Elevator pitch

Global value chains (GVCs) describe the cross-national activities and inputs required to bring a product or service to the market. While they can boost exports and productivity, the resulting labor market impacts vary significantly across developing countries. Some experience large-scale manufacturing employment, while others see a shift in demand for labor from manufacturing to services, and from lower to higher skills. Several factors shape the way in which a country’s labor market will be impacted by GVC integration, including the type of sector, lead firms’ strategies, domestic skills base, and the institutional environment.

Key findings

Pros

The employment effects of GVC integration are mixed in developing countries, with both winners and losers emerging in the process.

Labor market impacts go well beyond jobs and include changes in relative payoffs to skills, levels of inclusion, and skills development (upgrading) potential.

Some of the key determinants of labor market outcomes in GVCs are not within the control of domestic policy.

Women take a large share of jobs in labor-intensive chains, but lose out from upgrading.

Cons

In most high-income countries, higher-skilled workers gain in terms of rising wages, but lower-skilled workers experience greater job losses.

Countries with large labor surpluses and low wages have seen strong jobs growth following GVC integration.

Patterns across countries show that as sectors and countries upgrade, wages rise but net employment falls, and more skilled workers gain most.

Raising labor standards in GVCs appears to be a win–win proposition overall, with workers benefiting from improved conditions and firms experiencing productivity gains.

Author's main message

GVC integration may be a catalyst for job creation, but its employment effects are complex and difficult to control domestically. Large-scale job creation in GVCs may require sustained low wages, and labor and skills upgrading may worsen both inequalities and outcomes for low-skilled and female workers. Policy should focus more on the productivity gains associated with GVC integration rather than its role as a source of job creation. Policies to support supply-chain deepening and exploit technology spillovers, with a strong focus on skills development, will support an adaptable labor force positioned to maximize the dynamic potential from GVCs.

Motivation

“Value chains” describe the full range of activities that firms engage in to bring a product or service to the market, ranging from the design, production, and marketing of products, to logistics, distribution, and support. A “global value chain” (GVC) is when some of these activities take place across national borders. Typically, a GVC describes a situation whereby a firm, or group of firms, organizes and manages a network of activities spread across multiple countries, which is designed to take advantage of specific sources of comparative advantage in each location.

There is increasing interest from policymakers in developing countries to “join” GVCs, with a motivation to attract investment, increase exports, and create jobs. Integration into global markets for trade and investment is a critical pathway for developing countries to grow and to access productivity-enhancing technologies and knowledge. For many countries, participation in GVCs also plays an important role in the process of structural transformation, contributing to the creation of more productive, higher-quality, and higher-earning jobs.

However, reaping the benefits of GVC integration does not come automatically, and the dynamics shaping the emergence and development of GVCs may also represent a threat to sustainable, quality employment, particularly for those without portable skills or who face labor market segmentation. GVC integration is also likely to have distributional impacts, both through employment effects, as well as through effects on wages and working conditions.

Discussion of pros and cons

The structure of global production, trade, and investment has been transformed in recent decades. Falling transport costs, greater global openness and cooperative trade policies, and the information and communications technology revolution have allowed for vast productivity gains by fragmenting production into discrete processes that are relocated around the world to where they can be most cost-efficiently produced. This has resulted in widespread global production networks (or GVCs), often spanning dozens of countries and involving hundreds of firms, from small-to-medium enterprises (SMEs) to multinationals. More than 60% of global trade takes place within such GVCs, employing an estimated 16 million people worldwide [1]. Because the organization of GVCs involves restructuring the activities and locations of economic activity, it has fundamental implications for jobs: for what they are, where they go, and who gets them.

Offshoring in advanced economies

There exists now a fairly good track record of the impacts of GVCs in advanced economies [2]. This literature mainly involves the implications of “offshoring,” where firms in advanced economies outsource parts of the value chain (goods production and/or services) to third countries. While many debates remain to be settled in the offshoring literature, what is becoming increasingly clear is that GVC integration for advanced economies has reinforced the effects of skills-biased technical change. That is, offshoring will involve the most labor-intensive processes in the value chain. This will obviously result in a reduction in employment in the short term. But it also means that the firms doing the offshoring should become more productive, both because the costs for the offshored activities should decline and the productivity of their now more specialized domestic activities should increase. This would, over time, result in growth of the firm and more hiring. So the net, economy-wide effects on employment from offshoring may be neutral or even positive over time. But the composition of employment will change, with demand for manual and routinized activities (normally, lower-skilled) declining and that for non-routinized (higher-skilled) activities increasing [3].

But what is the evidence in developing countries, where GVC integration more often means being on the receiving end of foreign direct investment (FDI) in labor or resource-intensive parts of the value chain?

GVC integration and developing economies: What do we know?

Jobs

While the evidence of the impact of GVC integration on jobs in developing countries remains largely anecdotal, empirical evidence is beginning to emerge. The impacts on jobs can be thought of in four dimensions: (i) the number of jobs; (ii) the returns to jobs, including both job-specific wages and upgrading potential; (iii) the distributional impacts of jobs and wage effects; and (iv) the working conditions prevalent in GVC-linked jobs.

Lower-income countries that have been successful in attracting GVC investment often experience a significant increase in formal manufacturing jobs. In Bangladesh, for example, the emergence of the GVC-oriented export apparel sector led to the employment of more than three million people over the last two decades. On a smaller scale, Lesotho’s integration into the global apparel sector in the late 1990s transformed the structure of the economy, generating more than 50,000 manufacturing jobs—employing up to 10% of the workforce—in what was previously an almost fully agrarian economy. But the impact goes beyond the formal sector, as the growth of large, GVC-linked formal companies also increases the opportunities for subcontracting and other spillovers to smaller and informal firms. This is very common in sectors such as clothing and footwear.

But it is also important to recognize that a large increase in jobs in developing countries that results from GVC investment does not necessarily imply an increase in “labor intensity” (i.e. a larger expenditure of labor relative to capital). In fact, it is usually just the opposite. For any given volume of output, GVC participation will actually result in fewer jobs. This is because participation in GVCs requires companies to invest in improved technologies and to meet productivity requirements and strict quality standards, and because growth in output allows firms to gain productivity from scale economies.

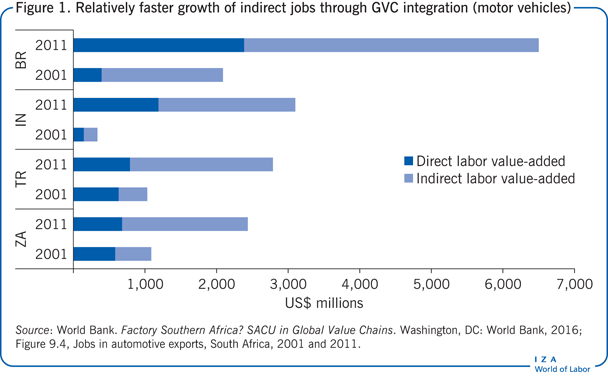

But developing countries are not a monolith, and the scale and nature of jobs impacts from GVCs will depend crucially on comparative advantage for hosting labor-intensive stages of production. A recent analysis of South Africa’s integration into the global automotive value chain during the 2000s highlights the complexity of the GVC job-creation story. While GVC integration coincided with a sharp decline in labor intensity of automotive exports (from $37 of labor per $100 of exports in 2001 to below $30 in 2011), significant nominal growth in jobs occurred as a result of the automotive sector’s extensive backward links to the domestic economy. While each direct job in the automotive sector was linked with one indirect job in 2001 (such as in a steel plant or an accounting firm, for example), by 2013 it was linked with three indirect jobs. Moreover, most of these jobs gains came through backward links to the domestic services sector rather than manufacturing (Figure 1).

Wages

At an aggregate level, the fact that GVC-oriented investment is concentrated on low-wage economies is supported by evidence showing that wage differences across locations are a substantial predictor of employment generated by new entry of multinational firms, and that changes in cross-country relative wages have large employment effects [4]. On the other hand, there exists a considerable amount of evidence showing that multinational firms pay higher wages than similar firms (i.e. in the same sector) located in the host economy [5]. This wage premium paid by foreign firms may reflect a number of factors, such as higher productivity, the fact that these firms employ the most skilled workers, a strategy to mitigate worker turnover, or simply a lack of sufficient knowledge of local labor markets. Whatever the reason, it suggests a positive aggregate story: GVC-oriented multinational firms improve their productivity by concentrating labor-intensive activities in low-wage countries, but in doing so they raise wage levels in those countries.

Of course, from a development perspective at the national level, the question is what happens over time. Development requires wage growth to move workers out of poverty and into higher income levels. But if those same factors that allowed globally “footloose” firms (i.e. firms that are not tied to any particular location or country) to locate in the host economy also allow them to just as easily shift out to a lower-cost location, countries may be locked into a “race to the bottom” on costs, which will most likely result in suppression of wages. The answer is improving productivity, as well as moving to higher value-added segments of GVCs that can support higher wages. What matters are unit labor costs, not wages per se.

A key part of the wage growth story is human-capital development. Empirical evidence shows that multinational investors tend to spend more than domestic firms on the training of workers, although this is far from consistent across sectors, countries, and FDI source countries [6]. This investment in training matters because, as shown in one of few studies that has been able to match data on firms with that on workers in those specific firms, the “foreign wage premium” only emerges over time and is explained only by workers that receive on-the-job training [7].

Inclusion

For many developing countries, attracting GVC-oriented investment contributes to more “inclusive” job creation (i.e. it allows access to jobs for youth, women, and lower-skilled workers), as demand is largely for lower-skilled, labor-intensive activities. In fact, in the sectors most intensely traded in GVCs—apparel, footwear, and electronics—employment is highly concentrated among lower-skilled, young female workers. And employment of these workers often draws workers from lagging, rural areas. However, developing countries that are more competitive in technology and skills-intensive activities may face, like more advanced economies, sharpening disparities, as demand for labor is biased toward higher-skilled workers. Indeed, this same challenge is experienced by low-income countries as they seek to upgrade to higher value-added positions within value chains. For example, as a firm and a sector shift to more skills, and capital-intensive activities, it is common to see a significant shift from female to male employment—described as a “defeminization” of the labor force [8]. This is for a variety of reasons including skills, but also cultural factors, where jobs involving machinery may be viewed as being more suitable for men than women.

Another aspect of inclusiveness is the nature of the firms that participate in GVCs. The strict standards and quality certification requirements that are common in most GVCs imposes a cost of compliance that is often more difficult for smaller firms to bear. Thus, SMEs often find themselves locked out of GVC participation. This is true in agricultural sectors, where, for example, commercial farms and large plantations are better positioned to comply with supermarket standards than small and medium producers.

Working conditions

Finally, any assessment of the employment effects of GVCs must take into account the working conditions involved in the carrying out of jobs. This tends to be an area where anecdotal evidence on sweatshop conditions, worker safety, and lack of benefits, among other things, suggests that GVC integration has negative consequences for developing countries. In many GVCs, however, global lead firms (including retailers and major brands) are now routinely operating with standards for health, safety, environment, and treatment of workers that exceed what is demanded by host governments and by the International Labour Organization (ILO). Recent research from the Better Work program, which is a partnership between the ILO and the International Finance Corporation, that is designed to improve labor standards and competitiveness in global supply chains, provides audits and technical assistance to help factories comply with improved standards and working conditions. Evaluation results indicate that improving working conditions is a win—win proposition, in that firms which have better working conditions and pay higher wages are also more productive [9]. This suggests that workers may respond to better conditions and better pay by working harder, or more efficiently. It may also be the case that in re-designing working and management practices to ensure better working conditions, firms find more efficient ways to operate. Alternatively, it could be the case that the firms who decide to pay higher wages and establish better working conditions are already the most productive ones or, at least, that they have more far-sighted management and so as a result are more predisposed towards higher productivity.

However, such findings may suffer from the common problem of selection bias. Indeed, the gains to GVC participation in terms of wages and working conditions in all likelihood depend on the position of the firm (and the country) in the value chain [10].

Exploiting the opportunities of GVCs for jobs

The above discussion makes it clear that the effect of GVC integration on jobs varies by country, by sector (or value chain), and, perhaps most importantly, by the stage of the value chain and thus the nature of activities that take place in the country. In all cases, however, what really matters is the potential for countries integrated into GVCs to experience employment and wage growth, while maintaining inclusion, over time. The available evidence suggests there are two main (and not mutually exclusive) channels for this. The first is to deliver continued productivity growth among firms operating in the GVCs to allow for competitiveness and upgrading to higher value-added activities. The second is to capture greater value-added and jobs by extending the reach of the GVC into the local economy. Also referred to as supply-chain “densification,” this involves fostering spillovers from GVC participation and engaging more local firms in the supply network [11]. In both cases, the mechanism is through spillovers of knowledge and technology from lead firms in the value chains to domestic firms and workers.

Nature of the sector and of lead firms

One of the most important contributions of the GVC literature is the role of value-chain governance in determining outcomes in GVCs [12]. Multinational lead firms that make offshoring and investment decisions also shape the way in which those investments play out in local economies and labor markets. The possibility to grow employment through local supply-chain densification depends, to a large extent, on the multinational’s global production strategy. If production is highly internalized—for example, because a large share of value-added is considered a core competency—the multinational is likely to have little interest in local sourcing beyond non-tradable services and standardized inputs like packaging [6]. Moreover, the sector matters. Localization of supply chains is more common in sectors with higher rents and higher levels of sunk investment. And the broader productivity spillovers from GVCs appear to be stronger with lead firm investments through joint ventures than by fully foreign-owned firms.

Absorptive capacity

Most critically, absorbing the potential benefits from GVC participation depends on supply-side capabilities. Firms and individual workers must have the skills and capabilities to absorb new knowledge and adapt to new technologies and processes in order to convert this into productivity gains. One determinant of spillovers within GVCs is the technology gap that exists between local producers and multinational lead firms, which is expected to mediate the absorption of knowledge and technology from GVCs. However, the empirical evidence conflicts. Some studies find that a large technology gap is beneficial for local firms, since their catching-up potential increases, while others find that local firms are less able to absorb spillovers if the technology gap between the multinational and local producers is too big.

The relationship between absorptive capacity and labor markets is a recursive one. Absorbing knowledge and technology from GVC participation is a source of labor upgrading and productivity gains. But a domestic firm’s ability to absorb foreign technology might also be positively related to its share of skilled labor. So in countries with low skills bases to begin with, the gains from GVC participation may, in fact, be difficult to exploit.

Moreover, limited labor mobility in many developing countries is a significant barrier to reaping the gains from GVCs, as the transfer of technology and knowledge gains from GVCs to the domestic economy requires a transmission channel. Along with supply chain linkages, the labor market is one of the most important of these channels. But if newly skilled workers are not moving between foreign-owned and domestic firms, the gains from GVCs become restricted to within the foreign-owned enclave. This is precisely what appears to happen in many low-income countries, where skilled workers often end up working exclusively within a small group of foreign-owned firms. These foreign investors outcompete domestic firms for access to a limited pool of skilled workers, as they are able to offer higher wages and benefits, as well as more attractive career prospects. As a result, skilled workers tend to circulate across multinationals rather than between multinationals and domestic firms.

Labor market institutional environment

The domestic institutional environment also plays a critical role in mediating the impacts of GVCs on jobs. More rigid labor markets lower the likelihood of multinational investment. And labor market rigidity, particularly with respect to wages, is also found to be a barrier to the acquisition of skilled labor and, from this, of a firm’s potential to absorb productivity spillovers from GVC participation. On the other hand, as more rigid labor markets tend to result in less turnover of workers, this may induce firms to invest more in training and skills development.

Limitations and gaps

The implications of GVCs for jobs is not a straightforward problem, and while the research base is expanding rapidly, it continues to throw out as many questions as it does answers. What is clear, however, is that simplistic arguments against offshoring jobs, or in favor of joining GVCs, are unhelpful and, in fact, lend urgency to the need for further research to unpack the labor market effects of GVCs and to address the current limitations in the research. Such gaps and limitations include the following:

The approach to the question includes many definitional challenges and normative positions. How exactly is participation in a GVC defined? Is it the level of participation that matters or the nature (e.g. position in the value chain)? Should the concern be more about jobs or wages? If wages, nominal or relative?

The evidence shows clearly the challenge of “endogeneity”: GVC participation can impact on labor market outcomes by shaping the demand for labor and skills, but labor market outcomes, in terms of participation, skills, and wages, also have a strong role in shaping the scale and nature of GVC participation. Thus, the direction of causality between GVC participation and jobs outcomes is often difficult to disentangle.

Most of the evidence relies on aggregate data sources to track large-scale economic phenomena. It is clear how participation in GVCs coincides with, or is linked over time, to broad labor market outcomes. But most of these effects are really taking place through labor market adjustment mechanisms. We still have very little evidence of how GVC investments impact individual workers over time. Exploiting matched employer–employee datasets, which at present are available in very few, mostly high-income countries, will provide a much richer, micro-level view to understand better how GVC participation and upgrading evolves and what implications it has on skills requirements, jobs, and wages.

Results to date suggest that heterogeneity—of sectors, firm types, countries—rules the day. While that has been the argument of this contribution, it would be highly unsatisfactory as an ultimate conclusion of this research question. Further research is therefore required, that uses newly available data sources including more cross-country data sets.

Summary and policy advice

The emergence of GVCs as new structures by which production and trade are organized has spurred substantial interest among policymakers seeking to exploit the opportunities for “joining and upgrading” in value chains [13]. GVCs offer a number of potential benefits to firms and countries, including potential for output and export growth and, most importantly, productivity spillovers. Along with this, GVCs may deliver jobs and earnings growth. But the employment effects, even assuming growth in output and exports, is not always obvious in terms of their nature, scale, and even direction. Moreover, many of the determinants of these outcomes exist outside the control of the domestic policy environment, and are shaped instead by global sectoral dynamics and patterns of value-chain governance. The evidence suggests that GVC impacts on jobs are highly dependent on policy, but within a multifaceted context. Moreover, the impacts often move in multiple directions: for example, job creation and increasing access to jobs for women and youth may come at the expense of wage growth.

To complicate things further, the technologies that drive the fragmentation and globalization of production networks are not standing still, but rather changing rapidly and continuing to reshape global patterns of trade and investment, skills demands, and ultimately labor markets. With routine tasks rapidly being computerized, the advantages of standardized mass production may be fading away. Thus a traditional model of GVC integration, with entry in labor intensive, low-skilled activities (such as assembly), and a gradual shift to higher-skilled activities (including services), may become increasingly less viable. This model, which has been successfully pursued by countries in the past, such as Thailand or China, may not be the answer to support development and structural transformation in Africa.

This raises serious challenges for policymakers seeking to exploit GVCs for jobs. And it suggests that attempting to design policy to achieve specific labor market outcomes from GVCs may be a fool’s errand. Instead, policymakers would be advised to focus on exploiting the productivity-enhancing benefits of GVCs. Meeting this objective, which would in any case require successful skills upgrading of the workforce, would put the country in the best possible position to achieve ongoing upgrading of its participation in GVCs. This, in turn, should contribute to rising job quality (wages and conditions). Of course, such a transition is not likely to come without distributional consequences: as demand for relatively scarce high-skilled labor expands, demand, and therefore wages, for low-skilled workers may stagnate. This is why the second main focus of policy efforts should be on minimizing adjustment costs in the labor markets—i.e. the frictions that make it difficult for workers to move across sectors and locations as labor market conditions change. Again, this points inherently to a focus on broad-based skills, but also to other factors that can limit worker mobility.

The policies linked specifically to GVCs that may move economies in the direction of achieving the objectives outlined above, include the following:

Support for skills upgrading, both at the level of the individual and the firm, including promoting investments in lifelong skills development (education and training), improving vocational training, addressing gaps in the provision of on-the-job training, and improving the base of managerial skills among SMEs.

Putting in place linkage programs, not only to promote local supply-chain deepening but also knowledge transfer. This can be facilitated further through incentives to multinationals to assist local SMEs in the use of freely available technologies, or to acquire technologies through licensing agreements with lead firms.

Supporting the adoption of, and compliance with, higher standards for local firms operating in GVCs. This can involve capacity building, but also work to facilitate convergence of public and private voluntary standards.

Implementing labor market policies that promote labor mobility and investments in ongoing training, both by firms and by workers.

Acknowledgments

The author thanks an anonymous referee and the IZA World of Labor editors for helpful suggestions on earlier drafts. The author would also like to thank Deborah Winkler and Daria Taglioni, co-authors of previous work with the author from which much of this article has been drawn [6], [11]. Thanks also to Asier Mariscal.

Competing interests

The IZA World of Labor project is committed to the IZA Guiding Principles of Research Integrity. The author declares to have observed these principles.

© Thomas Farole

Unit labor costs (ULC)

Source: OECD Glossary of Statistical Terms. Online at: https://stats.oecd.org/glossary/detail.asp?ID=2809