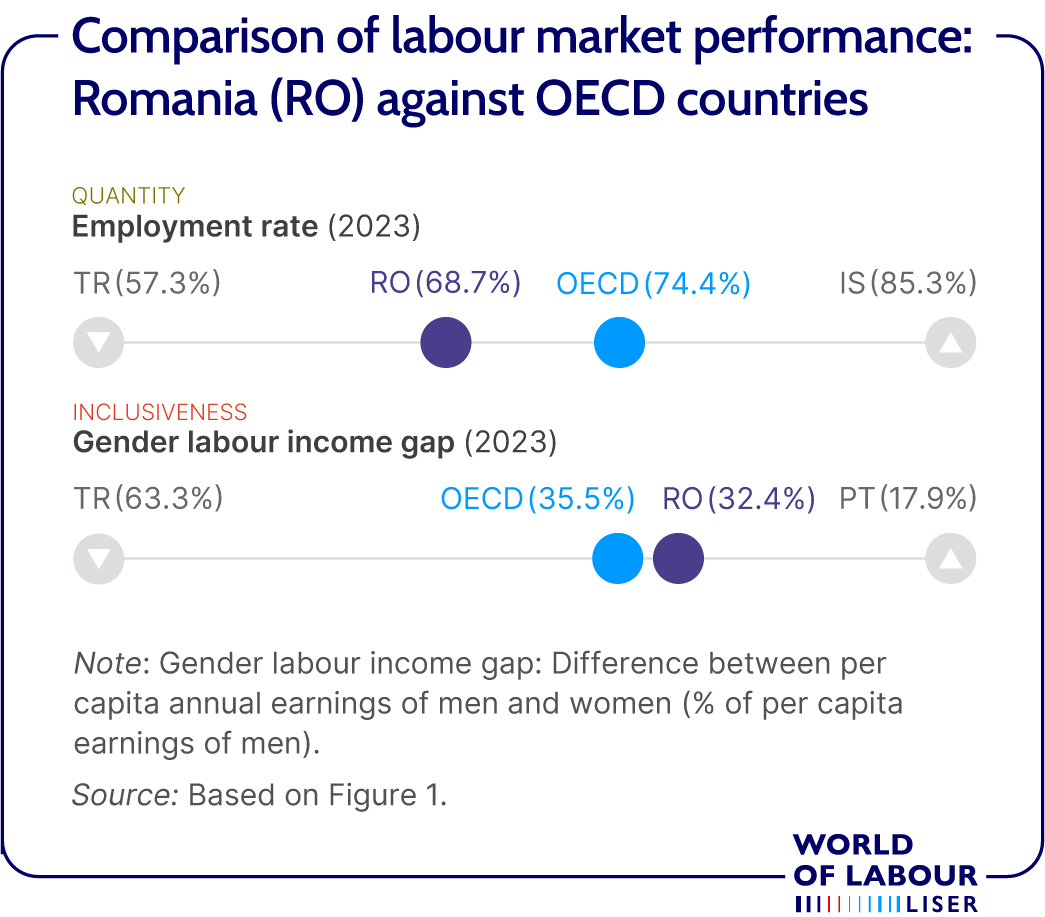

Elevator pitch

Romania’s labour market faced major structural challenges from 2000 to 2024. Employment rates have risen, but the number of employed individuals has reduced mainly due to demographic decline and emigration. The workforce is aging and young people face difficulties in transitioning from education to employment. Persistent disparities by gender, region, area of residence, education, and age constrain labour supply and deepen inequalities. Limited public resources and institutional and legislative weaknesses limit the effectiveness of labour market integration policies for vulnerable groups and allow informal employment to persist.

Key findings

Strengths

The overall employment rate increased from 2000 to 2024, despite adverse demographics.

Unemployment and long-term unemployment have remained relatively low over the past decade.

Wages have grown consistently over time, supporting living standards and reducing in-work poverty among employees.

The introduction of an objective minimum wage setting and data-driven tools for skills anticipation and labour market policies evaluation strengthens labour market governance.

Weaknesses

Chronic structural inequalities limit labour market participation and reinforce social and territorial disparities.

Romania faces persistently low employment rates for women, young people, low-educated, rural residents, and other disadvantaged groups.

Youth unemployment and NEET (not in education, employment, or training) rates are particularly high, indicating that young people face challenges transitioning from education to employment.

Undeclared work remains widespread and regionally concentrated, weakening worker protection and reducing tax revenues.

Very low public spending on unemployment and activation policies reduces the effectiveness of support for jobseekers and vulnerable groups.

Author's main message

Romania’s labour market is facing persistent territorial and socio-demographic disparities, despite increasing overall employment. Major difficulties in integrating young people, women, people with disabilities, and those residing in rural areas or less developed regions have exacerbated inequalities. Addressing them would imply prioritizing policies that expand labour supply and increase job quality, such as promoting flexible and adapted working arrangements, funding training and job-matching, scaling up childcare and other dependent care, and intensifying efforts to reduce informal employment.

Motivation

Romania’s labour market presents a notable paradox. Although employment rates have increased steadily, the country has nearly three million fewer workers than at the beginning of the century. Economic growth, rising wages, and persistent labour shortages occur alongside one of the most rapidly shrinking and ageing workforces in Europe. This contrast between apparent labour market strength and underlying structural fragility provides a framework for examining how demographic change and unequal access to employment are transforming Romania’s economy.

Discussion of strengths and weaknesses

Overall labour market trends

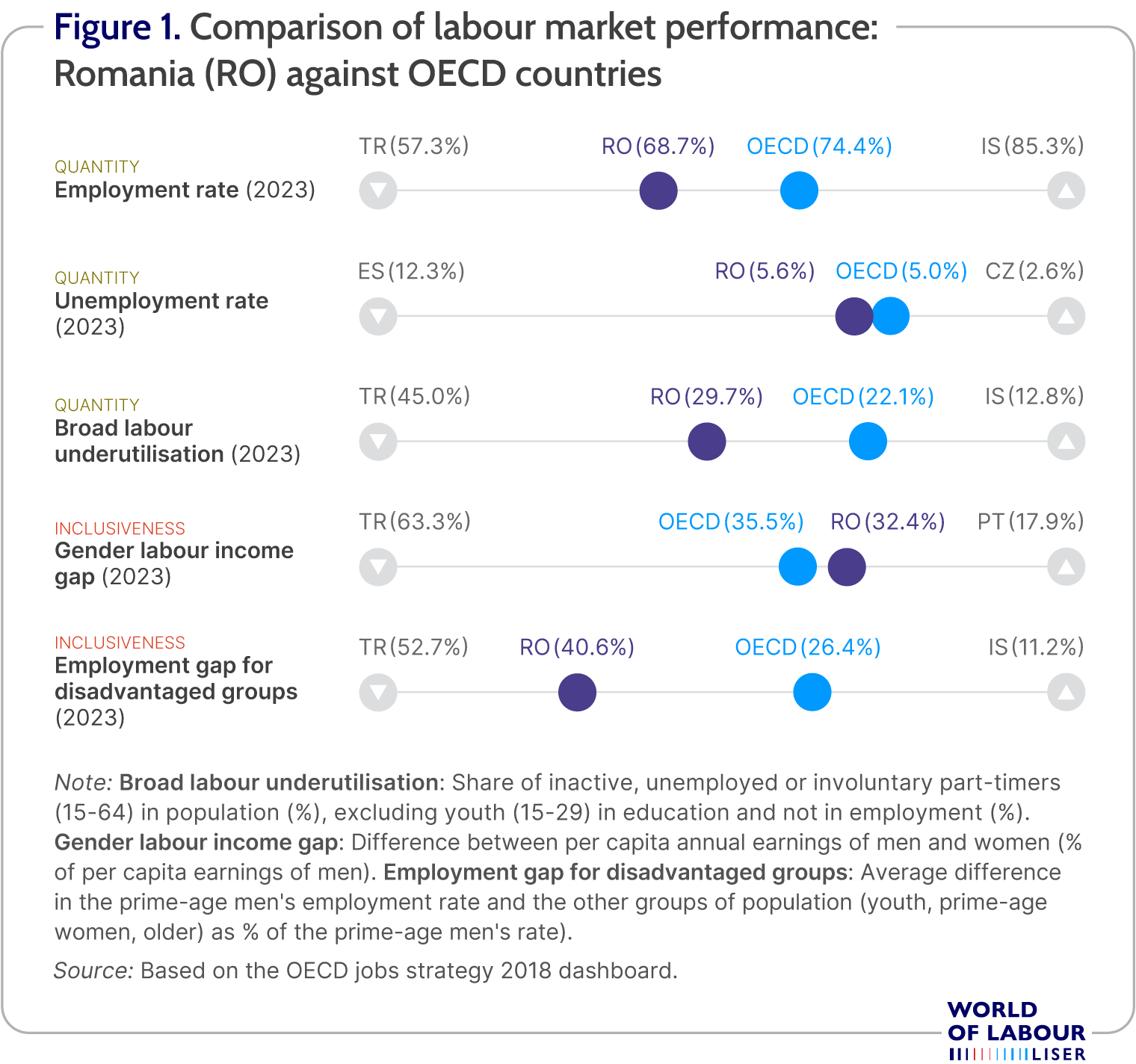

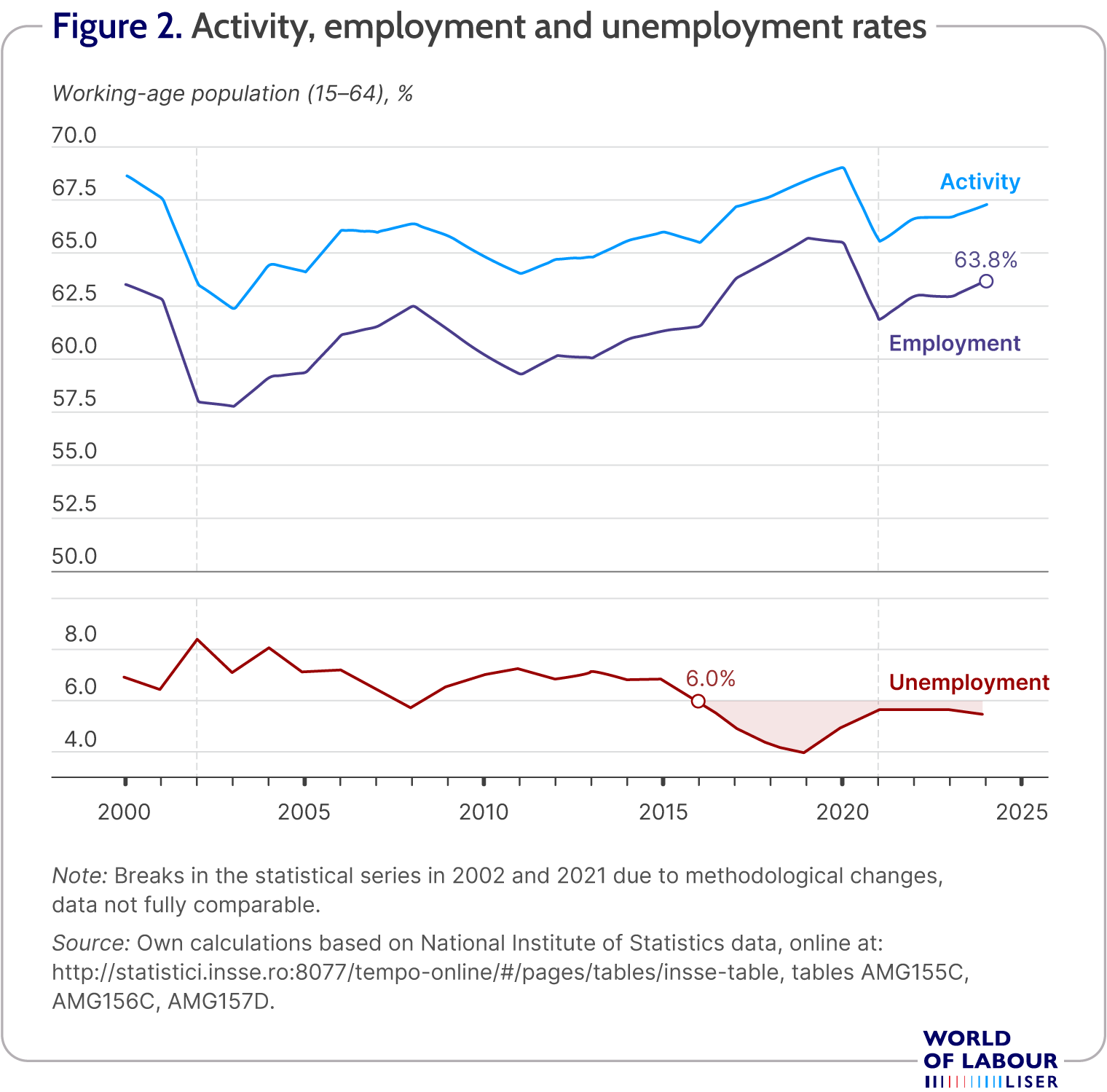

Over the past two decades, employment in Romania has increased, and the employment rate for the working-age population (those aged 15-64 years) reached 63.8% in 2024 (Figure 2). However, this rate remains low compared with other EU and OECD countries, reflecting deep structural challenges and changes in the labour market. Although the employment rate has improved, the total number of employed individuals declined sharply from 10.5 million in 2000 to 7.8 million in 2024, mainly due to demographic decline and migration. Consequently, the workforce has aged, with a higher share of older workers and fewer young entrants. Two significant declines in employment in 2002 and 2021 were mainly due to methodological changes that disrupted the continuity of the time series. The 2021 adjustment is especially important, as individuals who were self-employed in agriculture for own consumption (approximately 800,000 people in 2021) were reclassified and excluded from the employed and active population.

Wage employment dominates the Romanian labour market, accounting for more than 85.3% of workers. Self-employment accounts for approximately 12% of total employment, a share comparable to EU benchmarks, and is concentrated primarily in agriculture and rural areas (73.2% in 2023). Although the share of unpaid family workers has declined over time (from 19.7% in 2000), they still account for about 2.7% of the employed population, indicating the persistence of informal and subsistence-oriented work, that is work done primarily to meet basic needs of survival. Notably, 10.9% of all employed individuals are at risk of poverty, while the risk rises to 52.7% among self-employed and unpaid family workers.

Wage employment dominates the Romanian labour market, accounting for more than 85.3% of workers. Self-employment accounts for approximately 12% of total employment, a share comparable to EU benchmarks, and is concentrated primarily in agriculture and rural areas (73.2% in 2023). Although the share of unpaid family workers has declined over time (from 19.7% in 2000), they still account for about 2.7% of the employed population, indicating the persistence of informal and subsistence-oriented work, that is work done primarily to meet basic needs of survival. Notably, 10.9% of all employed individuals are at risk of poverty, while the risk rises to 52.7% among self-employed and unpaid family workers.

The activity rate for people aged 15-64 years has remained stable at approximately 66-67% in recent years, while unemployment has generally remained below 6% over the past decade (see Figure 2), and long-term unemployment has stayed around 2%. However, the inactive population is growing. In 2024, 2.4 million individuals aged 25-64 years were inactive; of these, 58.8% lived in rural areas, 39.3% had no more than lower-secondary education, and 70.1% were women. This highlights a structural challenge, as institutional and legislative weaknesses limit the effectiveness of labour market integration policies for vulnerable groups, including women, rural residents, people with disabilities, and young people. These problems are exacerbated by limited local employment opportunities and insufficient childcare and dependent-care services, particularly in rural areas. The disparity is especially pronounced in early childhood care provision: although the population of children under the age of seven is about 30% higher in rural areas than in urban areas, 91.6% of nurseries and kindergartens are located in urban areas. These factors significantly restrict labour market participation, particularly for women and younger adults in rural communities [1].

The Romanian labour market shows clear divides by gender, area of residence (rural versus urban), age, economic activity, and region. The following sections will examine these segmentations in more detail.

Gender and rural-urban gaps

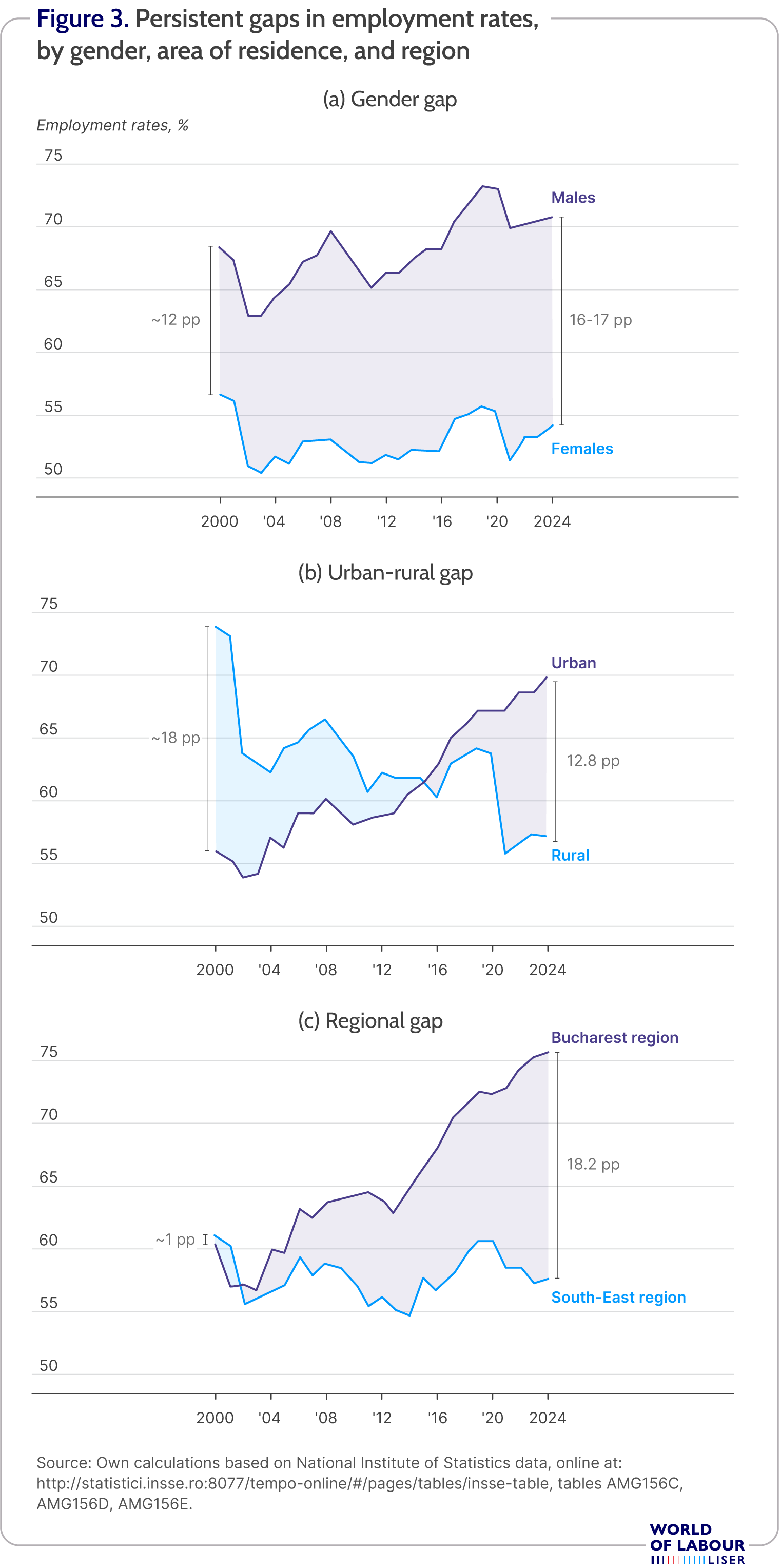

A persistent feature of the Romanian labour market is the substantial employment gap between men and women, which is about 16 to 17 percentage points. This gap has increased in recent years after narrowing during the 2000s, as it can be noted in Figure 3. Limited use of flexible work arrangements contributes to this difference: only 1.4% of total employment is part-time (the same share among women), compared to OECD averages of 15.1% overall and 22.8% for women. Fiscal legislation further discourages part-time work, as social contributions are calculated based on the statutory minimum wage, even for reduced working hours and lower wages. The minimum contribution base aimed at preventing wage underreporting was introduced in 2017, removed in 2019, and reinstated in 2022.

A significant urban-rural employment gap continues to exist, at approximately 12.8 percentage points in 2024, in favour of urban areas (see Figure 3). The 2021 methodological change, which excluded subsistence self-employment in agriculture from employment statistics, produced the most pronounced decline in rural employment since 2001. Over the long term, Romania has shifted from a predominantly agricultural workforce (43.9% of employed population in 2000) toward services and industry. However, the country still has the highest share of employment in agriculture, forestry, and fishing in the EU (10.9% in 2024, compared to the EU average of 3.2%).

A significant urban-rural employment gap continues to exist, at approximately 12.8 percentage points in 2024, in favour of urban areas (see Figure 3). The 2021 methodological change, which excluded subsistence self-employment in agriculture from employment statistics, produced the most pronounced decline in rural employment since 2001. Over the long term, Romania has shifted from a predominantly agricultural workforce (43.9% of employed population in 2000) toward services and industry. However, the country still has the highest share of employment in agriculture, forestry, and fishing in the EU (10.9% in 2024, compared to the EU average of 3.2%).

Regional disparities

Regional segmentation is especially marked, with the distance between the least and the most developed regions widening steadily, especially after 2015. Bucharest-Ilfov has emerged as the dominant economic area, attracting a disproportionate share of financial resources and highly skilled labour compared to other regions. This concentration has led to a growing employment divide: in 2024, the employment rate gap between Bucharest-Ilfov and the South-East region, the weakest performer, reached 18.2 percentage points (Figure 3). Even the North-West region, the next best-performing area, has fallen further behind Bucharest-Ilfov.

These disparities are closely tied to regional economic structures. Bucharest-Ilfov benefits from a concentration of high-productivity industries, including information and communication technologies, financial and professional services, public administration, and high-value-added manufacturing. In contrast, least developed regions rely more on low-productivity manufacturing, agriculture, and traditional services, which offer fewer jobs and lower wages. Limited industrial diversification, weaker infrastructure, and lower administrative capacity additionally limit job creation outside the capital region, reinforcing persistent regional inequalities. EU Cohesion Funds are supporting the development of less developed regions by improving infrastructure, business and human capital, local administrative capacity and public services. While Cohesion Policy has reduced to some extent territorial disparities, it has not reversed the overall trend of regional divergence, as Bucharest-Ilfov continues to benefit from structural advantages. The effectiveness of these funds across regions is clearly influenced by local governance and initial levels of development [2].

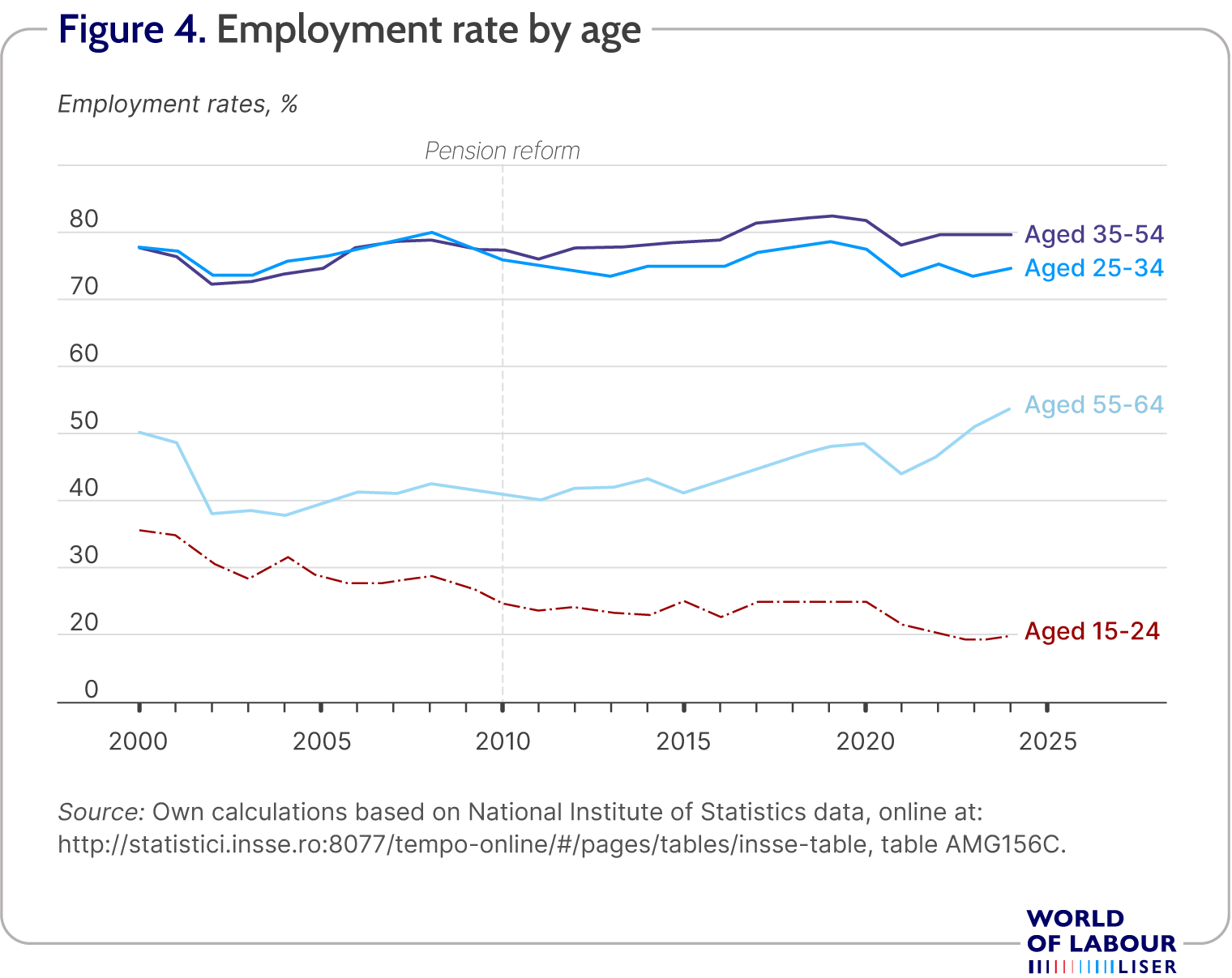

Age segmentation and an ageing workforce

Employment rates for young people (aged 15-24) have declined, remained stable for prime-age workers (aged 25-54), and increased substantially for older workers (aged 55-64), as it is shown in Figure 4. Reforms such as Pension Law no. 263/2010 discouraged early retirement by requiring longer contribution periods, following a wave of early retirements in the early 2000s. The share of workers aged 35-49 years rose from 33.6% to 42.8%, making this the largest group, while those aged 50-64 years rose from 19.4% to 30.9%, reflecting the aging of larger cohorts born in the 1960s and 1970s. In contrast, youth employment declined sharply (from 11.5% to 5.1% for ages 15-24 and from 25.5% to 20.2% for ages 25-34) due to lower birth rates and longer periods in education. Youth unemployment remained high at 23.8% in 2024, alongside a high rate of those not in education, employment, or training (NEET), 19.6% among 15-29-year-olds, indicating that many young people face challenges transitioning from education to employment.

High emigration, which began in the 1990s and intensified after Romania's EU accession in 2007, has further influenced these trends. According to international migration data, by mid-2024, approximately 4.6 million Romanians resided abroad, representing about a quarter of the resident population, while the immigrant stock was estimated at around 655,000 people in 2024. Although immigration could partially address workforce age imbalances, it is mainly concentrated in low-skilled occupations.

High emigration, which began in the 1990s and intensified after Romania's EU accession in 2007, has further influenced these trends. According to international migration data, by mid-2024, approximately 4.6 million Romanians resided abroad, representing about a quarter of the resident population, while the immigrant stock was estimated at around 655,000 people in 2024. Although immigration could partially address workforce age imbalances, it is mainly concentrated in low-skilled occupations.

Education structure

Regarding employment by education, Romania shows a distinct pattern compared with most EU countries. The share of tertiary-educated workers remains relatively low, at around 23% in 2024, and has increased only marginally over time, in contrast to the EU average of 38.7%, which continues to rise. The modest expansion of tertiary employment in Romania points to both supply-side constraints, such as lower higher-education attainment and migration of graduates, and demand-side factors, including the still modest presence of high-value-added, knowledge-intensive industries outside major urban centres.

By contrast, employment among individuals with medium levels of education has grown substantially, from 54.7% in 2000 to 63.5% in 2024 – the opposite of the prevailing EU and OECD trend, where the share of medium-educated workers in employment has tended to decline as economies shift toward higher-skill profiles (EU average: 45.6% in 2024). In Romania, this pattern reflects the continued importance of medium-skill occupations in activities such as manufacturing, construction, transport, and agriculture, as well as the slower speed of technological upgrading and digitalisation across much of the economy.

At the lower end of the educational distribution, labour market vulnerability remains pronounced. Among individuals with low levels of education (according to the International Standard Classification of Education, ISCED, a score of only 0-2), the employment rate is at just 36.9%, well below the EU average of around 46%. This group is disproportionately concentrated in rural areas and declining sectors such as subsistence agriculture. It faces multiple barriers to labour market participation, including limited access to training, poor transport connectivity, and weak local labour demand. Low education is therefore closely connected with long-term inactivity, informal work, poverty, and contributes to the reproduction of social inequalities [3].

Wages, taxation, and minimum wage dynamics

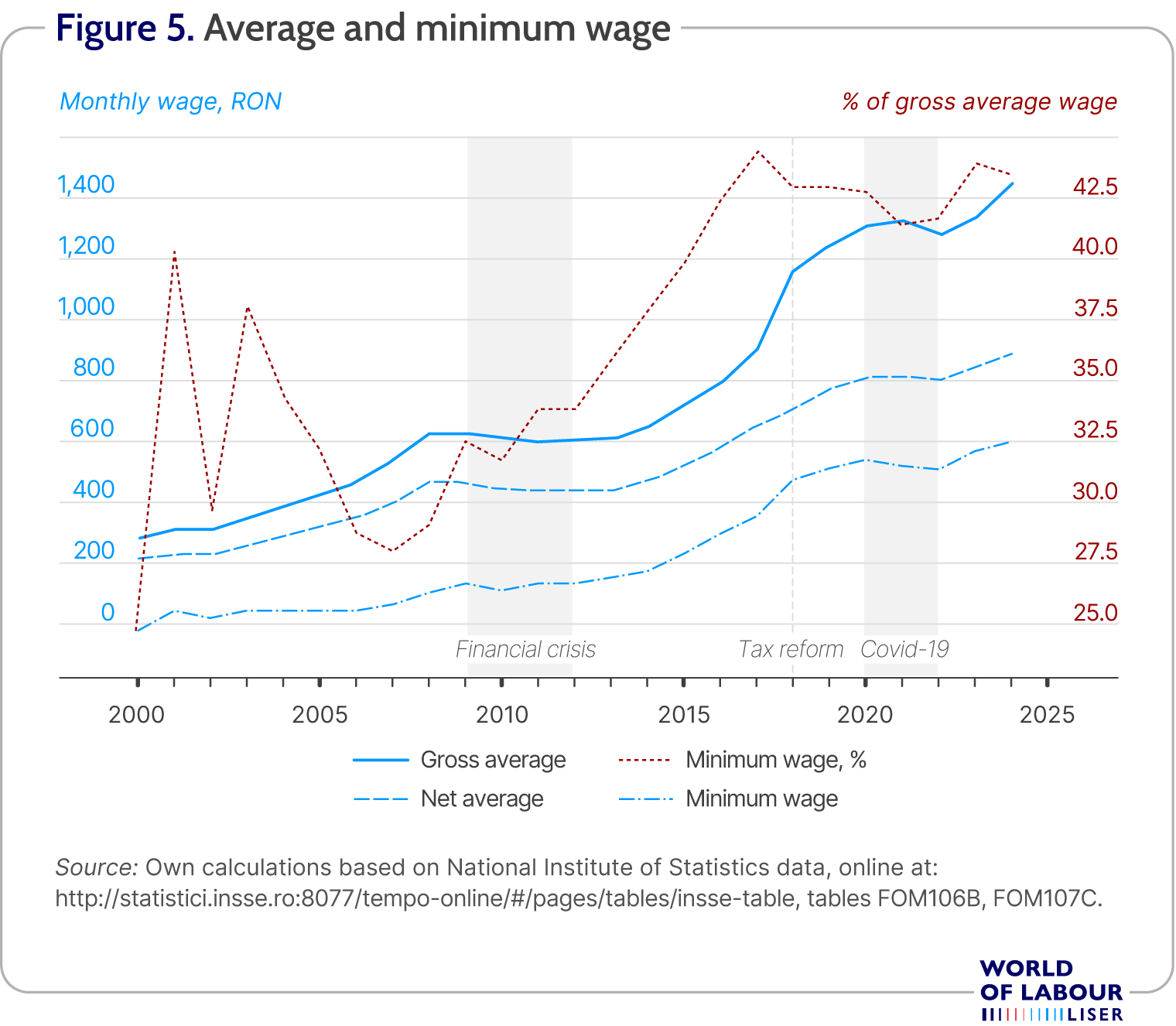

Wages have risen steadily over time, with visible setbacks during the 2009-2012 financial crisis and the 2020-2022 pandemic (Figure 5). In 2024, average monthly net earnings were around 1,055 Euros (about 43% of the EU average). The gap between gross and net wages has widened, partly due to the 2018 social contributions reform, which shifted most social security contributions from employers to employees. However, Romania has one of the highest labour tax wedges in the EU: 36.9% for the average wage and 36.0% for 67% of the average wage (2024), compared with EU averages of 29.9% and 24.9%, respectively. This is notable given Romania’s comparatively low wage levels and reflects a labour tax structure that relies heavily on employee social security contributions, with consequences for work incentives and informal employment.

The statutory minimum wage has risen rapidly since 2016, compressing the lower end of the wage distribution. According to the Romanian Ministry of Labour, about 14.6% of employees earn the minimum wage, and another 16.3% earn near-minimum wages (up to 6.7% above the minimum wage) [4]. A planned mid-2026 increase of the minimum wage may push a significant share of near-minimum workers onto the statutory floor, potentially raising the share of minimum-wage earners above 30%. While this can support low-income workers (to note that only 4.8% of employees were at risk of relative poverty in 2024), its sustainability depends on careful coordination with labour taxation to avoid negative employment or undeclared work effects [5].

The statutory minimum wage has risen rapidly since 2016, compressing the lower end of the wage distribution. According to the Romanian Ministry of Labour, about 14.6% of employees earn the minimum wage, and another 16.3% earn near-minimum wages (up to 6.7% above the minimum wage) [4]. A planned mid-2026 increase of the minimum wage may push a significant share of near-minimum workers onto the statutory floor, potentially raising the share of minimum-wage earners above 30%. While this can support low-income workers (to note that only 4.8% of employees were at risk of relative poverty in 2024), its sustainability depends on careful coordination with labour taxation to avoid negative employment or undeclared work effects [5].

Since 2025, Romania has introduced an objective adjustment mechanism for the minimum wage through Government Decision No. 35/2025, which establishes the annual procedure for determining the minimum wage, in line with both national legislation and European requirements (Directive EU 2022/2041 on adequate minimum wages in the EU). Under this mechanism, the minimum wage is updated annually based on expected inflation and real productivity growth and is further negotiated with social partners in the National Council for Tripartite Dialogue within a 47–52% corridor of the average gross wage. Also included in the mechanism, there is an annual impact evaluation of minimum wage effects on employment, labour costs, poverty and other relevant socio-economic indicators [6]. The minimum wage was around 800 Euros per month in 2025, placing Romania in the lower part of EU countries, but in the upper half when measured in purchasing power parity (ppp) terms. The minimum wage represents around 41–42% of the average wage (2024, see Figure 5), while the minimum-to-median wage ratio is about 62%.

Wage inequality and sectoral differentials

Wage levels differ substantially across sectors, largely reflecting variations in labour productivity. ICT, finance and insurance, and energy production and distribution offer the highest wages, while hotels and restaurants, agriculture, and real estate provide the lowest, often paying two to three times less on average.

Romania’s gender wage gap is notably low, at approximately 4% in 2024, compared with an OECD average nearly three times higher. Nevertheless, overall earnings inequality remains pronounced: the top 10% of earners are paid about 4.3 times as much as the bottom 10% (2022), exceeding the OECD ratio of 3.2. Increases in the minimum wage have not fully mitigated other sources of inequality, including the high share of low-skilled workers and unequal access to employment in rural and less developed regions.

Labour shortages and skills mismatches

Labour shortages are widespread, affecting high-, medium-, and low-skilled occupations. The 2025 CEDEFOP skills labour shortage index points to severe shortages among professionals in various fields (business and administration, ICT, legal/social/cultural fields, and science and engineering). These shortages are generally driven by demand pressures. In particular, ICT and science/engineering shortages are reported at very high levels across all dimensions: demand, supply, and imbalance, while the EU average is only moderate in their cases. This reinforces the need for directed education in ICT, science, and engineering, as well as measures to attract and retain talent. The share of ICT specialists in total employment is 2.6% (2024) and declining, compared with an EU average of 4.8%.

For medium-skilled and elementary occupations (e.g., personal care, cleaning, refuse collection, food preparation, driving, assembly), shortages are more supply-driven, reflecting replacement needs from retirement and other frictions.

Skills mismatches are pronounced among professionals and workers in mining, construction, manufacturing, transportation, and agriculture, forestry, fisheries. These mismatches are expected to intensify as digital and green activities expand. Only 27.7% of Romania’s population has at least basic digital skills [7], compared with an EU average of 55.6%, underscoring the urgency of expanding digital skills across education and training. While existing studies and data provide information on shortages by occupations and broad macroeconomic trends, there is a lack of regional and sector specific approach, relevant in the Romanian labour market context [8].

Adult participation in learning has risen significantly over the past two decades, from 0.9% in 2000 to 8.9% in 2024. This trend shows growing recognition of lifelong learning and the expansion of EU-supported training programs. However, participation in adult learning in Romania remains low compared to the European benchmark of 13.5%. Persistent barriers include limited access to training in rural areas, low employer investment in skills development, time and cost constraints for workers, and insufficient incentives for low-skilled and older adults to pursue upskilling or reskilling.

To strengthen alignment between education and labour market needs through a strategic, coordinated tool, important steps have been taken through the ReCONECT Platform. This innovative digital initiative, developed by the National Agency for Employment together with other national authorities and institutions, integrates large-scale administrative data from multiple public institutions to create an integrated mechanism for anticipating, monitoring, and evaluating labour market demand, education, and vocational training.

Also, fiscal incentives (lower social contribution and income tax rates) and sector specific statutory minimum wages, higher than the national statutory minimum wage, introduced in 2019 for the construction and agriculture sectors were designed to address labour shortages, reduce informality, and increase competitiveness. These measures were intended to raise earnings without increasing total labour costs. In construction, employment stabilised and even increased; in agriculture, effects are less clear given strong seasonality, subsistence work, and informality. Nevertheless, these incentives did not resolve more profound structural issues such as low productivity and low skills in these sectors. By 2025, all such fiscal incentives were fully abolished after a gradual phase-out that began in 2023.

Labour market institutions and financing

Public spending on unemployment in Romania is extremely low—the lowest in the EU—at only about 0.03% of GDP, compared with an EU average of 1.04% (according to 2023 Eurostat data). This severe underinvestment limits both the scale and effectiveness of labour market interventions. The composition of spending also raises concerns about potential impact: more than one-third of available resources are allocated to employer incentives for hiring vulnerable groups. Another third is absorbed by unemployment benefit payments. This leaves very limited funding for core activation measures such as training, upskilling, personalized counselling, or job-matching services.

At the same time, unemployment benefits are low, providing only weak income protection. As a result, the effective earnings losses associated with unemployment are considerable: around 55% for minimum-wage earners and as high as 66% for average-wage earners, even after accounting for the potential take-up of other social benefits. This combination of low benefit generosity and limited activation support increases the risk of poverty during unemployment while doing little to enhance re-employment prospects or job quality. In this context, the ReCONECT Platform, already mentioned, represents an important asset, as it will generate systematic impact evaluations of active labour market measures, helping to identify which interventions are effective and where resources could be better targeted.

Structural constraints are also evident in the client profile served by the Public Employment Services (PES). According to the National Employment Agency's Annual Activity Report (2024) National Employment (2024) [9], around two-thirds of PES clients are aged 40 or older, 73% come from rural areas, and more than 64% are assessed as having low or very low employability. At the same time, labour demand mediated through PES is heavily concentrated in unskilled or low-skilled occupations. This reinforces a low-skill equilibrium in which limited job opportunities coexist with limited incentives and opportunities for upskilling.

Informal employment

Informality is a structural feature of the Romanian labour market, with the highest rates of undeclared and unobserved employment in the EU. Recent evidence from a national assessment developed within the Informality Data Research Lab Nat Scientific Research Institute shows that informal employment has remained high throughout 2000–2024, generally exceeding 15% of total employment and rising to nearly 30% after 2021. While the early 2000s reflected the social costs of post-transition restructuring, EU accession in 2007 brought only partial and temporary stabilization. More recent dynamics indicate that economic recovery and growth have not translated into durable formalization, confirming that informality in Romania is not purely cyclical but deeply embedded in institutional arrangements, sectoral structures, and labour market exclusion.

Regional evidence reinforces this conclusion and highlights a pronounced territorial dimension. Estimates reveal extreme differences across regions, with shadow economy shares ranging from very low levels in Bucharest–Ilfov to exceptionally high figures exceeding 40% in structurally weaker regions such as South-West Oltenia and North-East. Romania closely follows the Central and Eastern European pattern, in which capital regions consistently exhibit the lowest levels of informality, benefiting from better economic opportunities, stronger companies and institutions. However, it stands out for the severity and persistence of informality in its peripheral, predominantly rural regions, where agricultural dependence, poverty, and limited enforcement capacity reinforce reliance on undeclared work. Since different methodologies capture distinct aspects of informal economic activity estimates may vary but provide complementary insights.

Together, national and regional evidence shows that informality in Romania is both widespread and spatially concentrated, with significant policy implications. National-level reforms, though essential, are insufficient on their own. In recent years, labour inspectorates have intensified enforcement against undeclared work, including targeted inspections in high-risk sectors such as construction, agriculture, and hospitality, as well as coordinated campaigns involving cooperation between labour, tax, and social security authorities [10]. But evidence indicates that formalization strategies must extend beyond enforcement. Fiscal incentives for the agriculture and construction sectors (2019–2025) were also designed to reduce informal employment and enhance sector attractiveness. Romania’s alignment with European labour standards will ultimately require place-sensitive policies that integrate effective control mechanisms, incentives for formal job creation, and targeted measures to address long-term structural exclusion in regions with high informality.

Limitations and gaps

Series with methodological breaks were included in the analysis because the recalculation carried out by the National Institute of Statistics based on the most recent methodology covers only the period 2009–2024. The analysis would have benefited of a more in-depth investigation of employment if data on employment at the intersection of gender and area of residence would have been available.

Summary and policy advice

Romania’s labour market between 2000 and 2024 combines improving key indicators with deep structural weaknesses. Employment rates have increased and unemployment has remained low, while wages have grown steadily, yet the total number of employed people has fallen sharply due to demographic decline and sustained emigration, resulting in an ageing and increasingly constrained workforce. Activity remains low by international standards, with a large inactive population concentrated among women, young people, rural residents and people with low education. Persistent divides by gender, region, age and education, together with high levels of informal employment, limit labour supply and social inclusion. At the same time, labour shortages coexist with significant skills mismatches, reflecting weak links between education, training and labour market needs, as well as still low participation in adult learning despite recent progress. Labour market institutions are underfunded, providing limited income protection and insufficient support for activation, upskilling and job matching. Overall, the evidence shows that recent improvements have not changed the underlying structural constraints.

From a policy perspective it is important to recognize that long-term economic growth and social cohesion depend on policies that expand effective labour supply and raise job quality, notably through stronger activation and training systems, improved care services, reduced incentives for informality, and targeted interventions to narrow regional and social disparities.

Acknowledgments

The author thanks the anonymous referee(s) and the World of Labour editors for helpful suggestions on earlier drafts.

Competing interests

The World of Labour project is committed to the European Code of Conduct in Research Integrity. The author declares to have observed the principles outlined in the code.

© Eva Militaru