Elevator pitch

Charity rating agencies often focus on overhead cost ratios in evaluating charities, and donors appear to be sensitive to these measures when deciding where to donate. Yet, there appears to be a tenuous connection between this widely-used metric and a charity’s effectiveness. There is evidence that a focus on overhead costs leads charities to underinvest in important functions, especially skilled workers. To evaluate policies that regulate overhead costs, it is necessary to examine whether donors care about overhead costs, whether they are good measures of charity effectiveness, and what effects a focus on overhead costs has on charities.

Key findings

Pros

Overhead cost ratios are easy to compare across charities relative to other metrics.

Many third-party rating agencies rely on overhead cost ratios when evaluating charities, at least in part.

Many donors report relying heavily on overhead cost metrics when choosing among charities.

Donors exhibit strong distaste for charities that report high overhead costs, even when there is no relationship with the charity’s effectiveness.

Cons

Donors’ focus on overhead costs can lead to counterproductive outcomes for charities, such as underinvestment in staff and administrative support, which hamper their effectiveness.

Measuring the quality or effectiveness of a charity can be difficult, and overhead cost ratios are often a poor metric for judging a charity.

Imposing legal regulations to limit overhead costs can create large burdens for charities.

Charities can find it difficult to compete for skilled labor due to donors’ and regulators’ desire to minimize overhead costs.

Author's main message

The overhead cost ratio is the most commonly used metric to rank charities. However, for most charities, it is a crude measure that does not adequately evaluate their effectiveness. Despite the fact that broader measures of impact are far more meaningful, donors exhibit strong distaste for high administrative costs. Excess focus on these costs can lead charities to underinvest in crucial operating infrastructure, especially skilled workers, thereby diminishing their ability to deliver services. Policymakers should avoid these simplified measures, striving instead to utilize better impact metrics, despite their enhanced complexity and costs.

Motivation

A commonly used metric for evaluating charities is their overhead cost ratio—that is, the amount the charity spends on administrative and fundraising expenses as a proportion of their total spending. Many charity ratings guides, like Charity Navigator, focus on these measures in their recommendations. Coupled with donor complaints about salaries for the senior staff of some large non-profit organizations, which are considered by some observers to be excessive, it is not surprising that a recent survey by Grey Matter Research found that nearly two-thirds of Americans believe that non-governmental organizations (NGOs) spend excessively on administrative costs. There is less emphasis on these measures in other developed countries, likely because monetary donations are substantially lower than in the US. For example, as a percentage of gross domestic product (GDP), giving in the UK is less than half of that in the US, giving in France is one-sixth of that in the US, and giving in Germany is only about one-twentieth. However, limiting overhead costs, through donor or regulator pressure, can have a particularly pernicious effect on a charity’s ability to attract highly qualified workers. An inability to pay competitive wages in the marketplace due to a need to limit administrative costs leaves charities at a disadvantage in the labor market, even if the compensating differential of working for a cause one believes in partially makes up for some of this disparity.

Discussion of pros and cons

Policymakers have, at times, attempted to regulate charities’ overhead costs directly by setting limits on these expenditures. This has been the subject of some contention in the US, where courts have struck down some of these state and local regulations as a violation of free speech. Only a handful of countries currently have formal regulation of overhead cost ratios, with some only requiring compliance for particular types of charitable accreditation. For example, South Korea caps administrative and fundraising expenses at 10% of a charity’s total funds raised. In Austria, donations are tax deductible only if the charity is registered with the government, and registered charities must limit certain non-fundraising administrative expenses to 10% of total donations [1]. With a goal of preventing fraud or enhancing efficiency in an often opaque yet large and important market, there may be temptation for regulators to intervene with respect to charities’ administrative costs. In the US, an Internal Revenue Service document goes as far as to explain that “[c]ompensation of an exempt organization’s executives is some of the information most sought by the public on Form 990. Contributors do not like to see their hard-earned money used to pay the compensation of an executive who earns many times more than the contributors, especially where they believe the executive does not perform exempt function-related tasks commensurate with such salary” ().

For policymakers to weigh the costs and benefits of such policies, it is necessary to examine the extent to which donors care about overhead costs, whether these metrics are a good measure of a charity’s effectiveness, and what effects this focus may have on charities.

Do donors care about overhead costs?

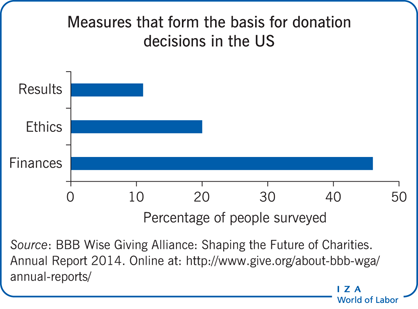

A survey by Hope Consulting indicated that, among donors who do research on charities prior to donating, the most frequently sought-after data revolve around administrative efficiency. It seems evident that the decades-long emphasis on overhead costs as a metric of quality has had an impact on donor behavior: academic research suggests that donors tend to be quite sensitive to administrative costs [2], even when these costs have no relationship to the quality of the charity [3]. This latter finding is based on data from an online giving platform. Donors could choose from numerous very similar charities—namely, projects posted by school teachers requesting funds. The platform itself added certain costs, but these costs were explicitly unrelated to the quality of the project. Yet, donors were still less likely to give when these costs were higher relative to the size of the request amount, showing strong preferences for projects with lower costs. In other words, projects received less donor funding when the administrative costs related to collecting funding were relatively higher in comparison to the projects’ costs, despite the administrative costs having no direct connection to the actual projects. Similar results have been found using workplace giving campaigns [4]. Using variation over time in the overhead cost ratio of the same set of charities, prospective donors were less likely to give and gave smaller amounts to charities when their overhead cost ratios went up.

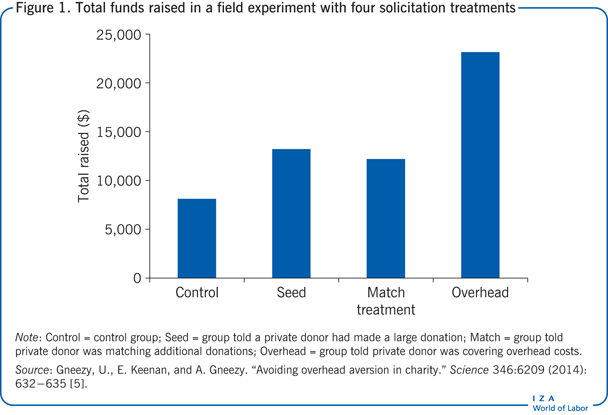

Most strikingly, a recent field experiment showed the degree to which donors focus on overhead costs, finding that the most effective use of a large donation is to cover administrative costs and to promote the charity on this basis (i.e. charities advertise the fact that large individual donations are used to pay administrative costs) [5]. In this study, potential donors were solicited with one of several possible approaches based on random assignment. Random assignment (or natural circumstances that lead to as-good-as-random assignment) is crucial, as merely observing that individuals behave in a particular way when faced with a certain situation is insufficient to draw inference about their general behavior and preferences. For instance, it could be that potential donors who are interested in charities that happen to emphasize low administrative costs are particularly generous, leading to a spurious correlation between low overhead ratios and generous donations. In this particular field experiment, individuals were assigned to one of four groups: (i) a control group who were simply asked for funds; (ii) a group who was told (truthfully) that a private donor had made a large donation; (iii) a third group who were also told that the private donor’s funds were being used to match additional donations; and (iv) a fourth group who were further told that the private donor’s funds were covering the overhead costs associated with the project [5]. As seen in Figure 1, this last treatment (iv), in which donors were told the administrative costs were covered by the large donation, raised three times as much as the control group and twice as much as the other two treatments, even though, in reality, the large donor’s funds were fungible across the charity’s activities—after all, it is merely an accounting exercise to designate certain funds, but not others, for a particular activity. It is clear, and perhaps not surprising, that donors look for shortcuts to gauge a charity’s quality (in this case the concept of a large donor funding the charity’s administrative costs appears to serve as a sufficient qualifier), given that even small costs associated with finding reliable information about charities can deter donors from giving [6].

Should donors care about overhead costs?

Having established that donors are, in fact, responsive to administrative costs, the natural question is whether this metric is useful. Of course, in extreme cases, in which a charity spends nearly all of its donations on staff compensation and other non-programmatic activities, overhead ratios can provide an important indicator of fraudulent activity. However, this does not appear to be the norm.

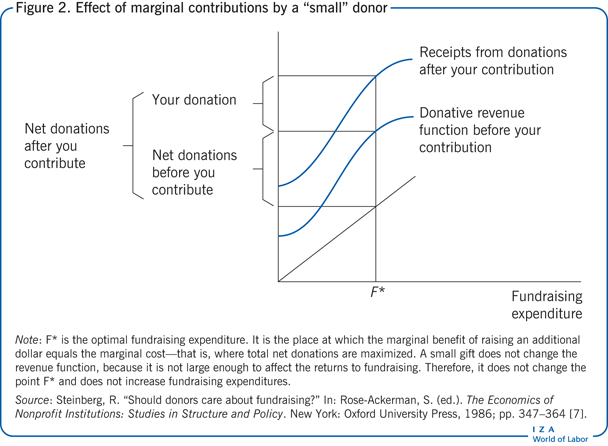

Some research suggests that overhead ratio metrics are nearly useless, since they represent average rather than marginal expenses [7]. That is, the presence of fixed costs for a charity’s operations, like rent for office space or basic office support services, means that an additional dollar donated will not be allocated primarily to administrative costs, or at least not at the same rate as the average ratio. This is illustrated in Figure 2 which shows that a charity that is optimizing its expenditures on overheads will not alter its behavior in response to a gift (that is small relative to its total donations). The straight line represents spending on fundraising, while the lower curved line represents the donations received at that level of fundraising expenditures. The optimal behavior is to spend on fundraising until the next dollar raises only one dollar, at point F*. Spending any more after that point will yield less than a dollar and therefore equate to a net loss, while spending less will yield more than a dollar and therefore be inefficiently low. A relatively small gift does not alter the shape of that revenue curve and therefore does not affect spending on fundraising.

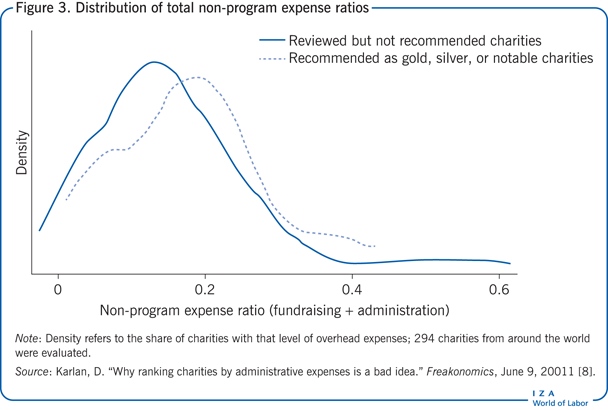

More importantly, successful delivery of the programs on which a charity is focused requires administrative support, and expanding these activities requires fundraising expenditures—indeed, using donations to fundraise and spread awareness may, in fact, be a particularly effective use of funds. A charity with a low overhead cost ratio that fails in its stated mission should not be judged more highly than one with a higher ratio that succeeds. The so-called “effective altruism” movement focuses on more meaningful impacts rather than shortcut metrics, though it is much more time consuming to investigate the former than the latter. For instance, Givewell.org, a charity rating site focused on alleviating the worst of human suffering, performs in-depth analysis of charities’ impacts, including their ability to utilize additional donations. Recommended charities actually had somewhat higher expense ratios than those that were not recommended, as shown in Figure 3 [8]. While this finding is merely suggestive, it does indicate that overhead costs are not a reliable metric of a charity’s effectiveness.

What effects does the focus on overhead costs have?

Since donors’ decisions are affected by overhead costs, despite strong indications that measures of these costs may be counterproductive, it is instructive to examine the effects that this focus has on charities’ operations. Administrative expense ratios (but not fundraising ratios) have fallen substantially in recent years, primarily driven by reductions in the proportion of funds spent on staff wages [9]. Since staff wages generally make up a large part of administrative costs, an emphasis on reducing administrative costs almost necessarily means paying below-market salaries and providing less generous fringe benefits. This is particularly worrisome, as charities may find it difficult to compete in the labor market for talent. Paying wages that are low relative to similar jobs in the private sector means that the most talented workers are unlikely to choose to work for charities. While those working for charitable organizations may receive a so-called compensating differential from the “warm glow” that they may feel as a result of working for a cause in which they believe, this can only go so far in limiting the talent drain. For example, employees who are directly involved in the delivery of services with a social mission, such as case workers at a homeless shelter, may feel a great deal of personal satisfaction from helping the less fortunate. It stands to reason, though, that the IT support staff in that organization will experience less direct satisfaction compared to the case workers, since the IT workers will not typically be involved in the hands-on tasks that elicit the aforementioned warm glow. This implies that employees like those in the IT field may not be willing to accept a reduction in pay to work for a charity, and may instead choose the typically higher-paying private sector jobs. As such, charities may find themselves having to employ lower-quality workers in important support positions.

When examining compensation for very similar jobs at for-profit, non-profit, and government organizations that compete in the same industry, there is little evidence of differential wages across organizational type, indicating that the warm glow concept is not a significant factor. Thus, charities that must limit their administrative costs (due either to regulation or in an effort to appeal to donors) have a diminished ability to pay competitive salaries, and thus stand at a clear disadvantage when it comes to recruiting and retaining talented workers in comparison to other sectors.

On the other hand, there is some evidence that employees are more productive and perhaps even willing to accept lower compensation when working for firms that practice corporate social responsibility or in the public sector. However, the complex process by which workers and firms find each other and agree to terms often makes it difficult to make strong, general statements about the exact nature of this relationship.

As a result of being less able to use higher compensation as a means of competing for desirable employees, charities may underinvest in necessary infrastructure [10]. This is exemplified in a series of case studies that illustrate the pitfalls of keeping overheads low, with staff required to cover administrative roles outside of their purview and a general lack of support for key functions [11]. Even large charities did little to no tracking of how funds were being spent, let alone how donors were being solicited, and the non-program staff had little experience in administration, accounting, or finance. For example, one charity outlined in the study did not have any staff with finance or accounting experience and found itself missing invoices and making bookkeeping errors; moreover, it was unable to track its donors or analyze fundraising, obviously inhibiting its overall effectiveness.

Unsurprisingly, misreporting of expense data among charities is therefore rampant. Public disclosure documents frequently improperly allocate expenses across different categories, perhaps unintentionally at times, but often in an attempt to reduce the all-important overhead cost ratio. This can, for example, take the form of classifying administrative expenses as program-related; a recent study found that one-quarter of US-based charities listed accounting fees as a program expenditure, despite instructions from the Internal Revenue Service to include them in overhead costs. Somewhat astonishingly, one-fifth of charities with total donations in excess of five million dollars reported no fundraising costs whatsoever [12]. Yet, stricter standards are a double-edged sword. Regulatory burdens on charities, like requiring extensive governmental filings on finances, can, perversely, increase administrative expenditures owing to a greater emphasis on compliance [13]. This can, in turn, reduce giving as donors are put off from donating in the face of higher overhead costs.

Potential alternatives to overhead cost ratios

The use of a single statistic like the overhead cost ratio is limiting and can often be misleading. Yet donors clearly want a simple metric by which to judge charities. In an effort to provide more meaningful measures, charity rating groups have moved towards more holistic approaches to evaluation. For example, the Better Business Bureau Wise Giving Alliance examines 20 standards, including whether a charity has board oversight and whether the charity assesses its own effectiveness in a formal way. Administrative and fundraising costs are included among these standards, but the threshold is relatively high and appears to be primarily used to screen out illegitimate charities. Similarly, Charity Navigator now evaluates the financial health and transparency of charities using multiple criteria; adjustments are made for the size of a charity and its area of focus to reflect differences in expectations for, say, a small, local animal shelter and a global aid agency. It has also begun an initiative to survey charities on their effectiveness and is planning to add these data to their ratings.

Limitations and gaps

While the burgeoning effective altruism movement focuses on better metrics of effectiveness for the evaluation of charities, it is not clear how to weigh immediate charitable needs, such as alleviating poverty, against investment in future potential, like biomedical research. Much of the existing academic research focuses on donors’ taste (or distaste) for overhead costs and, to a lesser extent, the effects of this focus on the charities themselves; moreover, most of these papers study non-profit organizations in the US. It is unclear how the results might generalize to other countries, though donors’ interest in the impact of their money is likely universal.

Finally, few studies have focused on how charities are actually organized and managed, which leaves a significant knowledge gap on this topic. Existing research is also insufficient when it comes to evaluating the impact that the single-minded focus on reducing overhead costs has on charities’ operations.

Summary and policy advice

Due in large part to third-party ratings agencies’ focus on relatively easy-to-measure metrics like overhead cost ratios, donors tend to believe that these measures are a useful way to decide how to direct their charitable funds. Donors clearly respond to overhead cost ratios to an excessive degree, with research showing that the aversion to high overhead costs can shift donor behavior to a great extent. However, this focus hurts non-profit organizations’ effectiveness by limiting their ability to compete in the labor market and by altering their administrative structure in a counterproductive way.

Rather than making decisions driven by the value of a particular investment in staff or support, charities must also consider the impact on their cost ratio and, by extension, donors’ willingness to give. Policymakers should resist the temptation to use these metrics to regulate charities’ activities, even as they police against fraud. Alternative measures based on the true impact of a charity’s activities would be far more useful, but they require substantial investigation and are often difficult to compare across different fields. For instance, it is far easier to gauge whether a food pantry is effective in feeding the hungry than whether a charity funding long-term research in disease prevention and control is spending its money wisely.

While better data is needed for more rigorous evaluation, policymakers should be mindful of the burdens imposed by strict reporting practices, particularly on smaller charities.

Acknowledgments

The author thanks an anonymous referee and the IZA World of Labor editors for many helpful suggestions on earlier drafts. Previous work of the author contains a larger number of background references for the material presented here and has been used intensively in all major parts of this article [3], [6].

Competing interests

The IZA World of Labor project is committed to the IZA Guiding Principles of Research Integrity. The author declares to have observed these principles.

© Jonathan Meer

Evaluating charities

Overhead costs generally fall into two broad categories: administrative and fundraising expenses. Administrative expenses include the salaries of support staff and other typical expenditures, like information technology, legal services, and insurance. Fundraising expenses are those spent on soliciting contributions to the non-governmental organization, including grants from foundations and the government.

Source: https://www.irs.gov/pub/irs-pdf/i990.pdf

Charity Navigator is a service to “guide intelligent giving.” This service is one of America’s largest and most influential charity evaluators and examines charities’ financial health and transparency using data from the Internal Revenue Service of the United States.Source: http://www.charitynavigator.org/

Among many others, ratings organizations include CharityWatch (US-based charities), CharityChoice (UK-based charities), and Change Path (Australian-based charities).