Elevator pitch

Traditional models of the labor market typically assume that wages are set by the market, not the firm. However, over the last 15 years, a growing body of empirical research has provided evidence against this assumption. Recent studies suggest that a monopsonistic model, where individual firms and not the market set wages, may be more appropriate. This model attributes more wage-setting power to firms, particularly during economic downturns, which helps explain why wages decrease during recessions. This holds important implications for policymakers attempting to combat lost worker income during economic downturns.

Key findings

Pros

A monopsony model may better characterize the labor market than the standard competitive model.

Empirical evidence supports the monopsonistic perspective that firms have wage-setting power, and that an increase in this power decreases wages during a recession.

The monopsony model implies that employment may vary less over the business cycle, reducing the severity of recessions.

The existence of increased firm wage-setting power calls for policies to stabilize workers’ earnings during an economic downturn, such as a temporary payroll tax cut.

Cons

Most studies that find evidence of firm wage-setting power do not have random variation in wages, possibly biasing results.

While there exists strong evidence consistent with a monopsonistic model of wage-setting, there is less direct evidence of firms’ of monopsony power to set wages.

A temporary payroll tax cut for workers experiencing wage declines could have unintended consequences, effectively subsidizing wage cuts.

Weaker firms may survive an economic downturn due to increased wage-setting power, decreasing the “cleansing” effect of a recession.

Author's main message

Empirical evidence suggests that firms have the power to set wages, and that this power increases during an economic downturn. Furthermore, this evidence implies that increased firm wage-setting power may push wages down during a recession. Policies used to fight recessions typically focus on replacing lost earnings of workers who suffer job loss, but this approach may not be sufficient. In response to decreasing wages, policymakers should consider additional interventions that focus on replacing the lost earnings of workers who remain employed during a recession, such as a temporary payroll tax cut.

Motivation

The standard “textbook model” of the labor market typically assumes perfect competition, where there are no market frictions and neither firms nor workers have wage-setting power. Empirical evidence, however, suggests that a model incorporating market frictions, such as a monopsonistic model, may better describe real-world labor markets. Markets are termed “monopsonistic” if many firms compete to hire labor in a given market, but each firm is able to choose wages that are lower than its competitors without risking the loss of a significant portion of its labor force to competing firms. This model has important implications for understanding and addressing economic downturns. If firms can exercise their wage-setting power, they may choose to lower workers’ wages rather than laying off workers when facing economic hardships. Increased wage-setting power may change the nature of recessions, decreasing the volatility of employment but increasing the volatility of wages. This suggests that policies that focus on stabilizing earnings for employed workers, such as a temporary payroll tax cut, are important tools to fight recessions.

Discussion of pros and cons

The monopsonistic model as a model of frictions in the labor market

When only one firm supplies a good to consumers in a market, the market is a monopoly market and the firm will possess price-setting power. Similarly, when only one firm hires, choosing among many workers in a market, the market is a monopsony market and the firm will possess wage-setting power. When firms possess price-setting power despite not being the only firm in a market, that market is referred to as “monopolistic.” Similarly, when firms possess wage-setting power despite not being the only firm in the market, that market is termed “monopsonistic.” The monopsony model was first developed in the 1930s and for decades the most common example was the rare company town in which a single firm accounted for all labor demand in the market.

To better understand monopsonistic labor markets, it is important to have a clear understanding of perfectly competitive labor markets. There are two key assumptions behind a perfectly competitive labor market. The first is the presence of many firms and workers. The second is that all jobs in a given market are identical and that workers can, without cost and instantaneously, move between these jobs. Note that markets in this context are defined not just by geography, but also by skill or job title.

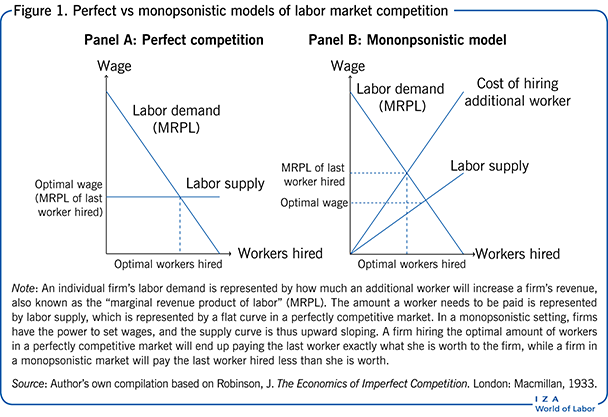

Panel A in Figure 1 displays the textbook model of a competitive labor market at the firm level. The downward sloping demand curve represents each additional worker’s productivity in dollar terms, i.e. the “marginal revenue product of labor” (MRPL). The flat line represents labor supply to the firm, determined by the market wage, which is the optimal wage to offer workers in this setting. The firm can hire as much labor at the market wage rate as desired without increasing wages. This characteristic of the market comes from the assumption that there are many firms in the market, so any additional hiring by one firm has a minuscule effect on overall market demand. In addition, the firm could not hire any worker if it were to offer a single cent less than the going wage rate, a result of the assumption that all jobs in a particular market are identical and thus interchangeable. If these jobs are identical and it is easy for workers to move, a firm not offering the going wage rate will see an exodus of its workers to competing firms. The market equilibrium is where the flat supply curve intercepts the downward sloping demand curve. The last worker hired is paid a wage rate that is exactly equal to their value to the firm and the firm hires all workers whose value exceeds the market wage.

There are compelling reasons to question whether workers will move quickly and freely between firms in order to chase a small difference in wages. First, workers must invest time and energy into searching for a new job. Second, workers might not view all jobs as equal. Even if an alternative job were to pay slightly more, the small increase in pay might not compensate for adjustment costs, such as increased commuting distance.

In contrast to the perfectly competitive model, panel B in Figure 1 presents the monopsony model of the labor market. Here, firms face an upward sloping labor supply curve, as opposed to a flat one. If the firm were to cut its wage, it would lose some, but not all, of its workers. If the firm wanted to hire more workers, it would have to increase the wage offered for each additional worker. If a firm pays a standard wage to all workers in the same position, labor costs can rise sharply if the firm wants to grow. For example, suppose a wage of $15 will recruit one worker, and a wage of $18 will recruit two workers. If the firm is unable to tell which worker would be willing to work for $15 among the two who show up for a posted wage of $18, it must offer both workers the higher wage. Thus, the labor costs of hiring one or two workers are $15 or $36, respectively, implying that it costs 21 additional dollars to hire two workers instead of one. The additional $21 is known as the “marginal expense of labor,” or MEL. If the supply curve is upward sloping and the firm is paying one wage to all workers in a given position, it will always cost more than the “sticker price” of an additional worker to increase the size of the firm because all existing workers in that position will necessarily receive a wage increase in line with the new hire. In other words, MEL lies above the labor supply curve. While monopsonistic firms pay all workers the same wage if they cannot infer anything about the wage at which each worker is willing to work, the firm may offer different wages to different workers if it is able to discern which worker is willing to work for the low wage, and which worker will only be willing to work for the higher wage. In practice, this often happens when firms can infer different wage requirements for observably different groups of workers. Monopsonistic firms setting wages in this way may explain some of the pay differential between different groups, such as men and women or natives and immigrants.

The monopsony model and wages

The monopsony model leads to dramatically different conclusions about the wage-setting process than does the traditional perfectly competitive model. When deciding how many workers to hire, the firm still weighs the benefit of hiring each additional worker (MRPL) against the cost of hiring one additional worker (MEL). The firm maximizes profits by hiring workers until MRPL is equal to MEL, and by paying workers according to the supply curve at this point. All workers, including the last worker hired, are now more valuable to the firm than the wage they earn. In contrast, in a perfectly competitive market, the last worker hired is paid exactly what they are worth to the firm (MRPL).

The monopsony model and the business cycle

A decline in labor demand will have different effects in perfectly competitive versus monopsonistic labor markets. First, consider a decrease in labor demand that only affects one firm. In a perfectly competitive market, the firm does not have the option to decrease wages because it would lose all its workers to other firms that still pay the market wage; instead, the firm must absorb the entire labor demand shock through a decrease in employment. By contrast, in the monopsonistic market, the firm can compensate for some of the shock by lowering wages without losing its workforce, thus decreasing the impact on firm employment. There is a similar result for a positive demand shock, implying that a monopsonistic labor market should generate less variation in employment but more variation in wages [4].

If an economy wide demand shock occurs, e.g. during a recession, labor supply to individual firms would increase as more unemployed workers search for jobs [4]. This supply increase would put downward pressure on wages in both perfectly competitive and monopsonistic labor markets. However, monopsonistic firms should see a greater fall in wages because the wage they choose to pay will be affected not only by the labor supply increase, but also by their power to set wages. Larger cuts in wages will tend to amplify the effects of a recession, while smaller declines in employment may have the opposite effect. Empirical evidence, presented below, supports this concept, and further indicates that firms’ wage-setting power increases during a recession.

In summary, there are important implications of the monopsonistic model on how both firms and workers experience a recession. Under a monopsonistic model, workers are less likely to be laid off but more likely to experience pay cuts. The option for firms to decrease wages rather than lay off workers should allow them to retain talent during an economic downturn and more quickly return to their pre-recession form once labor demand picks back up. Moreover, the ability to maintain a certain scale of production and save money by cutting wages may increase the number of firms that are able to survive an economic downturn. The types of firms that survive the downturn may also change, as discussed later.

Alternative models and wage-setting

One of the most appealing aspects of the monopsonistic model is that it is conducive to straightforward supply and demand analysis. While intuitively appealing, a simple supply and demand framework abstracts from many aspects of the wage determination process. It is thus worthwhile to briefly discuss some other more complex models. These models generally support the predictions of the monopsonistic model, justifying the straightforward supply and demand approach.

Labor market frictions, such as limited information about the availability of jobs, or job searching costs, prevent workers from flowing without cost and instantaneously between firms that offer different wages. Search and matching models account for these frictions and, in doing so, provide the theoretical foundation for the monopsonistic model. In these models, firms are not constrained to a single market-determined wage. Instead, they either choose their own wage to offer, or hire workers and then bargain over wages after matching with a worker. The firm and the matched worker will bargain over the “match surplus” [5], which is the difference between the lowest wage at which the worker is willing to accept the job (the “reservation wage”) and the value of the worker to the firm. Firms are typically able to bargain to a wage that is less than the value of the worker to the firm. The framework and wage-setting processes in these models explain why firms are able to lower their wages without losing all of their workers. Essentially, they have some wage-setting power and therefore are “monopsonistic” [6].

A simple search model where firms choose the wage to post provides the same prediction as the monopsonistic model of how wages behave over the business cycle. When the economy shrinks, the chances for workers to receive outside job offers decrease, which increases frictions and thus allows firms that advertise a fixed wage to offer lower wages. Recent work has arrived at similar conclusions even when jobs are not interchangeable and thus firms are not identical [7]. Similarly, when firms and workers bargain over wages, a shrinking economy should shift the bargaining power in the firm’s favor [5]. These findings indicate that firms’ wage-setting power increases during recessions, consistent with the more straightforward supply and demand framework of the monopsonistic model.

One shortcoming of predictions from both the search and matching and monopsonistic models is that they typically predict more volatility in wages and less volatility in employment over the business cycle than is observed in empirical data. These findings may be explained in part by “downward nominal wage rigidities,” which are factors not captured in a simple supply and demand model that prevent firms from lowering wages. One source of these rigidities is union contracts. Empirical research on the British and German labor markets has shown that wages are less likely to decline in bad economic times for workers who are covered by a collective bargaining agreement or have other forms of bargaining power. However, frictions imposed by union contracts may be less of a factor nowadays as union power, especially in the private sector, declines. Employers that do not profit maximize may also set wages differently; for example, public sector workers see their wages fall less than private sector workers during a recession. Social norms and preferences over equity could also inhibit a firm’s ability to lower wages. Recent advances in behavioral economics clearly show that individuals care about fairness. Thus, firms may pay high “efficiency wages” due to the above considerations, or if it is costly to monitor workers. Downward nominal wage rigidities should lower volatility in wages over the business cycle. At the same time, they may decrease volatility in employment, as a monopsonistic firm can maintain employment levels at moderately lower levels of demand [4].

Incorporating the framework of efficiency wages into matching models has been found to improve the ability of the model to explain cyclical variations in real wages [5]. Similarly, work in the monopsonistic framework is better able to match firms’ changes in wage-setting power over the business cycle to the wages of new hires than to the wages of workers who are already employed [1]. The similarity in the predictions of these alternative models to the monopsonistic model suggests that the simple supply and demand framework of the monopsonistic model provides a straightforward and accurate way to analyze changes in the real wage over the business cycle.

Measuring monopsony power

Researchers’ understanding of the competitive structure of the labor market has been greatly advanced by empirical work. Payroll data that provide information on wages as well as a worker’s employment start and end dates allow one to measure how worker turnover is related to wages and further infer how labor supply to a firm is related to wages. The concept of elasticity of labor supply to a firm describes how a 1% change in wages affects labor supply; essentially, it describes how steep the labor supply curve is. An infinite competitive value is represented by a flat line (e.g. Figure 1, panel A), while a very uncompetitive value of zero would be represented by a vertical line.

A large body of empirical studies examines the relationship between workers’ pay and job mobility. Two shortcomings of this literature are (i) a lack of direct evidence of how less elastic labor supply to the firm leads to lower pay and (ii) concerns that many empirical studies may not be measuring the causal relationship between earnings and mobility.

Some studies address this issue by following the same workers over a long period of time and by controlling for the time invariant characteristics (often difficult to observe) of a worker [1]. Other studies use “natural experiments” such as changes in public policy to create random variation in wages. Some insight is gained from considering a summary of 25 studies that provide estimates of the elasticity of labor supply to firms, which is the empirical key to understanding how much monopsonistic wage-setting power firms have [8]. Five of the studies used random wage variation, while 20 studies did not. The non-experimental papers yield smaller estimates of the competitiveness of the labor market, but even the results from the experimental approach are still relatively small. The median study estimates an elasticity of labor supply to the firm of 3.3, which predicts that workers are paid around 77% of their worth to the firm, significantly less than the 100% that a perfectly competitive model would predict.

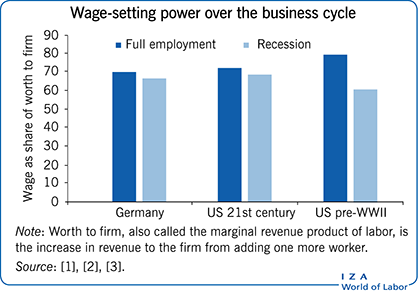

Three non-experimental studies measured firm wage-setting power over the business cycle, using data from the US and Germany [1], [2], [3]. One of the studies examines labor markets between World War I and World War II [1], while the other two employ more contemporary data. Each study finds that the elasticity of labor supply to the firm is lower during poor economic times; in other words, firms are able to drive a larger wedge between productivity and pay during recessions than during upswings. The illustration on page 1 uses data from these studies to show the predicted wage as a share of the last worker’s value to the firm under different economic conditions: the comparisons are between expansions and contractions for the pre-World War II US study; for 4% versus 6% unemployment for the 21st-century US study; and for a 2.5% increase in unemployment in the German study, which employed data from 1985 to 2010. The numbers show that a firm with monopsony power would pay the last worker hired 75% of their value to the firm (MRPL) during good times, and 66% during bad economic times. In other words, an economic downturn could cut wages by about 11%.

The predicted decline of 11%, driven mostly by estimates of a mild recession, seems high but feasible compared to observed declines. For instance, one set of estimates shows declines between 3% and 4% during the Great Recession in the US, though estimates of the decline are over 11% in the UK during the same time period [9]. Still, these results provide compelling evidence from different countries and periods that increased wage-setting power during economic downturns can explain why wages may fall in a recession.

Wages and the business cycle

Increased wage-setting power may cause firms to want to cut real wages during a recession, but it is not entirely clear whether firms are able to do so, and if so, how they will do so. In times of high inflation, firms may freeze nominal wages, allowing inflation to make the pay cut to real wages. However, when inflation is near zero, such as in the Great Recession, firms must lower nominal wages in order to meaningfully cut real wages. As discussed above, lowering nominal wages may be difficult if there are downward nominal wage rigidities. It is therefore necessary to examine empirical research to see if real wages will decrease in a recession.

In the 1990s, the widely held belief was that real wages did not vary over the business cycle. However, the empirical work supporting this view was based on aggregate data, which was not able to control for compositional changes to the labor force during a recession [9]. If recessions lead firms to lay off their least productive, and presumably lowest paid, workers, overall average real wages would increase, thereby obscuring wage declines that occurred because of increased firm wage-setting power.

More recent research focused on following workers who continue to work for the same employer over time. One study found that between a quarter and a third of US workers saw their nominal wages fall between 2011 and 2012. A study from the UK using administrative data, which is generally more reliable than survey data, found even more common wage cuts during this period [9]. Other studies have found similar results for Germany and Portugal, continental labor markets typically characterized as more rigid than the US or UK, in which one would expect there to be stronger downward nominal wage rigidities, thus limiting firms’ ability to cut wages. However, even in a market with rigid wages, firms can adjust wages by cutting bonus pay, allowing firms to apply increased wage-setting power in a recession without changing a contractual wage. These findings suggest that, while nominal wage rigidities may dampen nominal wage decreases, they do not prevent them.

It is also worth considering how productivity changes over the business cycle. In the US, output in the Great Recession fell by 7.16% while total hours worked fell by 10%, implying an increase in productivity. Furthermore, firms may have “squeezed” higher productivity out of their workers during the Great Recession by inducing more effort [10]. Increasing productivity during a recession without increasing wages is another way that firms can enjoy increased wage-setting power.

Implications of the monopsonistic model for business cycles

One effect of recessions is the potential to cleanse the market by reallocating resources from unproductive to productive sectors and firms. If lower quality, less productive firms are more likely to be on the margin of exit from the marketplace, an increase in wage-setting power could help them survive, thereby decreasing the positively viewed cleansing effect. Indeed, recent research shows that this cleansing aspect of a recession was less pronounced during the Great Recession than in previous economic downturns. This would be consistent with increased wage-setting power during a deep economic downturn, as well as increasing monopsonistic power over time as barriers to wage cuts (such as the power of unions, social norms, and the nature of public employment) decline in the labor market as a whole [11].

Another implication of the predicted lower wages in a recession under the monopsonistic model is lower consumption in the economy. In turn, lower demand would lower production, thus creating a vicious cycle in which labor demand falls, generating further employer wage-setting power that leads to even lower wages. Many policy tools used to fight recessions or mitigate the negative consequences of recessions are designed as automatic stabilizers that respond to distress in labor markets by compensating for lost earnings. For example, expenditures on unemployment insurance in the US more than quadrupled during the Great Recession, with more than $80 billion spent on increased benefits alone during 2010 [12]. Programs such as unemployment insurance compensate workers who lose their jobs for lost earnings, but do not help employed workers facing wage cuts. Some important transfer programs such as the 40% wage subsidy earned by some workers under the US Earned Income Tax Credit even exacerbated the effects of wage cuts during a recession: a worker who would receive a $1 an hour wage cut would see their take home pay decline by $1.40, as the removal of the subsidy increased the take home effect of the wage cut.

Instead, policies that directly address wage cuts among the employed could counter the effects of increased firms’ wage-setting power in a recession. One such policy was the 2011–2012 temporary payroll tax cut in the US. Workers saw payroll taxes decrease by 2 percentage points, resulting in a tax cut of approximately $100 billion per year. One estimate suggests that this policy effectively lowered unemployment by 0.8 points and increased GDP by 0.7 points, though the study does not address wages specifically [13].

While a broad payroll tax cut may have effectively stimulated the economy, future research should explore how such a policy could better target those workers most likely to face a wage cut. Simply offering a broad tax cut to all workers potentially facing wage cuts would essentially subsidize wage cuts by firms who may otherwise have not cut wages. However, a more targeted policy that offered temporary tax cuts to workers in industries or local labor markets that were hardest hit by an economic downturn would be less likely to risk this type of strategic response by firms. Such a policy could help to stabilize worker earnings and aggregate demand by countering the wage decreasing effects of increased firm wage-setting power during a recession.

Limitations and gaps

As this article hinges on empirical analysis of firm wage-setting power, it is important to acknowledge that there are two major limitations to these studies. First, little direct evidence exists on the relationship between wages and labor supply. This is important for understanding whether firms are actually able to exercise monopsony power that they may possess. Only one recently published study directly measures the relationship between labor supply to the firm and wages. This study looks at the job market for nurses in the US and finds that firms are able to hire more nurses without having to significantly increase wages, implying a labor supply curve to the firm that looks more like a perfectly competitive market. However, this result could be explained by adjustments in worker quality, where wages may be increasing for workers of a given skill but the firm is hiring lower-skilled workers, or the presence of active unions in this market, which would imply that monopsony power is checked by worker bargaining power and therefore not observable. Several other papers have validated the predictive power of the monopsonistic model by showing that the relative wages between two groups, such as men and women or native workers and immigrants, are proportional to the implied relative wage-setting power over these groups; in other words, the groups’ wages reflect the level of wage-setting power their employers possess.

The second challenge in empirical studies is to identify causal relationships. It is possible that lower-paid workers are more likely to quit because lower wages cause them to search for better paying jobs. However, it is also possible that other factors (such as productivity or motivation) could drive both wages and job search. For example, if less productive/motivated workers receive lower wages and are less able to look for/find new jobs, then empirical results may underestimate the competitiveness of the labor market by attributing too little mobility in response to lower wages. However, even evidence from papers with an experimental design, which would not be subject to this critique, seem to suggest that firms do have wage-setting power.

Summary and policy advice

A monopsonistic model of the labor market suggests that firms have the power to set wages that are lower than would be expected in a perfectly competitive labor market. Empirical evidence from over two dozen studies supports the monopsonistic model of the labor market, and suggests that firms have increased wage-setting power during recessions. An implication of this result is that firms may be able to cut wages instead of employment. The existence of this wage-setting power may help smooth employment over the business cycle, but it could also amplify the cyclicality of wages. This implies that workers may face larger wage cuts in a recession, further decreasing consumption and creating a vicious cycle that extends the length of a recession.

Programs such as unemployment insurance for displaced workers should be complemented by temporary payroll tax cuts to offset declining wages for employed workers, ideally in a way that is targeted toward workers most likely to face wage cuts in the absence of the policy. The importance of addressing falling earnings of employed workers during a recession will further increase as collective bargaining or other barriers to wage-cutting practices continue to decline.

Acknowledgments

The author thanks two anonymous referees and the IZA World of Labor editors for many helpful suggestions on earlier drafts. Previous work of the author (together with Briggs Depew and Peter Norlander) contains a larger number of background references for the material presented here and has been used intensively in all major parts of this article [2], [3].

Competing interests

The IZA World of Labor project is committed to the IZA Guiding Principles of Research Integrity. The author declares to have observed these principles.

© Todd Sorensen