement tool, prompting firms to formalize a larger share of compensation. However, not all firms evade taxes—some genuinely pay minimum wage. For policymakers, this creates a trade-off: while minimum wage hikes can improve compliance and increase tax revenue–and social security contributions–they may also impose costs on compliant firms and risk job losses in that segment.

Motivation

Labour markets in transition and post-transition countries are often characterized by widespread payroll tax evasion, notably in the form of “envelope wages”—undeclared cash payments made in addition to official wages. This form of tax and social security contribution avoidance has several adverse effects. It distorts competition to the disadvantage of tax-compliant firms, undermines public revenues and the provision of public services, and weakens workers’ social protection and access to credit.

At the same time, many Eastern European countries have implemented frequent and sizable minimum wage hikes—for example, a 20% increase in Ukraine in 2021, 25% in Latvia between 2013 and 2015, 96% in Hungary between 2000 and 2002, and 50% in Russia in 2007. These increases are often substantial enough to affect a large segment of the workforce. Indeed, the share of minimum wage workers in these countries tends to be higher than in other EU member states.

Against this backdrop, a key question arises: Can raising the minimum wage help reduce labour tax evasion? More specifically, can minimum wage policy act as a tool for tax enforcement in economies where wage underreporting is widespread?

Discussion of pros and cons

Labour tax evasion at the intensive margin

In labour economics, informal employment is often described as a distinct sector operating at the margins of the formal labour market. Firms are typically viewed as either formal—fully compliant with labor regulations and tax obligations—or informal, operating outside the regulatory framework. However, in many countries, especially post-Soviet states in Eastern Europe, informality often takes a different form. Rather than existing entirely outside the formal sector, many firms are partially compliant: they formally declare their employees but underreport actual wages. In this setup, an employee's earnings consist of two components—a declared wage and an undeclared “envelope” wage paid in cash and exempt from taxes and social contributions. This form of labour tax evasion occurs at the intensive margin: the question is not whether to participate in the formal labour market, but to what extent.

Before examining the interactions between minimum wage policy and labour tax evasion, a key issue is how to properly measure wage underreporting. By its nature, labour tax evasion is difficult to observe directly, and estimating its prevalence poses significant challenges. The most straightforward measurement strategy relies on direct survey data.

Several European Commission Eurobarometer surveys (2007, 2013, 2019) include questions on undeclared wages and show substantial cross-country variation, with Eastern European countries consistently reporting higher rates. The headline 2019 Eurobarometer figure from the single direct question was that 3% of EU respondents overall admitted receiving part of their salary in cash (7% in Latvia, 6% in Hungary). Drawing on the additional, more detailed items in the 2019 module, recent studies show that prevalence is considerably higher once performance-related top-ups and other quasi-formal arrangements are taken into account [1], [2].

However, direct surveys likely underestimate the true extent of evasion, as respondents may be reluctant to answer truthfully. Moreover, they typically shed little light on the scale of evasion at the macroeconomic level. To address this limitation, researchers have developed the Labour Input Method [3], [4], which compares labour input measures from household surveys (e.g., Labour Force Survey) with administrative data. With this approach, large variation in undeclared work is observed at the EU level: from as low as 5.3% of private sector gross value added in Austria to 27.1% in Romania [3]. This method, however, rests on the assumption that survey respondents accurately report their labour market activity and earnings.

To mitigate the potential for underreporting bias in direct surveys, researchers developed so-called “indirect” survey methods. An interesting application of indirect survey was used to estimate the size of the informal sector in the Baltic states [5]. This application is based on two key premises. First, that firm managers are better informed than workers about wage reporting practices; and second, that asking managers about practices in their industry rather than in their own firm yields more candid responses. Based on this method, envelope wages are estimated to account for 15% of the total wage bill in Lithuania in 2009, 19.5% in Estonia, and 34% in Latvia. A key limitation of this type of approach, however, is that it provides aggregate-level estimates but no insight into the question who receives envelope wages, similarly to other existing approaches based on macroeconomic variables. However, understanding where are located evaders in the income distribution is crucial to study the relationship between minimum wage and wage underreporting.

Labour tax evasion and the wage distribution

The idea that increases in the minimum wage can reduce labour tax evasion relies on the assumption that evasion is most prevalent at the lower end of the wage distribution. In other words, underreporting tends to occur around the minimum wage. But why would envelope wages be concentrated near the official minimum wage?

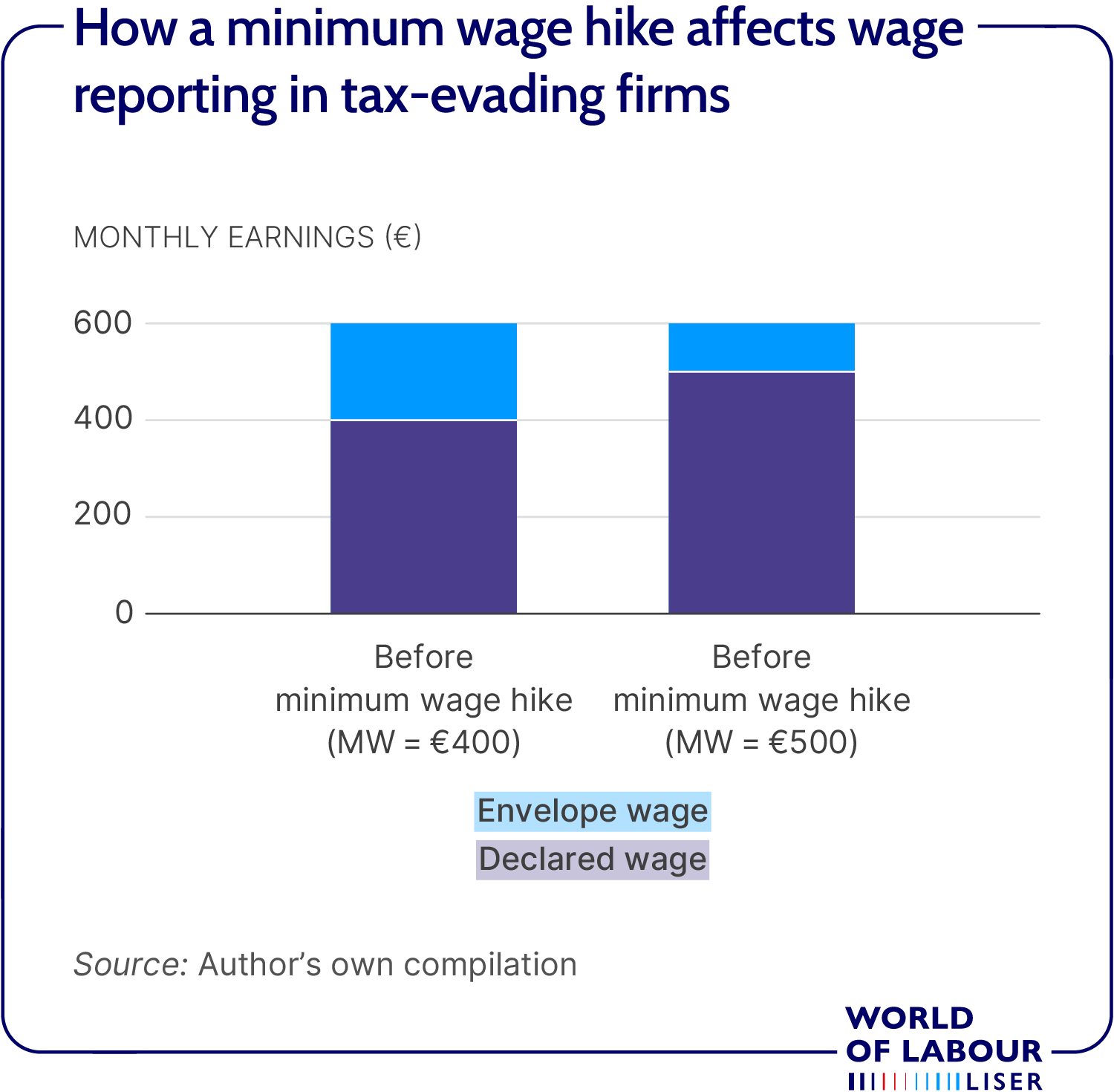

A key rationale is that employers and employees may collude to report only the minimum wage in order to reduce tax liabilities while avoiding scrutiny by tax authorities. In many countries, paying wages below the statutory minimum wage raises red flags and increases the likelihood of detection. As a result, workers officially receiving the minimum wage will experience an increase in their declared wage following a minimum wage hike, in order to remain compliant with the new threshold. Economic research has developed formal theoretical models in which the introduction of a minimum wage creates a spike in the distribution of declared earnings, as evaders bunch at precisely the minimum wage [6]. In support of this argument, another study documents a positive correlation between the size of the spike at the minimum wage in the earnings distribution and the extent of labour tax evasion in European labour markets, using data from direct surveys [7].

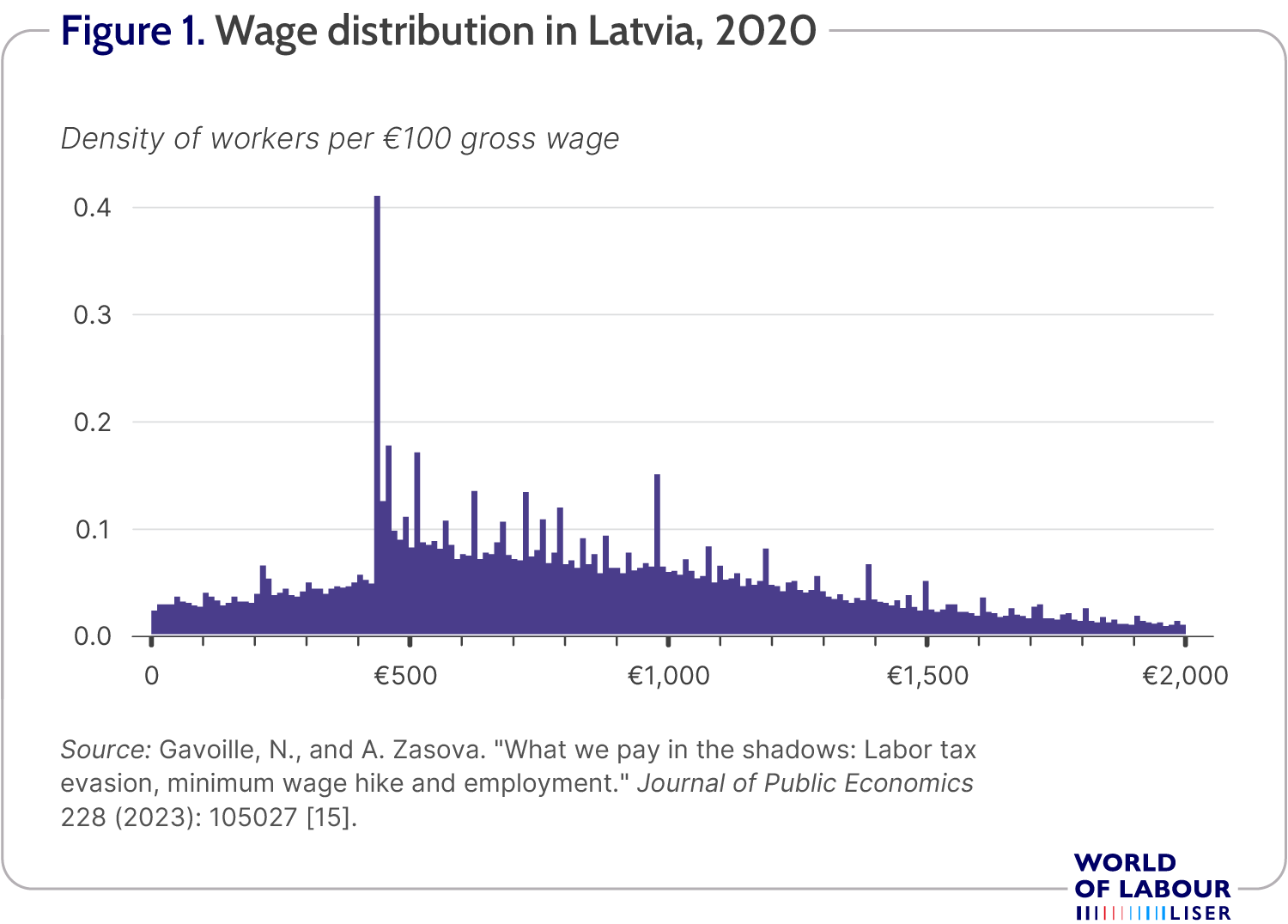

Beyond this macro-level correlation, several studies have examined income underreporting along the wage distribution. First, a recent study presents a body of suggestive evidence highlighting the prevalence of wage underreporting at precisely the minimum wage in Latvia [8]. This country is a good testing ground, since labour tax evasion is a major issue on the local labour market: according to the 2014 Eurobarometer survey, one in ten employees in Latvia admitted to receiving part of their salary in cash, the highest share in the EU. As an illustration, Figure 1 displays the wage distribution in January 2023, with a very large spike at precisely the minimum wage.

This study compares the labour market outcomes of individuals earning exactly the minimum wage to those earning slightly more. If workers earning officially the minimum wage are more likely to underreport than workers earning just a few euros more than the minimum wage - firms paying envelope wages having no incentives to increase the formal wage beyond the mere minimum wage - labour market outcomes of these two groups of workers should be significantly different. Accordingly, the study looks, among other outcomes, at the probability to obtain a (formal) pay raise over a three-year period during which the minimum wage remained stable. Consistent with this, the study shows that nearly 50% of individuals officially earning the minimum wage in 2011 were still earning exactly the same amount in 2013. In contrast, over 80% of workers earning just a few euros more in 2011 experienced a wage increase during the same period. The differences are particularly pronounced in small firms, which are known to have a higher incidence of wage underreporting. The same study also tracks the income of workers who change jobs. Among workers who switch from a small to a large firm, those previously earning exactly the minimum wage experience a substantially larger wage increase than those earning slightly more than the minimum wage. Taken together, these findings are difficult to explain without assuming a higher prevalence of envelope wages among workers earning the minimum wage.

Additional evidence comes from Hungary, where two papers exploit institutional features to explore the bunching of tax evaders near the minimum wage [9], [10]. First, a reform in 2006 required firms to pay social security contributions based on twice the minimum wage for workers paid below this threshold, unless they filed for an exemption that increased their audit risk. In other words, a firm employing a worker at the minimum wage had to pay social security contributions as if this worker was paid twice the minimum wage. A firm genuinely paying a worker the minimum wage should have no problem filing in an exemption form. For firms paying envelope wages, however, asking an exemption is more risky. The authors find that more than 10% of employees who declared the minimum wage prior to the reform reported exactly twice the minimum wage the following year. Evasion was found to be especially prevalent in sectors with a high risk of underreporting, such as construction and transportation, and more common in small domestic firms [11], [12].

The second study examines maternity benefits, which in Hungary are calculated based on declared wages prior to childbirth. This system creates incentives to shift undeclared wages into formal wages during pregnancy. The authors find that expectant mothers, on average, experience a rise in declared earnings between the second and sixth months of pregnancy. This effect is particularly strong among women who were paid the minimum wage before pregnancy, again suggesting that envelope wages are common at the bottom of the wage distribution.

Finally, a recent study proposes an attempt to not only evaluate where are evaders located in the wage distribution, but also what is the “thickness” of the envelope [13]. For this purpose, it implements a stochastic frontier analysis approach, modeling undeclared wage as an inefficiency. Using Latvian data, the authors find that evasion is concentrated in small firms, and that workers near the minimum wage are much more likely to receive envelope wages. On average, undeclared pay accounts for about 30% of the gross wage in such cases.

Envelope wages, minimum wage shock, and employment

Having established that, in countries where labour tax evasion is prevalent, wage underreporting primarily occurs at the bottom of the wage distribution, the focus now turns to the interaction between minimum wage hikes and evasion. How do firms that pay envelope wages to their workers absorb a minimum wage hike? And does this differ from the response of tax-compliant firms? Tax-evading firms can, in theory, use this “evasion margin” as a shock absorber [6]. If that is indeed the case, firms underreporting their workers' wages should show no employment response to minimum wage shocks. Thus, a minimum wage increase should reduce the share of total wages that are unreported, leading to higher tax revenue and social security contributions, without negatively affecting employment. But does this mechanism hold in practice?

One way to study this is to investigate the likelihood of an employer–employee relationship “surviving” a minimum wage increase, comparing workers paid exactly the minimum wage to those earning slightly more. If minimum wage workers are more likely to receive envelope wages, they should, on average, be more likely to retain their jobs, according to the shock absorption mechanism described above. This is precisely what is observed in Latvia, following the 2014 minimum wage increase [8]. Similarly, another study evaluating the employment effects of a substantial minimum wage increase in Lithuania in 2013 uses a closely related approach [14]. At the aggregate level, only limited evidence of negative employment effects is observed. However, comparing employment outcomes across firms plausibly paying envelope wages—those with fewer than 20 employees operating in the construction, retail trade, accommodation and food services, and personal services sectors—to the broader set of firms, the employment response turns out to be much smaller among the former group, suggesting that wage underreporting acts as an adjustment mechanism. Nonetheless, these results are essentially descriptive and do not rely on a clear classification of firms as compliant or evading.

Identifying the employment response of evading versus compliant firms requires a firm-level classification. However, since tax evasion is largely unobservable, creating such a classification is a significant challenge. One recent attempt relies on the use of machine learning techniques [15]. The idea is to train an algorithm to classify firms based on information from their balance sheets. For this, a sample of firms with known compliance status is required to train the model. Obtaining such a sample is, however, not trivial, since tax evasion is not observable. A possible approach could be to use data from labour tax audits performed by the state revenue service. However, audited firms have in general very specific features. To overcome the unavailability of a suitable training sample, an option is to build one, based on a few (strong) assumptions. First, one can consider that firms owned by foreign investors from low-corruption countries are compliant—a premise supported by finance literature showing that management practices are often “imported”. Second, firms employing “suspiciously” low-paid workers—those paid well below expected levels based on characteristics such as age and education—are assumed to be likely evaders. Based on this training sample, the algorithm classifies the broader firm population. Results suggest that about 35% of firms in Latvia in the early 2010s likely paid envelope wages. As expected, underreporting is more common among small firms and in the construction and transportation sectors.

While this method is based on strong assumptions, several validation checks support its relevance. First, for a subset of workers, survey-reported wages can be compared with administrative data. Employees in firms classified as evaders tend to report higher wages in surveys than in official records, unlike those in compliant firms. Second, workers who move from an evading firm to a compliant one experience substantial increases in reported earnings. By contrast, those moving in the opposite direction generally see no change in their formal wages. These patterns are consistent with the presence of envelope wages in the evading firms.

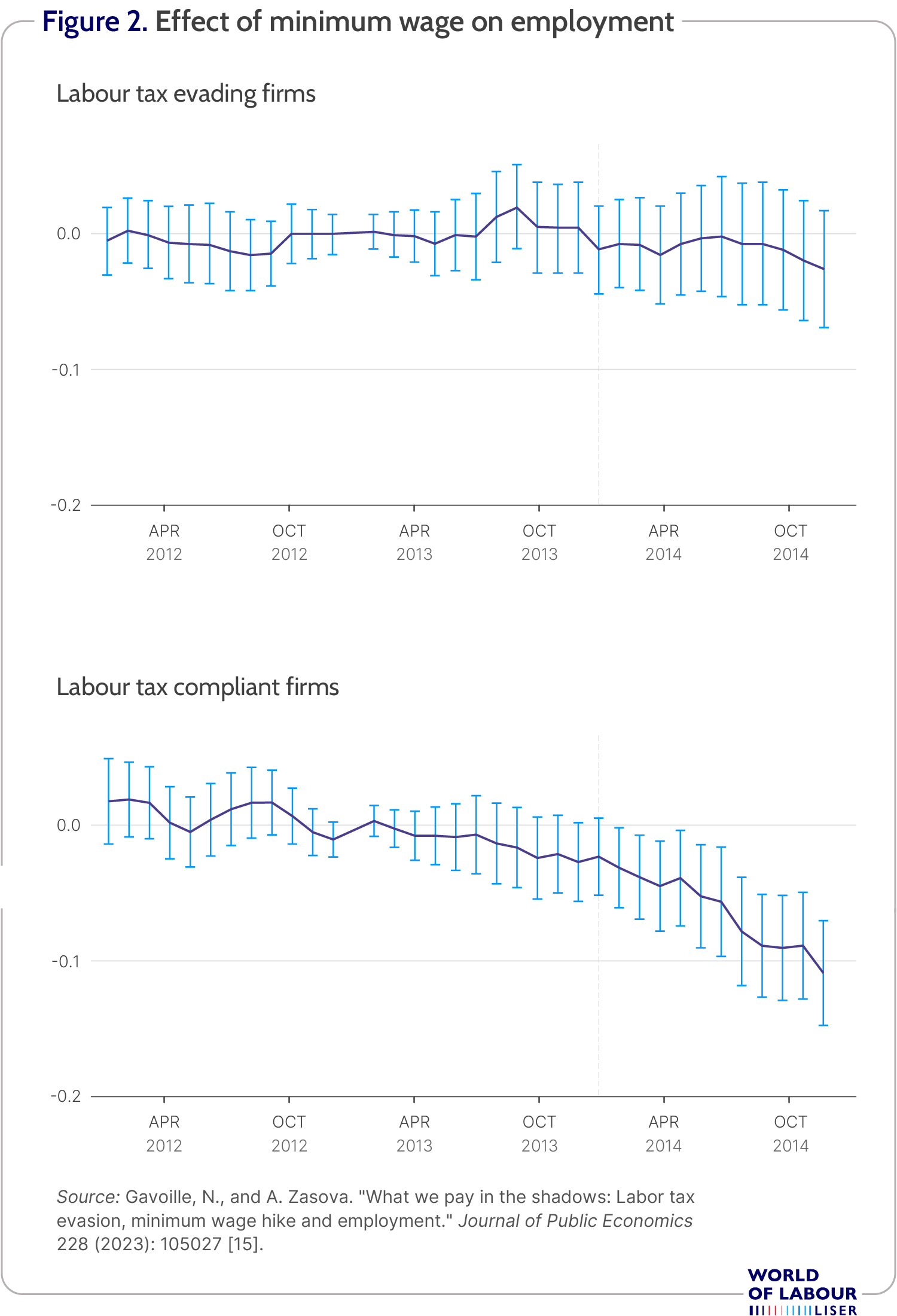

Finally, equipped with this compliant/evader firm-level classification, it becomes possible to estimate the employment response following a large increase in minimum wage, which took place in 2014/2015. Not all firms are impacted by the minimum wage hike in the same way: some firms have a lot of workers affected by the hike; some others do not have any. The idea is, thus, to estimate the relationship between the share of workers affected by the hike and the percentage change in employment before and after the reform, and to contrast the results between compliant and evading firms. If envelope wage is indeed used as a shock absorber, one should observe that employment consequences are smaller for evading firms than for compliant firms.

This is exactly what the data show. Figure 2 illustrates the cumulative employment effect from January 2013 (12 months before the reform) onward, comparing evading and compliant firms. It represents the difference in employment growth between a firm in which all employees are affected by the hike and a comparable firm where none are. The dotted vertical lines mark the introduction of the minimum wage increase. For evading firms, employment remained largely unaffected, with no significant relationship between exposure to the hike and employment change. By contrast, among compliant firms, those employing only minimum wage workers experienced 12% lower employment growth one year after the reform compared to those with no affected workers. This negative effect reflects both firm closures and changes in hiring and firing behaviour. Notably, prior to the reform, employment growth was unrelated to the share of low-wage workers. Furthermore, the increase in the minimum wage led to higher wages, income tax payments, and social security contributions, ruling out widespread non-compliance with the new wage floor (e.g., full-time workers being falsely reclassified as part-time).

A drawback of this approach is its inability to properly capture the macroeconomic effect of the minimum wage hike. Beyond firm-level analysis, a recent study combines micro- and macro-level approaches to assess how minimum wage changes affect undeclared wages at the aggregate level [16]. Using a Computable General Equilibrium (CGE) model, it examines the economy-wide effects of a minimum wage increase, accounting for undeclared income. The findings suggest that such a policy reduces underreported payments and raises reported gross wages, but comes at the cost of an overall negative employment effect. This type of micro-macro combination is a promising path for future research.

Limitations and gaps

Despite growing evidence on the interaction between minimum wage policy and labour tax evasion, several limitations remain. First, existing studies rely on indirect measures and strong assumptions to identify tax-evading firms, since wage underreporting is by nature unobservable. While recent machine learning approaches show promise, their accuracy depends on the validity of the training sample and may not be easily generalizable across countries.

Second, most of the empirical evidence comes from a limited number of case studies, particularly in Eastern Europe. It remains unclear to what extent the findings apply to other institutional contexts where minimum wage coverage, tax enforcement capacity, or informal norms differ.

Third, while some studies have begun combining micro and macro approaches, more work is needed to assess the general equilibrium and long-term effects of minimum wage hikes on informality and tax revenue.

Finally, when converting envelope wage into declared income, employees are likely to bear the burden of the additional personal income tax and social security contributions, resulting in a lower disposable income after the increase in minimum wage [6].

Summary and policy advice

Envelope wages—undeclared cash payments supplementing official wages—remain widespread in many transition economies, particularly among low-wage earners. Evidence suggests that labour tax evaders are over-represented among minimum wage workers, leading to a spike in the wage distribution at the minimum wage. In this context, raising the minimum wage can serve as a tax enforcement tool: by increasing the formal wage floor, policymakers reduce the scope for underreporting, effectively pushing firms to convert part of the envelope into declared pay. This improves tax collection and workers’ access to social protection, with limited adverse employment effects in evading firms. However, not all firms evade taxes—minimum wage hikes may negatively affect compliant firms genuinely paying low wages. Policymakers should thus weigh the gains in enforcement against the potential employment costs, possibly complementing minimum wage increases with targeted enforcement or support measures for compliant low-wage employers.

Acknowledgments

The author thanks the anonymous referee(s) and the World of Labour editors for their comments. Previous works of the author (together with Anna Zasova) contains a larger number of background references for the material presented here and has been used intensively in all major parts of this article [8] and [15].

Competing interests

The IZA World of Labor project is committed to the IZA Guiding Principles of Research Integrity. The author declares to have observed these principles.

© Nicolas Gavoille