Elevator pitch

While Mexico has improved the education of its labor force, maintained a stable macroeconomic environment, and been friendly to international trade, its labor market still faces many challenges. In particular, Mexico has difficulty creating high-paying jobs: the share of informal employment has remained stagnant for the last 20 years, and, by 2025, remains above 50%. These problems are particularly poignant in southern Mexico.

Key findings

Strengths

Mexico’s labor market has a low unemployment rate.

Wage inequality has decreased substantially.

The education of the labor force increased in the last two decades.

International trade with the US sustains manufacturing labor demand.

Proximity to the US provides migration opportunities.

Weaknesses

Mexico is the second country with the most working hours per year in the OECD.

The country has a large informal sector, where wages and productivity are low.

Gender wage gaps persist, and the labor force participation rate of women remains low.

Some regions of Mexico continue to lag in income and development indicators.

Author's main message

Mexico’s economy has many advantages, such as a young and ever-more educated labor force, and relatively privileged access to trade with the US, the largest market in the world. However, these factors have not translated into substantial wage growth for most Mexicans over the last two decades. Policies should promote labor demand, particularly for high-skilled workers, and facilitate the creation of formal jobs.

Motivation

Mexico is a large upper-middle-income country. It shares several characteristics with the rest of Latin America, including a large informal economy and lower levels of human capital and wages than in more developed countries. However, Mexico stands out due to its proximity to the US, which translates into a vigorous labor demand in export-oriented manufacturing and a historically strong motivation and opportunity for international migration. These factors have favored the Mexican labor market, although unevenly, leading to substantial regional disparities.

From 2005 to 2025, Mexico has faced and recovered from two significant recessions. During this period, the country experienced an increase in the education of its labor force, a stable macroeconomic environment, and trade openness. However, real wages have remained mostly steady except for the last six years. The informal economy is still quite large, female labor force participation is low, and the share of Mexicans working and living in poverty is high, although it has diminished recently.

Discussion of strengths and weaknesses

Low unemployment rates, but low female labor force participation

Mexico’s working-age population has grown steadily since 1990, and the country’s labor force remains relatively young compared to those of OECD countries. For example, while the old-age (65 or older) to working-age (15 to 64 years old) population ratio was 28% in 2023 for OECD countries, in Mexico it was 18%.

While Mexico’s fertility rate is the second-highest among OECD countries, at 1.91 children per woman as of 2023, it has been declining since 2005 and fell below the replacement rate in 2016. An upcoming challenge for Mexico’s labor market is the aging of its population as its fertility rate approaches that of high-income countries, and female labor force participation catches up to that of men.

In 2020, 65% of Mexico’s population was working-age, and the average worker was 40 years old. This healthy labor supply has been mostly absorbed into the labor market, leading Mexico to have one of the lowest unemployment rates among OECD countries, averaging 4.1% for 2005-2024, well below the OECD average of 6.6% and the Latin-American average of 7.1%.

Mexico’s labor market is highly segmented by gender. The female labor participation rate is about 30 percentage points lower than that of males, and by 2025, it was well below those of OECD and Latin American countries (67.1% and 52.1%, respectively). International evidence shows that a low female participation rate may be detrimental to growth and productivity. Mexico’s low female labor participation has been linked to supply factors, such as the high demand on women to provide care for other household members. There has been some progress in improving female job participation: the participation rate of women almost doubled from 1990 to 2010 [1], partly induced by changing social roles, a shift to services, and to large-scale conditional cash transfers that tended to improve employment opportunities for women [2]. However, since 2010, the increase in women’s labor force participation rates has slowed (Figure 2).

These gender gaps are also present in wages: on average, by the second quarter of 2025, a woman in Mexico earned 85% of the hourly labor income of a man (Figure 3, Panel a). This gap, however, has recently closed as overall wage inequality in the country has dropped. While wage dispersion remained relatively stable from 2005 to 2018, it decreased substantially after 2018, with the creation of separate minimum wages for the areas bordering the US and for the rest of the country, and substantial minimum wage increases of 375% from 2018 to 2025 in the border areas and 215% elsewhere. Wage inequality has decreased primarily because of a decline in lower-tail inequality (Figure 4), and has benefited the poorest areas of the country (the South, Figure 3, Panel b).

Migration, trade, and regional dynamics

International migration

Mexico borders the US to the north, which is the world’s largest economy. This proximity, along with large wage differentials between the two countries, has induced important net migration to the US [3]. As of the start of 2025, an estimated 11 million Mexican-born persons were in the US, representing around 8% of all Mexicans (Mexican Population Census and American Community Survey). Migration has tended to equilibrate local labor markets by decreasing labor supply in low-wage places of origin: the segments of the labor market with the most emigration–mainly younger men in the central and western regions of Mexico–have seen wages increase due to the reduced labor supply at the local level [4].

Recently, migration flows from Mexico to the US have decreased and are now small, and sometimes negative. Reduced net flows result from factors including slower population growth and improved labor market conditions in Mexico, aging migrant populations in the US, and intensified immigration enforcement [5]. These factors have induced some return migration, meaning that some Mexicans who lived and worked in the US for many years are relocating back to Mexico. Return migration can generate its own dynamics, as returnees often bring valuable human, social, and financial capital that can foster entrepreneurship, stimulate local investment, and raise productivity in their places of origin [6].

Export-oriented labor

The US and Mexico liberalized trade between them with the signing of NAFTA (North American Free Trade Agreement) in the mid-1990s. As a consequence, Mexico developed a significant export-manufacturing sector: by 2025, 27% of private-sector formal jobs were in firms that exported to the US. Given its relative abundance of unskilled labor, Mexico’s exports have focused on goods that are more unskilled-labor-intensive, as predicted by trade theory. Consistent with theory, employment and wages rose following liberalization, particularly among the lower-skilled and in the northern region closest to the US [7].

With a larger export sector, Mexico has increased its exposure to international trade shocks, particularly in the northern region, which has specialized more heavily in export manufacturing. Employment and wages in Mexico’s northern border states grew more after NAFTA. However, this region also saw more intense negative effects from Chinese competition after China entered the WTO in 2001 and in the aftermath of the global financial crisis in 2008. More recently, the US-bordering states saw a stronger recovery in labor markets following the Covid-19 shock, buoyed by US manufacturing demand growth.

The United States-Mexico-Canada Agreement (USMCA) trade agreement, an updated version of NAFTA, came into effect in 2020. This new agreement pushed Mexico, Canada, and the US to increase the use of “Rules of Origin”, under which the countries agree to use production inputs from the common trade area. While existing research has shown that such Rules of Origin decreased intra-regional trade volume, their effects on employment remain an open question. Finally, the USMCA pushed the creation of legal resolution centers that helped mediate conflicts between employees and employers.

Persistent regional differences

The uneven exposure of Mexican regions to the US economy adds to long-run differences in economic fundamentals within Mexico, resulting in significant heterogeneity across regional labor markets [8]. Figure 3, Panel b, shows that throughout the study period, average real wages were highest in the northern region, followed by the north-central, central, and southern regions. These stark regional wage differences persist even after a period of recent wage growth. The South has historically been less developed and has had lower levels of human and physical capital. Relative to the rest of the country, the southern region relies less on manufacturing and more on oil, mining, and services, including tourism. While tourism has contributed to a recent increase in employment and income at the local level [9], Mexico’s southern region still has lower wages and higher informality rates than the rest of the country, as well as a more unequal income distribution.

An additional source of spatial heterogeneity in development across Mexican regions is the violence that stems from organized crime. Such violent activity is distributed unevenly across space, reflecting the locations of conflict between organized criminal groups and resulting in lower employment and net out-migration of skilled labor at the local level in more violent areas [10].

While income differences across and within regions are still large, some policies have helped boost employment and wages in lagging regions. In the context of minimum wage increases and targeted infrastructure spending in Mexico’s South, wage growth among lower-income households in that region outpaced that of all other income groups and regions between 2018 and 2022. However, for minimum wage and government expenditures to induce regional convergence in labor market outcomes, these must be accompanied by persistent increases in productivity and labor demand.

Skills and the quality of employment

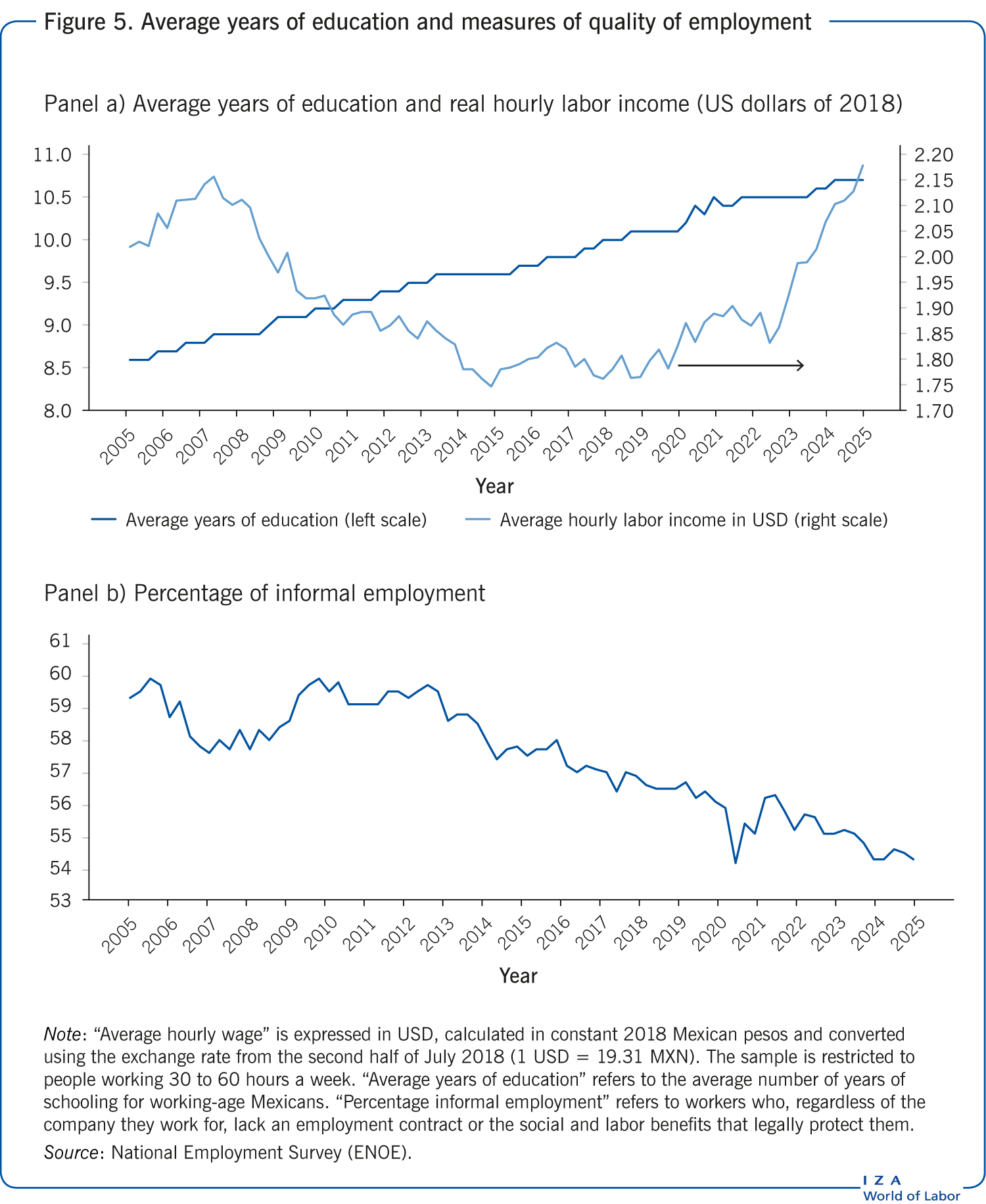

Over the last two decades, Mexico has made progress in increasing the education of its labor force. According to the National Employment Survey (ENOE), the average years of schooling for working-age individuals in 2005 was 8.6. By 2025, it was 10.7. A branch of literature has shown that large-scale conditional cash transfers contributed to this increase by inducing additional school enrolment in poorer communities from the mid-1990s to the late 2010s.

At the moment, Mexico is among the Latin American countries with the highest levels of schooling, just below Chile. Figure 5, Panel a, shows the evolution of the average years of education for working-age Mexicans in the last 20 years.

Despite these achievements, wages are stagnant, and the average quality of employment is not improving (see Figure 4, Panel a). More than half of all workers are employed in the informal sector (59% in 2005 vs. 54% in 2024; Figure 5, Panel b), where they have few–if any–benefits (like a contract, access to health insurance, or retirement benefits). The average number of weekly working hours has remained at about 42-43 over the last 20 years, making Mexico second among OECD countries in terms of working hours. Total productivity has been falling for the last 20 years [11]. Overall, any measure of employment quality reported in the ENOE shows limited growth or stagnation over the past two decades.

Previous research has noted that these improvements in education in Mexico have not translated into better jobs (in terms of wages). As schooling improved in Mexico, the returns to education have fallen. In other words, as the supply of skilled labor increased, wages decreased for this type of labor. Moreover, there is evidence suggesting that demand for skilled labor has not increased much relative to supply.

These phenomena might be partially explained by the fact that, in Mexico, most firms are small, and most workers are employed in small firms. According to the Economic Census, 95% of all establishments had less than ten workers in both 2003 and 2023. Such firms are too small to require much skilled labor, and their size also limits their potential returns to scale, resulting in the creation of low-productivity, low-wage jobs [12], where many high-skilled workers end up employed.

While there is no consensus on the root causes of the preponderance of small firms in Mexico, a prominent hypothesis is that many Mexican firms remain small, at least in part, to avoid government detection that would force them to become formal and pay additional taxes [12]. This problem has proven particularly hard to solve, as most interventions towards this goal–such as reductions in government costs or increased monitoring– have had very modest or null effects.

In Mexico, there are only a few policies with labor formalization as an objective. The Ministry of Labor routinely performs firm-level inspections to detect employment irregularities. There is evidence that, in the short term, such inspections may increase the probability of informal workers becoming formal [13]. Moreover, in August 2025, the Mexican government reached an agreement with delivery apps (like Uber Eats) to formalize their workforce. This policy is extremely new, so the existing evidence shows only that firms complied by formalizing their employees. Relatedly, in 2021, Mexico banned domestic outsourcing. This ban seems to have drastically reduced outsourcing, increased wages, and reduced wage markdowns without lowering output or employment [14].

Limitations and gaps

The currently low unemployment rate in Mexico might be deceiving. While a low unemployment rate is better than a high one, this low-unemployment scenario might result from a lack of a safety net, which pushes many individuals to look for a job, whatever it may be. For example, there is no national unemployment insurance, though people can withdraw pension savings during periods of unemployment. Mexico City residents do have access to unemployment insurance.

In fact, Mexico’s high entrepreneurship rate may be due to a lack of options in the formal sector [15]. Coupled with the high informality rate, low unemployment may not imply an abundance of high-quality jobs. Further research is needed on the determinants of formal job creation and the transitions from informality to formality.

Another limitation is the scarcity of evidence on the consequences of disruptions to global trade after 2024. While Mexican exports have been resilient to previous shocks as of late 2025, changes to trade policy could have broad impacts on Mexico because of its position as an important trading partner of the US. Given the recent, fast-paced evolution of international trade, constant monitoring is necessary.

Looking ahead, Mexico may need to calibrate its minimum wage policy carefully. Although rising minimum wages have reduced wage inequality and boosted incomes among poorer workers, Mexico’s current minimum-wage-to-mean-wage ratio of 73.7% is already among the highest in the OECD. Mexico should handle future minimum wage increases cautiously and monitor their labor market effects.

Summary and policy advice

Mexico has an abundant labor supply, unemployment rates below the OECD average, and a still-growing working-age population. Over the past 20 years, the macroeconomic environment has been stable, average educational attainment has improved, and the country has remained open to international trade. Despite all these tailwinds, challenges persist in the labor market. Real wages are stagnant, female labor force participation remains low, and a large share of employment is concentrated in the informal sector. These problems are particularly pronounced in southern Mexico, where integration into formal and export-oriented production networks is weaker.

Informality and low wages have some common causes. The labor demand faced by many workers is weak, pushing them into self-employment or other low-productivity work. At the same time, the incentives for firms to cover the costs of formalizing workers are weak. In this context, policy must aim to improve job productivity from both the firm and worker sides: fostering firm growth and ensuring that households invest in human capital that is valuable in the labor market, especially among women, lower-income workers, and in lagging regions. With diminishing population growth, Mexico’s comparative advantage as a supplier of unskilled labor will wane. In this context, policy must support the transition towards higher-skilled manufacturing and services.

Acknowledgments

The authors thank the two anonymous reviewers and the IZA World of Labor editors for their comments. They also thank Karla Neri Hernández, Vicente López Ramírez, and Constantino Carreto for excellent research assistance, and Alfonso Cebreros and Josué Cortés for insightful comments. The views and conclusions are exclusively the responsibility of the authors and do not necessarily reflect those of Banco de México or its Board of Governors.

Competing interests

The IZA World of Labor project is committed to the IZA Guiding Principles of Research Integrity. The authors declare to have observed these principles.

© L. Aldeco Leo, D. Osuna Gómez, and J. Pérez Pérez