Elevator pitch

The earned income tax credit provides important benefits to low-income families with children. At substantial costs (over $70 billion to the US federal government), it increases the incomes of such families while encouraging parents to work more by subsidizing their incomes. But low-income adults without children and non-custodial parents receive very low payments under the program in most years. Many of these adults are less-educated men, whose labor force participation rates and relative wages have been declining for years. They might benefit significantly from a more generous earned income tax credit for childless adults.

Key findings

Pros

The earned income tax credit boosts income and work effort among low-income parents, especially single mothers, and has contributed to the steep rise in employment among single mothers in the 1990s.

Expanding the tax credit to low-income childless adults should raise income and work effort among a group whose earnings and employment have fallen substantially in recent decades.

The statistical evidence shows that work effort among low-income adults is somewhat sensitive to their net wages, and an earned income tax credit for childless adults would raise their net wages.

Cons

The earned income tax credit is already very costly, extending it to childless adults would add to those costs.

The most recent experimental evidence suggests that a childless earned income tax credit would generate only small positive impacts on employment.

Expanding the tax credit to childless low-income adults might discourage marriage and work effort (and raise tax fraud) among childless adults.

Author's main message

Expanding the earned income tax credit to low-income childless adults and non-custodial parents, especially low-income men, would modestly increase their incomes, earnings and employment. This positive outcome might be larger if the federal government combined a permanently higher earned income tax credit for this group with significant outreach, to improve worker knowledge of the credit and how to file for it; many potential workers also need stronger workforce services or child support provisions, to improve their likelihood of finding and keeping jobs.

Motivation

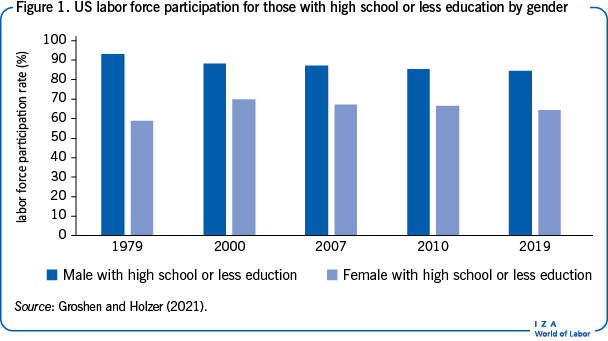

The earned income tax credit (EITC) in the US has succeeded in raising employment and earnings among low-income families with children, most of them headed by single mothers. But few benefits now go to low-income childless adults and non-custodial parents, especially men, whose earnings and labor force participation rates have declined substantially in the last few decades—in fact, more than for any other demographic group, as shown in Figure 1.

The EITC for families with children has at least some political support from both of the major political parties in the US and has grown in generosity over time, during both Republican and Democratic administrations. Research offers quite strong evidence of positive impacts of EITC benefits, not only on the earnings and employment of low-income parents but also on the educational attainment and other outcomes of their children. Expansion of the EITC for childless adults would almost certainly increase their incomes (net of taxes) and would likely boost their earnings and employment rates – though by smaller amounts – while also increasing tax filing and child support payments made by low-income non-custodial fathers.

In addition, many other OECD countries have instituted some form of EITC, also known as “in-work tax credits,” for workers with low employment and income. Their impacts on employment have been studied many times in the US (and elsewhere), and most such studies find some positive effects on employment of low-income parents with custody of children [1].

Discussion of pros and cons

The EITC is currently the largest public cash assistance program for poor families. It currently costs over $70 billion a year at the federal level alone. A number of states supplement the federal credit with credits against state income taxes.

As a cash assistance program for the poor, the EITC has had much greater political support than unconditional cash assistance (or “welfare”). The reason is simple: welfare provides families with benefits if the parents are not working and reduces those benefits as earnings rise, thus reducing net wages and creating a disincentive to work.

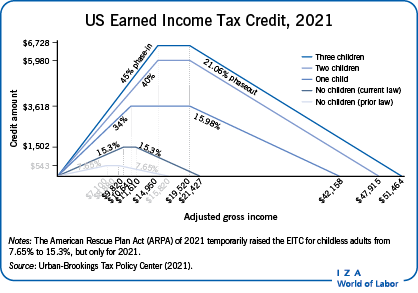

Instead, the EITC provides fully refundable subsidies at the following rates (for 2022):

34% of earnings for families with one child, up to an earnings ceiling of nearly $11,000 and a maximum credit of over $3,700;

40% for families with two children, up to an earnings ceiling of over $15,000 and a maximum credit of over $6,000; and

45% for families with three or more children, up to an income ceiling of over $15,000 and a maximum credit of nearly $7,000.

Thus, the EITC significantly raises recipients’ net wages (up to the earnings ceilings above), which should induce recipients to work more — as long as their labor supply elasticities are generally positive (i.e., their work effort responds positively to their net wages). That appears to be the case for low-income single mothers. When earnings rise above the eligibility ceiling, the phaseout of credits could create a disincentive to work. But the federal EITC has a very gradual phase-out, at the rate of about 20% per additional dollar earned, so that the marginal tax rate on earnings in this range is modest, to limit the work disincentive effect.

Indeed, most studies in the past few decades have shown the positive effects of the EITC on both earnings and employment rates of poor household heads, especially single mothers. The EITC expansion (along with a strong economy and welfare reform) has also been credited with raising single mothers’ employment rates in the 1990s.

There is some evidence of a negative effect on work during the phase-out of the benefit, but it is quite small, as are any negative effects on marriage rates [2]. Researchers find other positive effects of the EITC as well, particularly on recipients’ wage growth (since they are gaining more work experience over time) [3].

However, while the subsidy rate is 34–45% for families with children, the rate for low-income childless adults in most years (except temporarily under the American Rescue Plan Act, ARPA, in 2021) is just 7.65%, up to a ceiling of only $7,320—only enough to match their share of payroll tax payments—and up to a maximum credit of just $560. It begins to phase out at just over $9,000. The rationale for much lower subsidies to childless adults, no doubt, is that it does not directly benefit children – though its indirect benefits (for those with non-custodial parents, now or in the future) might not be trivial. At this low subsidy rate, the current take-up rate of the EITC among the target population of childless low-income men and women is quite low, and its effects on labor market outcomes are very limited.

Should the EITC for childless men and women rise?

A number of proposals in the past few years have called for a substantial increase in the EITC for low-income childless adults or for low-income adults who are non-custodial parents and paying their full child support order [4].

How many people would benefit from an increased EITC and what are their demographics? Approximately 17 million people in the US received EITC payments from ARPA in 2021, with eligibility beginning at age 19 [5]. This number would be reduced, by as much as 5 million, if eligibility began at age 25 (as does the EITC currently). Low-income childless adults include both men and women, but men make up a larger share of this group, especially among people in their 20s and older. Both groups tend to have low levels of education. Some low-income childless men are non-custodial fathers of children who live with their mothers, while others (both men and women) might expect to become parents in future years.

As noted above, employment (and relative wages) among less-educated men have declined dramatically in recent years. It is quite puzzling that the demographic group in the US whose labor market opportunities have declined the most, and whose incentives to work have dropped accordingly, benefit the least from a program designed to encourage more work and higher earnings among the poor. Employment rates of less-educated black men are very low – especially since so many are non-custodial fathers and/or have been incarcerated.

These men often face very little formal employer demand (though they often work informally and sporadically off the books). But their incentives to work are low as well, not only due to low wages but also to child support burdens among non-custodial fathers. For instance, judges often issue child support orders by “default,” or without any specific information about a non-custodial father’s labor market prospects, which are often quite modest. For low-income non-custodial fathers who have had children with multiple women—a growing phenomenon often referred to as “complex families”—the sum of child support orders can become extremely burdensome. If the father cannot make his payments, he falls into debt (arrears); and, if his family receives any public assistance, many states will add the costs of these support programs to what the father owes. If he becomes incarcerated, the unmet orders can continue to accumulate and the arrears grow. Once a non-custodial parent is in arrears, the tax rate on his low earnings becomes quite steep—usually 50% [6].

As a result, many fathers simply choose to not work (in the formal labor market) and to not pay child support. To get these fathers to pay, some states suspend their driver’s license and eventually incarcerate them—both of which, in turn, can further reduce their earnings potential. Where enforcement of these provisions is limited, there are very strong incentives for the non-custodial parents to exit the job market and the child support system.

Would raising the EITC for childless adults increase their employment?

What might an expanded EITC program that is intended to encourage employment among the low-income childless population (including non-custodial parents) look like, and how would it compare with the generous EITC benefits received by low-income custodial parents of two or more children? The main design parameters that need to be considered are the subsidy rates, earnings ceilings, and phase-out rates.

Would an expanded EITC program encourage more work among less-educated individuals in general and non-custodial parents in particular, especially men? While there has been relatively little rigorous evaluation of such programs in the US or in other OECD countries, there are several reasons to believe that the effects could be beneficial. For one thing, estimated labor supply elasticities for this population – which measure the responsiveness of work effort to wages – are quite positive: roughly 0.3–0.4 for low-income men and a little lower for low-income single women.

The first study of a childless EITC using credible statistical methods was based on a state-level experiment of an expanded EITC program for non-custodial parents paying child support [7]. Starting in 2006, New York State administered an expanded EITC program for non-custodial parents, offering up to 250% of the federal EITC benefit for low-income childless men and women (or more than $1,200), as long as the non-custodial parent was fully up to date on child support payments for the year. Take-up rates were not very high. Statewide, less than 3% of non-custodial parents with a child support order received a credit (9,600 out of more than 350,000) in 2009. Nevertheless, the study found positive impacts of 1 to 2 percentage points on employment and on child support payments for this population.

The most recent EITC evidence

In recent years, important new evidence has been generated on the labor supply effects of increasing the EITC for low-income parents and childless adults. Most rigorous evidence continues to suggest that the EITC raises both income and employment for low-income parents. However, one study questioned this result, claiming that employment does not rise for poor mothers in most cases after EITC expansions and that the increase in the 1990s was driven mostly be welfare reform [8]. Another study argues, however, that the EITC raises employment of low-income mothers for a wide range of empirical specifications, even during the 1990s [9].

The most important recent study of EITC payments to childless adults (including non-custodial parents) has been the evaluation of a pilot program called Paycheck Plus [10]. The program provided EITC payments of up to $2,000 to qualifying childless adults with positive earnings of up to $30,000 per year and who filed their taxes for 3 years; participants were chosen via random assignment in New York City (2012–15) and Atlanta (2015–18). The samples included both childless men and women, though special efforts were made to recruit poor men with particular barriers to work.

The pooled results across the two cities indicate that employment rose for the treatment group, by an average of 1.8 percentage points in years 2 and 3 (and, not surprisingly, by much less in the first year), relative to baseline employment rates of 74–80%. Pre-tax average earnings did not rise, though after-tax earnings rose by several hundred dollars per year. Results in New York City were considerably stronger than in Atlanta; in the former, employment and after-tax earnings rose by over 2 percentage points – mostly among women and disadvantaged men (defined as those who had been incarcerated or were non-custodial fathers), though not for less-educated men more broadly. In Atlanta, employment increased by only 1 percentage point (and not significantly); it rose marginally for men but not women. Child support payments rose in New York among non-custodial fathers, while tax filing rose in both cities; few effects on other outcomes like health were observed.

The primary reason for the weak results is the low rate of tax credit receipt – only 42% of the treatment group across both cities received such a credit in the first year and only 26% in the third year. Non-receipt was due to lack of eligibility (at least in some years as earnings fluctuated), lack of filing among those eligible, and lack of receipt among those filing (since receipt of the subsidy required more effort than when the federal government automatically sends a check to those eligible). Receipt was lower in Atlanta than in New York; and operational difficulties especially reduced receipt in the third year in the former. Efforts to improve filing and receipt would likely lead to stronger impacts on employment and earnings.

Other efforts to help raise employment among low-income men who face low employer demand are needed. Adding a “light touch” referral to the Employment Service for those eligible for Paycheck Plus had little effect on employment gains in New York [11]. Evidence from recent evaluations of more serious programs for this population is also discouraging. For instance, a program to raise employment among poor non-custodial fathers, The Child Support for Noncustodial Parents Employment Demonstration (CSPED), did not generate employment or earnings boosts on average for participants, though payment of child support did rise. Also, pilot programs that provide transitional jobs for a year or less for the hard-to-employ, paid for by the public sector or non-profits, have been evaluated by the US Department of Labor (the Enhanced Transitional Jobs Demonstration, or ETJD) and by the Department of Health and Human Services (the Subsidized Transitional Employment Demonstration, or STED). Generally, these programs provided only short-term earnings and employment boosts for participants, and reductions in recidivism among those with criminal records at a few sites.

Of course, this body of evidence might soon be supplemented by analysis of an important natural experiment: the national rise in childless EITC payments during 2021 as part of ARPA. Since that increase was smaller than the one in Paycheck Plus – the maximum credit was $1,500 rather than $2,000 – and since it lasted for just one year, it might generate even milder effects. On the other hand, a lasting childless EITC at the federal or state levels might generate more tax filing and greater benefit receipt over time than did the temporary ones to date, as the population of childless adults becomes more familiar with the credit and how to attain it.

Some decisions to make about expansion of the EITC

In preparing to expand the EITC to childless adults and non-custodial parents, one of the first decisions to make is whether low-income childless adults should be broadly eligible or whether eligibility should be limited to non-custodial parents (as long as they are up to date on payment of their child support orders in a given year). The narrower EITC costs much less and targets the group that faces the worst market incentives to work right now: low-income non-custodial parents under a large child support order. But these proposals seem to reward such men for behavior that undercuts two-parent families, and provides no assistance to other poor childless adults. Most proposals therefore now call for the broader program for all low-income childless adults, rather than the narrower one only for non-custodial parents.

Another issue to resolve is the age at which individuals would become eligible for the EITC. To reach low-income youth, especially young men who are at high risk of “disconnecting” from the worlds of school and work, some proposals call for making individuals eligible at age 21 or even 19. Whether college students – either part-time or full-time – should be eligible is another question.

Another concern is that adults who receive EITC benefits might be discouraged from marrying, since that could jeopardize the EITC benefits one or both partners receive. The “marriage tax” feature of an EITC extension could be countered in a number of ways—such as by further raising the income level at which the phase-out of the credit begins for two-parent families, or by counting just half the income of the partner with the lower income when calculating tax liability for married joint filers.

Finally, the tax credits available to families with children have grown dramatically over time, especially in 2021, when, in addition to the childless EITC expansion, the Child Tax Credit (CTC) also increased dramatically (from $2,000 per child to $3,000 for all children and $3,600 for those aged 5 and less). This expansion was just for one year as well, and it had no direct effect on childless adults. But many analysts and politicians have been considering possible changes in the CTC and the EITC together. The role of a childless EITC in any such restructuring of tax credits for families with children would have to be carefully considered.

Limitations and gaps

Despite the potentially positive effects listed above, there are also some important costs of an expansion to be considered, and some limitations on what is known about the effectiveness of the EITC in these circumstances. First, the direct budgetary cost of a childless EITC is not trivial. According to the Congressional Research Service, the ARPA expansion in 2021 cost about $12 billion [12]. Even so, it is at least possible that this cost might be paid for with reductions in public benefits to families with children.

Moreover, researchers do not know the full extent to which low-income childless men would be affected by an expansion of the EITC, for several reasons. First, as already noted, the EITC is designed as a remedy for weak incentives to work on the supply side of the labor market, whereas major barriers to employment for this group might exist on the demand side. Given the weak results of the transitional employment demonstrations, the hard-to-employ might need more substantial assistance to gain employment, such as ongoing subsidized work.

In addition, many non-custodial parents in arrears on their child support might not be eligible for the EITC, due to lack of work; even if they fully meet their obligation in a given year, their EITC benefits will be withheld if they are in arrears, thus weakening their incentives to work or file income tax returns. In Payroll Plus, take-up and benefit receipt were low; and take-up can be hard to improve, especially for a population with weak earnings potential and strong disincentives to participate. To encourage more non-custodial parents to participate, an EITC expansion might need to be accompanied by strong workforce services – like permanently subsidized jobs – and perhaps some type of arrears management or forgiveness (beyond what was provided in CSPED).

An additional concern about expanding the EITC program for childless adults and non-custodial parents is that it could exacerbate fraud and misreporting of income by potential recipients [13]. Currently, the Internal Revenue Service estimates that roughly a quarter of all EITC claims and payments, worth roughly $15–20 billion per year, are fraudulent. This figure would likely rise with an expansion of the EITC program, though it is difficult with the information now available to predict by how much.

Perhaps the most important limitation is that the evidence on the potential impacts of an extension of the EITC program on worker behavior remains limited, as the only rigorous evaluation evidence to date is from Paycheck Plus. New evidence will likely be available soon on the effects of the ARPA expansion in 2021, though a single year of availability would limit its effectiveness.

It would be useful to have more city- and state-level experiments with the extension of the EITC program to childless adults and non-custodial parents that can be rigorously evaluated for their impact. Such experiments could yield valuable evidence on effectiveness that could inform decisions on how to proceed at the federal level. Only then would enough evidence exist to accurately judge the benefits of higher earnings and employment to childless adults, and whether these benefits over time are sufficient to make the policy cost-effective.

Summary and policy advice

Federal and state EITC payments to low-income parents with children have expanded dramatically in recent decades, with clear benefits to the poor in terms of higher income and work effort. However, few jurisdictions extend much of these benefits to low-income childless adults and non-custodial parents, who are often less-educated men. Indeed, this group has suffered greater losses in relative wages and has responded with greater declines in labor force activity than any other major demographic group.

The best recent experimental evidence suggests that an enhanced childless EITC would generate higher net incomes and small increases in employment among childless adults, with some occurring among men and some among women. Evidence is not yet available from the 2021 increase in the childless EITC in ARPA. If such an increase were permanent, it would likely induce even more adults to file taxes and receive the benefit, as their knowledge about how to get it would rise.

At a minimum, federal or state governments should experiment with extensions of EITC benefits to childless adults and non-custodial parents to generate more information through rigorous evaluation of the benefits and costs. Any experimental EITC should be lasting and large enough to incentivize changes in behavior toward work, child support payments, and tax filing. Major outreach efforts to low-income men might also be needed to generate sufficient take-up among those who currently avoid formal work and tax filing, along with strong workforce services (like permanently subsidized jobs) and child support provisions, such as help with managing arrears.

Acknowledgments

The author thanks two anonymous referees and the IZA World of Labor editors for many helpful suggestions on earlier drafts

Competing interests

The IZA World of Labor project is committed to the IZA Guiding Principles of Research Integrity. The author declares to have observed these principles.

© Harry J. Holzer