Elevator pitch

Current cohorts of young adults entered adulthood during an international labor and housing market crisis of a severity not experienced since the Great Depression. Concerns have arisen over the impacts on young adults’ employment, income, wealth, and living arrangements, and about whether these young adults constitute a “scarred generation” that will suffer permanent contractions in financial well-being. If true, knowing the mechanisms through which young adults’ finances have been affected has important implications for policy measures that could improve the financial well-being of today’s young adults in the present and future.

Key findings

Pros

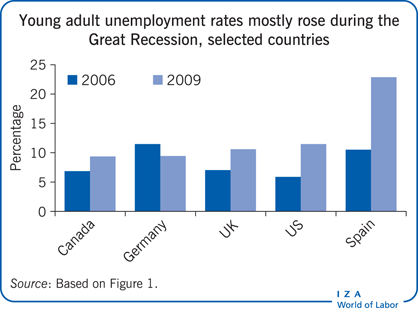

In the Great Recession, young adults in most countries experienced disproportionately high unemployment rates.

Entering adulthood during a recession results in persistent declines in earnings.

Young adults experienced large declines in net worth in the Great Recession, attributable to declining assets and rising debt.

Declines in home and stock ownership among young adults may lead to persistent declines in net worth.

Rates of co-residence with parents increased among young adults in the Great Recession, which is partly attributable to borrowing constraints due to elevated debt-holding.

Cons

Entering adulthood during a recession often leads to increased schooling, which could boost earning power in the future.

Young adults experienced smaller declines in net worth than slightly older adults because they were less invested in housing and stock markets.

Depressed rates of home ownership are not permanent, and ownership gaps typically narrow later in life.

At the same age, young adults in the current cohort have higher asset ownership rates and are less likely to experience financial distress than young adults who came of age around 1989.